Shunt Reactor Market Forecast to 2034: Growth, Trends, and Key Drivers

Other |

2026-07-01 13:29:01

PW Consulting’s new market research preview outlines why 2026 will be a watershed year for strategic decisions in the 5G‑Advanced semiconductor ecosystem. Building from a recent base year (2025), our modelling shows the global 5G‑Advanced chip market accelerating from USD 3,850 million in 2025 to USD 5,578.8 million in 2026 and projecting to USD 41,506.3 million by 2032, driven by an observed 40.45% compound annual growth rate over the forecast period (2026–2032). The market is already concentrated: the top three firms account for roughly 72.4% of industry revenue and the top five for about 88.2% — a structure that shapes partner selection, pricing power and entry strategy.

Worldwide 5G-Advanced Chip Market

Timing: The transition from prototype and early commercial devices to broad adoption is compressing. Supply‑chain and standards maturity in 2026 mean decisions made this year about strategic partnerships, capacity reservations, and platform bets will determine competitive positioning through 2028–2030.

Worldwide 5G-Advanced Chip Market

Capital allocation: With a six‑to‑tenx market expansion expected within the decade, executives must reconcile near‑term margin pressure from scale‑up and R&D with long‑term revenue runway. Our scenario modelling quantifies trade‑offs for aggressive vs. conservative investment paths.

Worldwide 5G-Advanced Chip Market

Technology pivot points: The confluence of Release 18 (5G‑Advanced), rapid GaN RF adoption in high‑frequency radio front ends, advanced packaging and foundry node access creates multi‑vector technology risk. Boards and CTOs need a prioritized technology roadmap rather than an exhaustive list of options.

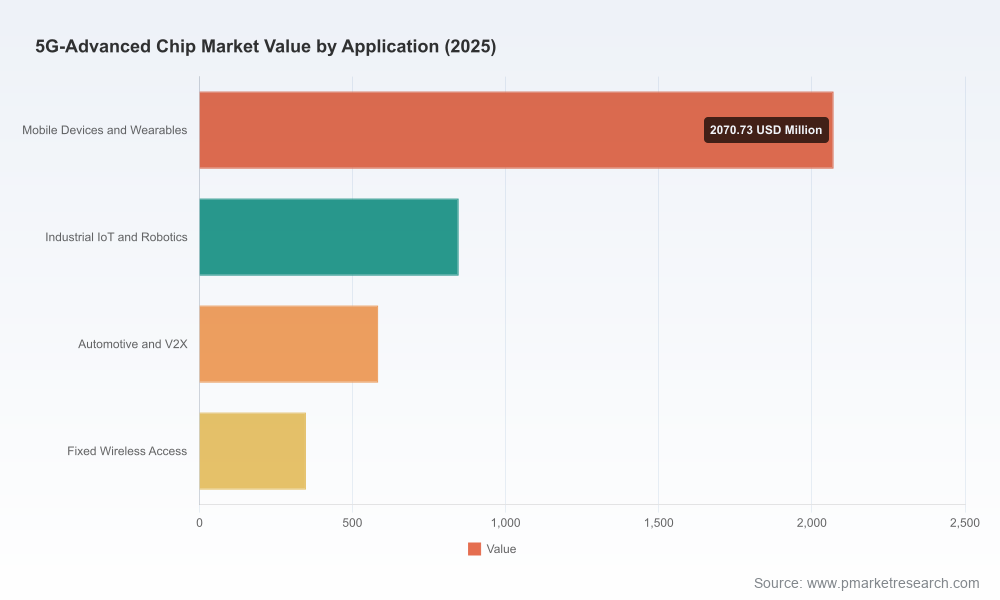

The topline growth trajectory is dramatic and durable. After a steep ramp in 2023–2025 as initial 5G‑Advanced features moved from standardisation into silicon, 2026 will shift the market from a technology‑led window to a volume and diversification phase. Our forecast captures not only handset and fixed access demand, but also fast‑growing adjacent use cases (industrial IoT, automotive V2X, telematics and FWA), where chipset complexity, integration level and certification timelines differ substantially.

Importantly, the headline CAGR of 40.45% masks important asymmetries — adoption velocity differs by device class, by compute/RF integration complexity, and by the presence (or absence) of software ecosystem support. PW Consulting’s full report disaggregates these dynamics and models cash‑flow and margin outcomes under multiple adoption pathways; the detailed split tables and company shares are available in the subscriber release.

Standards and product readiness: 3GPP Release 18 has moved from specification to product reality. Its enhancements across DL/UL MIMO, AI/ML–driven PHY/MAC optimisation, evolved duplexing and RedCap evolution increase the architectural importance of modem‑RF integration and system‑level firmware. Devices that can expose predictable interfaces for AI offload and power‑aware scheduling will gain lead indicators of platform stickiness.

RF materials and amplifier transitions: GaN is already the dominant RF material in many modern telecom radio chains and is on track to extend toward the majority of RF shipments in mmWave and high‑power applications. This materially shifts supplier ecosystems and cost curves for front‑end modules.

Foundry and packaging constraints: Advanced nodes and high‑performance packaging (including HBM proximity and advanced TSVs) remain concentrated geographically. Policy interventions — notably CHIPS Act channeling large investments into advanced node capacity — are mitigating some supply risk, but access to leading nodes and specialised GaN/SiC facilities will remain a gating factor for many OEMs.

Concentration and ecosystem control: High CR3/CR5 ratios create a market where platform owners can accelerate ecosystem adoption via software, reference designs and certifications — effectively raising switching costs for OEMs and operators.

Our review of leading chipset and IP vendors shows differentiated go‑to‑market plays and near‑term catalysts that will re‑shape share dynamics in 2026.

Qualcomm Technologies, Inc. — Continues to cement a leadership position with end‑to‑end modem‑RF platforms and aggressive platform roadmaps. The launch of the X105 (positioned as Release 19‑ready with AI integration) signals a strategy of moving customers up the value chain by embedding capability earlier and capturing software monetisation opportunities. For partners, Qualcomm’s scale provides rapid device-reference momentum but also necessitates careful IP and differentiation planning.

MediaTek Inc. — Playing to strengths in cost‑effective integration and rapid feature adoption. Its T930 and related modems are examples of targeting high‑volume CPE/FWA and device OEM segments with integrated AI QoS functions. MediaTek’s approach can be an attractive collaborative option for OEMs pursuing faster time‑to‑market without the premium of incumbent flagship platforms.

Samsung Electronics — Leverages vertical integration (foundry, SoC, memory) and materials R&D (GAA, HBM) to offer differentiated high‑performance silicon. Samsung’s advantage is most pronounced where OEMs need tight integration between application processor workloads and modem stacks.

Broadcom Inc. — Focused on infrastructure and wideband radio SoCs, with recent interoperability work tying FPGA acceleration to scalable beamforming. Broadcom’s play is infrastructure‑centric and positions it for operator and neutral host deployments that demand throughput and low latency at scale.

GCT Semiconductor — Recent commercial shipments and qualification wins indicate that newer entrants can capture niche, high‑value applications (e.g., air‑to‑ground networks) with focused go‑to‑market strategies. Expect selective partnerships and white‑label opportunities.

Sequans Communications — Targeting the IoT and eRedCap transition with low‑power, certifiable modules and licensable IP. Their roadmap is attractive for device makers prioritising energy envelope and rapid certification for low‑cost connectivity.

Huawei Technologies — Remains a major infrastructure and vertical solutions supplier with deep system integration in areas like robotics and healthcare. Geopolitical and regulatory constraints vary by market, but Huawei’s integrated solutions will continue to be strategically relevant in many regions.

Intel Corporation — Focused on network processors and edge compute‑centric chipsets, Intel’s differentiation hinges on converged edge‑cloud stacks and operator partnerships where co‑design of compute and network functions is required.

Product launches and sampling (e.g., Qualcomm X105, MediaTek T930/M90) indicate that silicon innovation is front‑loaded and device OEMs will be qualifying multiple silicon platforms through 2026.

New commercial shipments from smaller vendors (e.g., GCT) validate faster qualification cycles for specialized applications, opening pockets of opportunity outside handset and CPE volume lanes.

Interoperability successes linking SoCs and FPGAs for wideband radios point to an architecture where silicon vendors must account for programmable acceleration and software toolchains as part of their value proposition.

PW Consulting’s full Worldwide 5G‑Advanced Chip Market report is structured as an operational playbook for 2026 decisions. Key deliverables include:

Market sizing and scenario models (2020–2032) with sensitivity analysis across adoption curves and pricing scenarios;

Detailed supplier and customer value‑chain maps, including manufacturing capability matrices and lead‑time risk scoring;

Competitive benchmarking and product readiness timelines for Tier‑1 and emerging suppliers, with go‑to‑market implications;

Technology readiness assessments for GaN, advanced nodes and packaging options, and recommendations on co‑investment thresholds;

Regulatory and policy impact matrix (including CHIPS Act implications and regional compliance pathways), plus a mitigation playbook;

Commercial models and negotiation playbooks for OEMs, operators and silicon vendors (pricing, revenue sharing, software licensing frameworks);

M&A and partnership screen with quantified fit‑scores and integration risks for potential acquirers and private equity investors;

Practical checklists and risk registers for production ramp, certification and field trials tailored to device class (handset, FWA/CPE, automotive, industrial IoT).

To respect competitive confidentiality and maintain the “preview” principle, this press release omits detailed regional, application and company‑level share tables. The full datasets and stratified market splits are accessible via the PW Consulting subscription portal.

Chipset vendors: Prioritise software certification and developer ecosystems alongside silicon roadmaps. Secure foundry and GaN capacity through multi‑year agreements and risk‑sharing arrangements.

OEMs and module makers: Adopt dual‑sourcing strategies for critical platforms, and use our vendor fit‑scores to accelerate qualification bets in H1 2026.

Network operators and system integrators: Target early trials on differentiated stacks (AI‑assisted QoS, evolved duplexing) to shape standards‑conformant feature prioritisation with vendors.

Investors and PE firms: Use our scenario cash‑flow matrices to underwrite investment pacing tied to contract milestones rather than calendar dates, given the concentration and capital intensity of the ecosystem.

2026 is the pivot year where strategic choices — about partners, capacity commitments, technology focus and monetisation models — will compound into decade‑long advantages or structural weaknesses. PW Consulting’s full Worldwide 5G‑Advanced Chip Market report provides the granular evidence, models and playbooks necessary to make those choices with confidence. For access to the complete report (including detailed regional and application splits, company share tables and downloadable model files), please visit the PW Consulting research portal or contact your account representative.

For detailed analysis of this topic, please visit the official page:Worldwide 5G-Advanced Chip Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com