Second-Life Automotive Battery Module Systems Market Estimated at USD 2.2 Billion in 2026, Forecast to Reach USD 9.4 Billion by 2036

Other |

2026-07-08 19:02:30

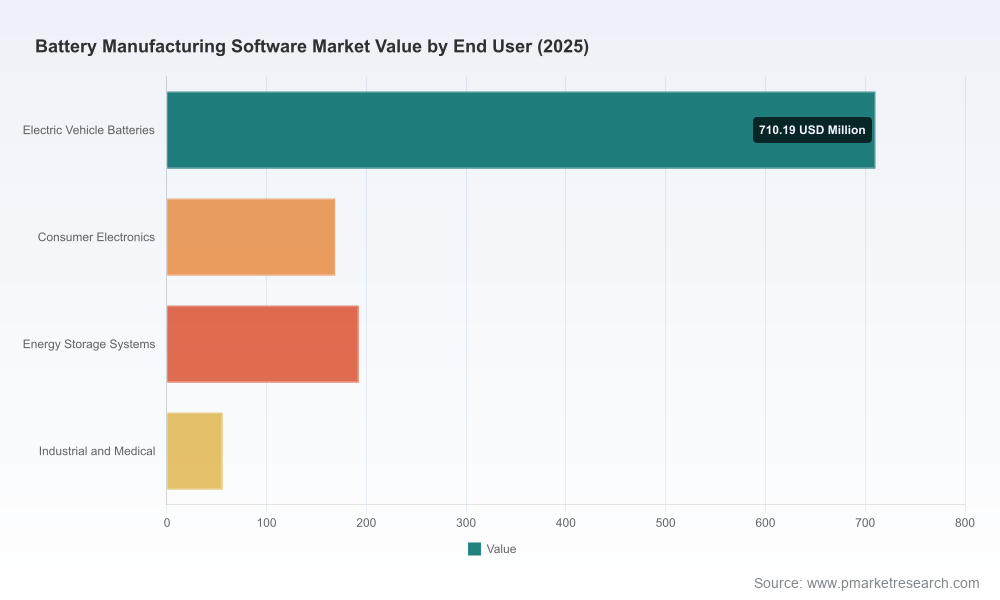

As global battery manufacturing scales from pilot lines to gigafactories, the software layer that orchestrates production, quality, analytics and compliance has become a strategic choke point. Our new Worldwide Battery Manufacturing Software Market study (base year 2025; forecast 2026–2032) shows that the market has moved well beyond early-adopter pilots into substantial commercial adoption: the market size in 2025 reached USD 1,127.29 Million and is on a sustained growth path (projected to expand at a compound annual growth rate of 18.24% across the 2026–2032 forecast period, reaching a multibillion-dollar opportunity by 2032). For corporate leaders planning 2026 capital allocations, vendor strategies, and production ramp roadmaps, this report serves as the operational playbook — combining market sizing, risk scenarios, vendor benchmarking, implementation playbooks and pragmatic ROI tools to inform immediate decisions.

Worldwide Battery Manufacturing Software Market

From compliance to cost control: regulatory requirements (for example, emerging battery passport regimes and tightening data-sovereignty expectations) are making traceability and auditable data flows a non-negotiable element of any manufacturing software strategy. Executives must embed compliance into their software selection process, not treat it as an add-on.

Worldwide Battery Manufacturing Software Market

Scale transformation risk: as facilities scale to gigawatt-hour outputs, software complexity and integration risk rise exponentially. The right software architecture determines whether a ramp-up is predictable or plagued by quality escapes and yield loss.

Worldwide Battery Manufacturing Software Market

Operational leverage: digital use cases that reduce labor needs (notably in high-throughput cell lines) and cut energy consumption in stages such as electrode production are material to per-kWh cost curves. Our analysis synthesizes third-party evidence that targeted digitalization use cases can reduce energy consumption significantly and incrementally reduce labor cost exposure across production lines.

Vendor landscape dynamics: a handful of global incumbents and a set of specialized analytics and battery-intelligence providers create a heterogeneous buyer market. Understanding functional coverage, integration models, and commercial packaging is essential to avoid costly rip-and-replace projects.

High-fidelity market sizing and scenario models. We quantify market trajectories under conservative, baseline and accelerated adoption scenarios for 2026–2032 and provide sensitivities tied to policy shifts, EV adoption curves and domestic manufacturing incentives.

Decision-ready vendor benchmarking. Our comparative matrices map vendor capabilities against nine functional dimensions (MES/MOM, simulation & design, quality management, asset performance, analytics/AI, traceability, cybersecurity, cloud/on-prem deployment and services). Profiles include strategic positioning and recent strategic moves to help shortlist vendors for pilots vs long-term strategic partnerships.

Implementation playbooks and KPI sets. For senior leaders and factory-level sponsors we provide phased roll-out blueprints, integration checklists and the KPI bundle to track during 0–6, 6–18, and 18–36 month horizons. This includes recommended metrics for yield improvement, scrap reduction, ramp lead time, and energy profile monitoring.

ROI and TCO models tailored to factory archetypes. Our templates allow finance and operations teams to stress-test investment cases under varying yield, scrap and energy-saving assumptions and to quantify payback horizons for software modules and professional services bundles.

Cyber and compliance readiness assessment. Practical requirements for secure updates, encryption standards, and architecture patterns aligned with ISO 21434 and IEC 62443 are provided, along with vendor checklist items for secure software lifecycle management (e.g., AES-256, TLS 1.3 where applicable).

The vendor map is a mix of industrial automation champions, software-first analytics specialists, and emerging niche platforms focused on battery intelligence. Leading industrial players are extending broad MES/MOM and digital-thread portfolios into battery-specific use cases; meanwhile, battery-focused software vendors are competing on domain expertise in cell and pack analytics and on their ability to bridge R&D and volume production datasets.

GE Vernova, Siemens, Rockwell Automation and ABB represent scaled MES/MOM incumbency with deep integration into OT stacks and a clear value proposition around end-to-end visibility, traceability and standardization in gigafactory environments.

Honeywell and Panasonic Connect have made headline moves with battery-specific MES and factory-excellence platforms to accelerate digital transformation at scale; recent product launches underscore their intent to own the operational layer of next-generation battery production.

Specialist analytics vendors such as Voltaiq, PDF Solutions, Energsoft and camLine (Elisa IndustrIQ) are competing on the quality of their battery-data models, analytics pipelines and ability to extract actionable signals from dispersed test and production datasets.

The market structure — neither a pure monopoly nor atomized — favors partnerships: strategic combinations of an MES leader plus an analytics/battery-intelligence specialist are emerging as the de facto approach to cover both OT integration and deep domain analytics without duplicative stack build.

Notable recent developments that shape 2026 choices: Honeywell launched its AI-driven Battery Manufacturing Excellence Platform (Battery MXP) to reduce startup material scrap and accelerate ramp cycles; Panasonic Connect introduced Syncora, an end-to-end MES aimed at U.S. EV battery manufacturing growth. These moves, together with ongoing policy action supporting domestic production, are accelerating vendor product roadmaps and commercial models — with implications for procurement timing and integration risk.

Prioritize modularity and interoperability. Require open APIs, conformance to industrial data standards, and vendor commitments for integration with cell testers, lab systems and energy-management platforms. Locking into proprietary stacks risks costly migration during scale-up.

Design two-track supplier strategies. Combine a proven MES/MOM partner for OT-critical operations with a domain-specialist for analytics. This reduces time-to-value and protects advanced analytics investments from OT dependencies.

Make compliance and traceability non-functional requirements. With battery passport regimes and carbon footprint reporting nearing mandatory status in several jurisdictions, traceability and data provenance must be built into deployment specifications.

Test yield & energy use cases first. Our field work shows that targeted investments in predictive quality and energy tracking produce disproportionate benefits: energy optimization use cases frequently deliver measurable consumption reductions (notably in electrode processes), while predictive quality workflows reduce staff-driven inspection load and limit scrap during ramp.

Run bounded pilots with commercial-style SLAs. Use 3–6 month sprints tied to measurable yield/throughput KPIs before enterprise rollouts. Include rollback and data migration pathways in every contract.

Invest in data architecture and talent. Establish a factory data lake strategy, decide cloud vs on-prem segmentation for sensitive datasets, and train cross-functional teams in data-literate manufacturing practices.

Calibrate M&A and partnership plays. For OEMs and large suppliers, acquiring or partnering with analytics specialists can accelerate time-to-insight. For software vendors, expanded services and systems-integration capabilities are a competitive differentiator.

The study maps the common value levers — yield improvement, scrap reduction, energy optimization, labor efficiency and faster ramp — to realistic adoption pathways and payback scenarios for factory archetypes. To illustrate the kind of operational impact found repeatedly in our primary research and corroborated by independent studies: energy-tracking and optimization program designs have demonstrable potential to materially reduce energy consumption in high-intensity stages; focused digitalization use cases can shave staff requirements and incremental production costs; and robust traceability implementation can simplify compliance workflows while reducing quality incident response times. (For decision-makers seeking the precise assumptions, scenario inputs and step-by-step ROI tables, the full interactive models are available with the report.)

Vendor selection and RFP design — tailored to pilot vs scale needs, with risk-weighted scoring and TCO modeling.

Implementation roadmaps — phased plans linking capability delivery to operational KPIs and financial milestones.

Cybersecurity & compliance audits — alignment with standards such as ISO 21434 and IEC 62443, plus actionable remediation roadmaps.

Integration and data-architecture advisory — mappings from factory OT to cloud analytics with hardened data governance patterns for traceability and IP protection.

Merger & acquisition diligence — technical and commercial assessment of target software/analytics assets and integration fit.

Conclusion — a 2026 imperative: the window for capturing disproportionately large manufacturing and cost advantages closes quickly as best practices and software capabilities commoditize. Organizations that move in 2026 with clear acceptance criteria, modular vendor architectures, compliance-by-design and measurable pilots will materially lower ramp risk and capture first-mover operational advantages. Our Worldwide Battery Manufacturing Software Market report provides the market intelligence, vendor insight and executable playbooks to make those decisions with confidence. For the full suite of interactive models, granular scenario tables and the complete vendor benchmarking database, access the report webpage to download the full research package and supporting tools.

For detailed analysis of this topic, please visit the official page:Worldwide Battery Manufacturing Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com