Dermal Fillers In Dubai For Collagen Boosting Effect

Health |

2026-06-13 09:24:09

PW Consulting’s latest market study on Worldwide Cooling Apparel delivers an evidence-first, execution-ready briefing for executives planning their 2026 playbook. Anchored on a 2025 base year and a historical review from 2020–2025, the report forecasts the market through 2032. The category has demonstrated resilient expansion — growing from the low‑single‑billion dollar range in 2020 to approximately $2.75 billion in 2025, and is projected to approach the $5.0 billion mark by 2032 under a compound annual growth rate near 9%. For leaders weighing investment, portfolio pivots, or M&A in 2026, these trajectory signals are a necessary input to near‑term strategic choices.

Worldwide Cooling Apparel (Cooling Clothing) Market

Demand shock meets supply pressure. Rising frequency of extreme heat events has materially lifted consumer and institutional interest in cooling garments — independent consumer surveillance indicates a double‑digit year‑over‑year uplift in demand categories associated with heat protection. That demand acceleration collides with input‑side inflation (notably in technical polyester and other synthetic feedstocks) and tightening labor cost baselines in key garment hubs, requiring firms to reconcile topline growth with margin preservation.

Worldwide Cooling Apparel (Cooling Clothing) Market

Regulatory and materials inflection. New chemical and materials rules in major markets are already constraining certain cooling agent formulations and microencapsulation practices used for phase‑change systems. Companies that treat regulatory compliance as a product feature — not a compliance tax — will win faster access to enterprise and public sector procurement in 2026.

Worldwide Cooling Apparel (Cooling Clothing) Market

Fragmented competitive structure. The market remains commercially fragmented, with global sportswear brands, specialized thermal tech vendors, and legacy apparel OEMs each holding meaningful yet non‑dominant shares. That competitive topology invites targeted consolidation and high‑leverage partnerships rather than broadscale defensive plays.

Market sizing and seven‑year forecast (2026–2032) that underpins scenario planning and valuation work for M&A and capex decisions;

Demand segmentation frameworks and purchaser personas (consumer, occupational, military, medical), with go‑to‑market playbooks tailored to each buyer archetype;

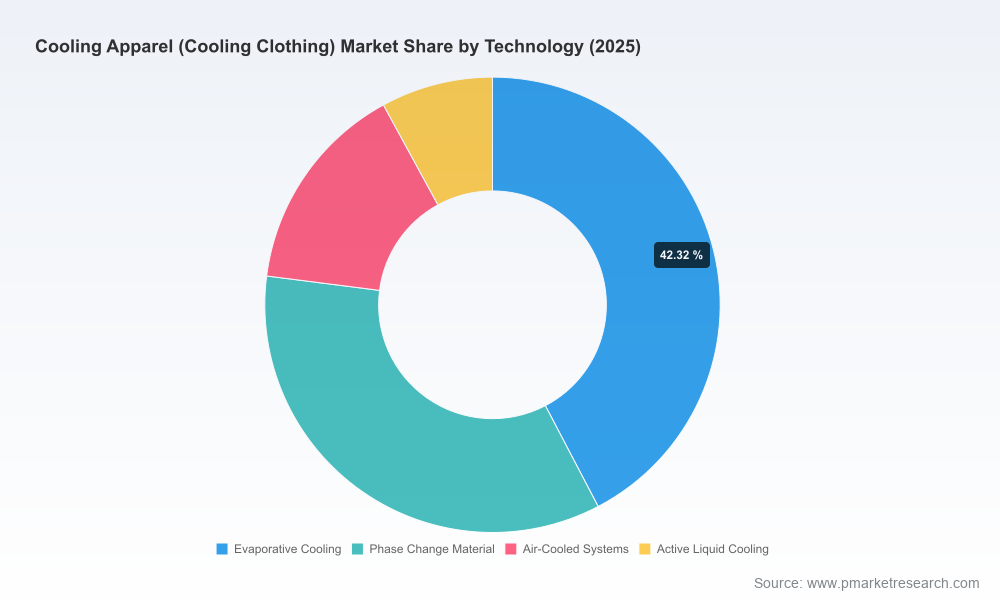

Technology and product maturity maps (evaporative systems, phase‑change materials, air‑cooled and liquid active cooling), including risk matrices for scaling, cost exposure, and regulatory fit;

Supply chain stress tests that quantify the impact of raw material price swings and labor cost changes across sourcing geographies, plus recommendations for hedging, nearshoring, and strategic inventory;

Commercial models for pricing, channel mix (DTC vs wholesale vs B2B safety contracts), and subscription/aftercare monetization strategies that preserve margin while broadening customer lifetime value;

Competitive intelligence dossiers — product roadmaps, patent trends, and recent commercialization milestones for the leading and specialist players; and

Actionable 100‑day and 18‑month operational playbooks for product launches, regulatory readiness, and targeted M&A or JV screening criteria.

Reprioritize materials strategy. Given the observed increase in polyester staple fiber pricing and renewed regulatory scrutiny of certain encapsulated PCMs, procurement and R&D must collaborate to accelerate alternative fiber trials, negotiate multi‑year contracts, and qualify compliant PCM suppliers or bio‑based substitutes.

Embed regulatory compliance into product roadmaps. With new restrictions in several top markets, product teams should treat compliance testing and documentation as launch gating criteria. Early investment in lab‑scale validation reduces time‑to‑market and prevents costly later reformulation.

Design margin recovery into pricing architecture. Firms should model multi‑scenario margin paths that incorporate raw material shocks and wage inflation. Value‑based pricing — emphasizing performance, durability, and total cost of ownership for B2B buyers — is a higher‑yield route than blanket cost‑pass throughs.

Targeted channel optimization. In 2026, top performers will narrow channel investment to high‑return cohorts: performance sports and occupational safety buyers who accept premium pricing, and selected direct channels for brand differentiation and data capture.

Operational resilience and nearshoring. Labor cost increases in important manufacturing geographies argue for a blended footprint: keep high‑value R&D and finishing near markets, while automating commodity cut‑and‑sew where scale economics still justify it.

The market is characterized by a mix of scale incumbents and agile specialists. Global sportswear leaders leverage branded fabric innovations and broad distribution networks to drive volume and cross‑sell; niche players focus on technified, targeted products for industrial, medical, or climate‑sensitive use cases. Highlights:

Major performance brands are accelerating product innovation. Several household sportswear names are extending their moisture‑management and evaporation systems into higher‑performance cooling ranges, embedding proprietary fabric treatments and leveraging athlete endorsement channels for credibility.

Specialists are converting product focus into vertical dominance. Companies offering purpose‑built cooling accessories and occupational wear are monetizing functional differentiation — water‑activated fabrics, UPF integration, merino blends, and NASA‑derived phase‑change solutions are examples where narrow expertise translates to defensible niches.

Recent commercial moves illustrate the dynamic: a leading outdoor apparel brand launched an advanced sweat‑activated cooling textile in mid‑2025 and showcased expanded infrared‑responsive collections at a major trade fair the same year. Meanwhile, a category specialist introduced sustainable instant‑cool neck gaiters earlier in 2025 — signaling continued innovation at both the premium and mass‑market ends of the spectrum.

Market concentration remains modest; the top few players collectively occupy under a third of total market value. That dispersion leaves room for differentiated entrants, targeted consolidation, and strategic alliances around raw materials and distribution.

Raw material inflation and supplier concentration. Action: implement staged hedging, qualify alternate polyester suppliers, and accelerate substitution trials for high‑risk technologies.

Regulatory tightening on cooling chemistries. Action: invest in compliance lab capabilities, prioritize physically based cooling technologies (evaporative, structural PCM encapsulation compliant with new rules), and maintain a regulatory early‑warning dashboard.

Demand volatility tied to extreme weather patterns. Action: adopt agile manufacturing capacity planning, create flexible seasonal assortments, and pilot demand‑response SKUs with quick replenishment cycles.

Labor and logistics cost shifts. Action: model a dual source strategy combining nearshore manufacturing for high‑margin SKUs and contract manufacturing for commodity lines; consider capital investments in automation for repetitive processes.

Clients engage us for a combination of market foresight and hands‑on execution: from validating an acquisition target against our integrated forecast model, to designing a three‑year product roadmap that balances compliance, cost, and consumer desirability. Our offerings for 2026 include rapid commercial due diligence, procurement optimization clinics, regulatory readiness workshops, and pilot program design for direct‑to‑consumer cooling subscriptions.

PW Consulting’s report is purposefully structured to equip executives with the strategic lens and practical tools needed to convert the cooling apparel category’s growth tailwinds into durable, profitable positions. The full study contains detailed segmentation tables, regional demand matrices, and company‑level profiles that underpin the tactical recommendations summarized here. To access the full intelligence suite — including downloadable competitor dossiers and scenario models — please visit the report page on PW Consulting’s research portal.

Base year: 2025 | Historical coverage: 2020–2025 | Forecast period: 2026–2032

For detailed analysis of this topic, please visit the official page:Worldwide Cooling Apparel (Cooling Clothing) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com