Vinyl Ester Market: Size, Share, and Future Growth

Other |

2026-03-18 03:56:42

PW Consulting’s latest Worldwide Mono Cartons Market report (base year: 2025) delivers an evidence-driven briefing designed to inform capital allocation, product strategy, and regulatory risk mitigation for 2026 and beyond. The mono cartons market has moved from a specialist packaging niche into a core strategic battleground for consumer-packaged goods, pharmaceuticals, and e‑commerce logistics. Our analysis situates the market within a clear macro trajectory: after steady expansion through the historical window (2020–2025), total market value stood at the 2025 base year (USD, revenue in Million), and the market enters the forecast horizon (2026–2032) with a compounded annual growth rate (CAGR) of 5.25%—a momentum profile that favors scalable, integrated suppliers and agile mid‑market converters prepared to serve sustainability-driven demand.

Worldwide Mono Cartons Market

Mono cartons are maturing from a cost‑efficient carrier to a strategic interface between brand experience, sustainability credentials, and circularity compliance. The market’s projected path—anchored by a 5.25% CAGR across 2026–2032—reflects multiple, reinforcing tailwinds: regulatory pushes toward mono‑material designs, premiumization in retail packaging, and the substitution of multi-material formats in liquid and frozen categories. For corporate planners, the implication is clear: invest now to capture share in a growing market, but align that investment with dynamic regulatory and raw‑material scenarios to avoid stranded assets.

Worldwide Mono Cartons Market

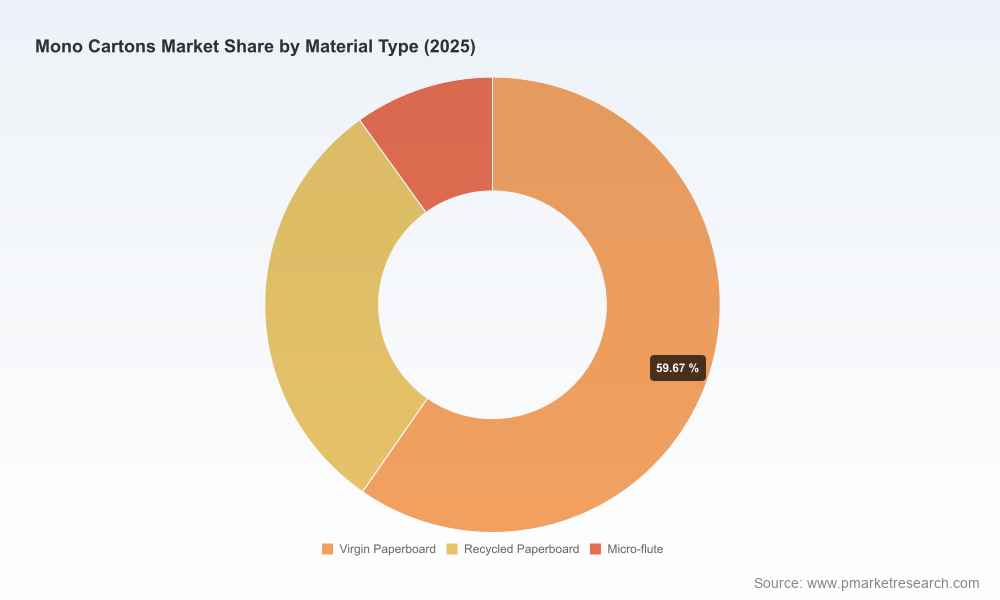

The market is segmented by region, material type, and end‑user verticals. Each dimension presents different strategic implications: material selection drives recyclability and cost profile; regional demand patterns influence supply chain design; and end‑user requirements determine technical specifications and value capture (e.g., barrier solutions for food vs. luxury finishing for premium consumer goods). To preserve the competitive integrity of our clients and guide subscription conversions, the public preview intentionally omits granular split values; the full report contains detailed, auditable segmentations and interactive tools for scenario modeling.

Worldwide Mono Cartons Market

Material economics are central to mono carton profitability. Solid bleached sulphate (SBS) — one of the primary substrates used in high‑grade cartons — is tracked by producer price indices that climbed into 2026; monitoring indices such as the US Bureau of Labor Statistics PPI (278.5, Jan 2026) should be part of any procurement dashboard. Recycled paperboard prices also tightened in 2025—Fastmarkets RISI reported an average near USD 850 per tonne in Q4 2025—reflecting supply chain constraints and higher collection costs. These inputs matter for converters and brand owners because they change the calculus around mono‑material adoption, printing and finishing choices, and end‑of‑life economics for closed‑loop programs.

Regulation is no longer a peripheral risk; it is a primary demand driver. In Europe, the Packaging and Packaging Waste Regulation (PPWR) has accelerated the move toward mono‑material designs and sets explicit recycled‑content ambitions. The UK’s Plastic Packaging Tax (applying a defined per‑tonne levy on non‑recycled plastic content) creates a cost asymmetry that favors paperboard solutions where feasible. Collectively, these regulatory levers alter product design requirements and supplier selection criteria—favoring mono‑carton constructions that can demonstrate recyclability and a credible recycled content roadmap.

The mono cartons ecosystem combines global pulp and paper majors, specialized board producers, and converters that bundle converting, finishing, and supply chain services. Selected players profiled in our analysis include:

Recent industry moves underline the strategic thrust toward sustainability and capacity expansion: for example, Mondi launched a high‑barrier mono material product in mid‑2025; WestRock showcased recyclable, e‑commerce‑optimized cartons at Pack Expo (April 2025); Smurfit Kappa announced FSC certification for recycled‑board ranges in March 2025; and Stora Enso commissioned a significant paperboard line in late 2024. These actions are directional signals: leaders are aligning upstream capacity and product capability with downstream sustainability requirements.

Q: What regulatory thresholds should companies prioritize in 2026?

A: Key enforcement themes to monitor include recycled content mandates and extended producer responsibility regimes. For example, China’s EPR requires minimum recycled content and establishes financial penalties for non‑compliance; other jurisdictions are tightening labelling and recyclability rules. Companies must map obligations at a country level and build compliance timelines into product roadmaps.

For firms making 2026 resource allocation decisions, the mono cartons market represents a growth opportunity married to regulatory complexity. PW Consulting’s report arms leaders with the intelligence to convert compliance into competitive advantage—by optimizing material mixes, securing resilient feedstock supply, and making targeted investments in capacity and capability. The public preview is designed to show you where the inflection points are; the full report supplies the segment-level data, interactive scenario models, and vendor scorecards you need to operationalize a winning strategy.

To access the complete Worldwide Mono Cartons Market analysis, including detailed segmentation, financial models, and the operational playbook, please visit our report page for subscribers and clients.

For detailed analysis of this topic, please visit the official page:Worldwide Mono Cartons Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com