Can Early Detection and Advanced Therapies Accelerate Growth in the Aneurysm Market?

Networking |

2026-06-22 12:20:34

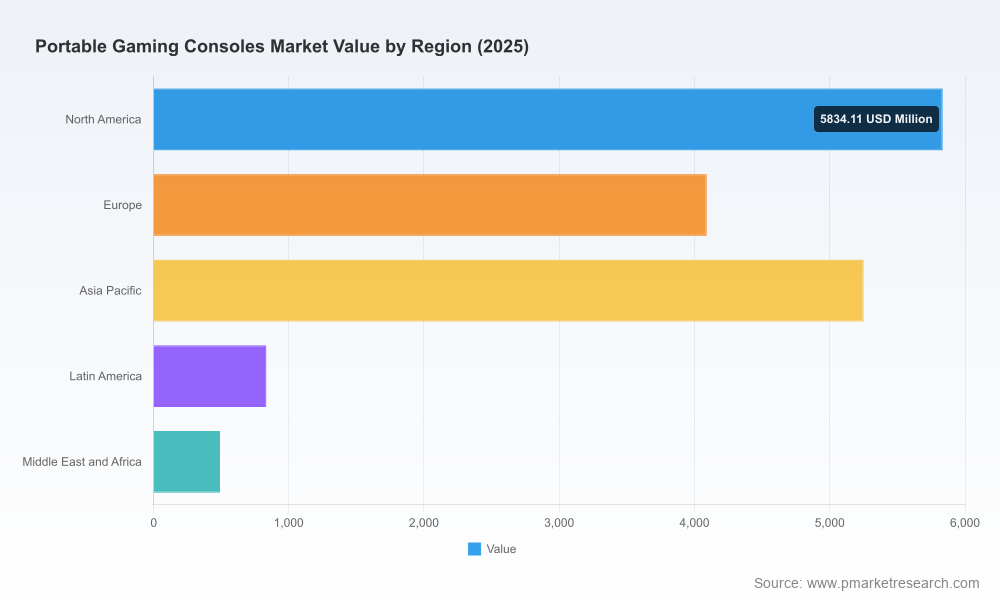

PW Consulting today publishes its authoritative industry study on the Worldwide Portable Gaming Consoles Market (base year: 2025; historical coverage: 2020–2025; forecast horizon: 2026–2032). The market reached USD 16,500 Million in 2025 and, under our baseline modeling, is expected to grow at a compound annual growth rate (CAGR) of 8.98% over the forecast period — a trajectory that nearly doubles market scale by the end of the decade. As a strategic briefing designed for executives, investors, and product leaders, this release translates that macro momentum into concrete decision levers for 2026 planning while withholding granular segment dumps to preserve the full commercial value of the underlying models.

Worldwide Portable Gaming Consoles Market

Actionable foresight: The handheld market is transitioning from a hardware-centric cycle to a hybrid hardware+services ecosystem — companies that align product roadmaps, content partnerships, and supply chains now will capture the majority of incremental value through 2032.

Worldwide Portable Gaming Consoles Market

Concentration dynamics: Market concentration is high — our analysis shows the three largest participants control the overwhelming majority of market value, with the top five accounting for over ninety percent. This structural reality changes competitive playbooks: scale advantages in distribution, IP lock-in from first-party content, and supplier leverage are decisive.

Worldwide Portable Gaming Consoles Market

Decision-ready deliverables: The report converts high-level forecasts into immediate inputs for 90-day to three-year programs: SKU rationalization, silicon sourcing decisions, channel investments, and M&A screening criteria tailored to the portable gaming value chain.

Proprietary market model: A time-series model (2020–2032) with scenario variants (baseline, cost-inflation, geopolitics, rapid-cloud-adoption) that feeds revenue, unit, and ASP sensitivity modules. The base-year calibration is anchored in observable 2025 outcomes to support immediate forecasting and budgeting cycles.

Competitive playbooks: Detailed profiles and decision matrices for leading OEMs and challenger brands, benchmarking product strategies, content ecosystems, distribution reach, and supply chain exposure.

Supply chain risk maps: Component tiering, concentration heatmaps for display and memory suppliers, and mitigation protocols including dual-sourcing and manufacturing footprint scenarios.

Go-to-market and channel strategies: Practical guidance for hybrid channel mixes, subscription bundling, retail partnerships, and direct-to-consumer tactics optimized for different customer segments (premium, mid-tier, retro/budget).

Regulatory and safety checklist: Consolidated compliance requirements for battery safety and energy efficiency across major jurisdictions, plus a playbook for product certification timelines that can materially affect launch windows.

M&A & investment screen: A scoring system and a shortlist methodology that investors can apply rapidly to identify tuck-ins and platform buys aligned with strategic ambition.

Hybrid hardware wins: Product launches and upgrades in 2025–26 emphasize hybrid portability and interoperability with home ecosystems. Firms that can combine strong hardware ergonomics with a distinctive content/library advantage are the primary value creators.

PC-class portability accelerates: The rise of Windows- and PC-based handhelds, and the ongoing development cycles of purpose-built devices, mean platforms that enable AAA-class experiences on the go will define premium positioning. This trend demands closer collaboration with silicon and thermal partners to balance peak performance against battery life and cost.

Cloud and streaming remain strategic wildcards: Streaming-focused handhelds and remote-play devices are proliferating. Their success depends on network quality, low-latency codecs, and subscription economics — areas where service providers and device makers must co-invest to unlock mainstream adoption.

Component and raw-material cost pressure: Elevated demand for high-density DRAM and advanced OLED/POLED panels, plus episodic semiconductor export controls, create multi-factor cost pressure that can compress margins or slow launches if not proactively managed.

Innovation at the display edge: Foldable and expandable POLED concepts signal potential category evolution in form factor and user experience, creating new premium tiers and accessory markets.

Nintendo: As the incumbent with significant IP and a renewed hybrid console product, Nintendo’s strategy reinforces first-party content as a durable moat. Competitive responses should assess licensing arrangements, cross-platform content strategies, and complementary accessory ecosystems.

Valve and PC-focused OEMs: Valve’s ongoing work on a next-generation device and the proliferation of SteamOS-licensed handhelds indicate a robust premium PC-handheld cohort. Companies targeting this customer must prioritize silicon partnerships and developer pipelines to ensure parity with desktop-class titles.

Windows/console ecosystem collaborations: Microsoft’s device partnerships exemplify ecosystem playbooks that combine Game Pass and cloud services with hardware partners. Expect further tie-ups and co-branded devices — players should weigh the trade-off between ecosystem alignment and platform independence.

Specialist and budget brands: A vibrant mid- and low-tier segment focused on retro and emulation devices will remain profitable but sensitive to component inflation. These vendors can defend margins through modular designs, cost-plus distribution, and focused community engagement.

Scenario planning: Our models quantify the impact of four realistic supply-state shocks on margins and time-to-market. Decision-makers can map product launches to these scenarios to determine acceptable risk profiles for 2026 SKUs.

Design-for-resilience: Technical recommendations include adaptable BOMs (dual-display sources, scalable memory footprints), thermal budgets that allow silicon flexibility, and modular designs that decouple scarce subsystems from the main assembly line.

Commercial levers: Pricing corridors, pre-order strategies, and subscription bundling are modeled to preserve revenue in inflationary contexts. For players with service ecosystems, pushing higher-margin digital packages offsets hardware margin compression.

Regulatory readiness: Battery and energy certifications are frequently underestimated schedule risks. Our checklist and regional timeline templates help product teams avoid costly launch delays.

High concentration at the top of the market implies both defensive consolidation and targeted bolt-on opportunities. Our report provides a prioritized investment framework: targets are scored on IP defensibility, software/content assets, manufacturing agility, and channel footholds. For 2026, the most compelling opportunities typically combine differentiated software/content with low-cost manufacturing or unique distribution access. The full report includes candidate screening matrices and valuation sensitivity tables designed for rapid diligence.

Product roadmap alignment: Use our scenario outputs to set realistic performance and price milestones for new handheld SKUs and to sequence launches around component availability.

Commercial negotiation: Leverage our supplier concentration analysis and cost-sensitivity models in discussions with display, memory, and SoC vendors to secure favorable terms or prioritized allocations.

Channel optimization: Apply the playbooks to rebalance online/offline mixes, decide on exclusives, and structure digital bundles to increase lifetime value.

M&A & partnership decisions: Use the scoring system to fast-track or pause deals based on resilience to trade-policy shocks and supply-cost trajectories.

Executives face a compressed decision window in 2026: hardware product cycles, silicon roadmaps, and supply chain contracts signed now determine market position for several years. Our study transforms aggregated market momentum — a market that has already surpassed USD 16.5 billion in 2025 and is on an ~9% CAGR path — into operational playbooks and risk-tested scenarios that leaders can execute immediately. We intentionally present deep methodological transparency and strategic frameworks in this briefing while reserving the full, granular segmentation, vendor-level financials, and downloadable models for our subscription and bespoke clients.

To access the complete dataset, detailed segment-level forecasts, and the download-ready decision-support tools that operational teams require to act in 2026, please visit PW Consulting or contact our industry desk for enterprise licensing and tailored workshops.

For detailed analysis of this topic, please visit the official page:Worldwide Portable Gaming Consoles Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com