Worldwide Hypersomnia Drug Market — Strategic Outlook for 2026 Decision‑Makers

PW Consulting today publishes its definitive market intelligence brief on the worldwide hypersomnia drug market, timed to inform executive decisions across biopharma, investors, and health‑system stakeholders as they set strategy for 2026. This executive summary presents the macro trajectory, near‑term catalysts, and the actionable strategic themes that will determine commercial success in a market undergoing simultaneous therapeutic innovation and intensified pricing pressure.

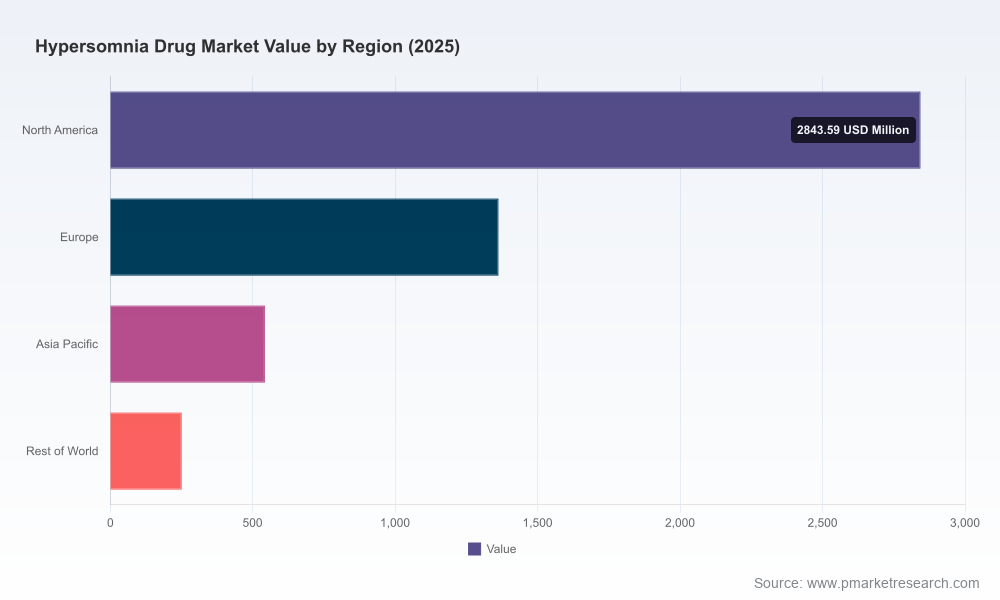

Worldwide Hypersomnia Drug Market

Market at a glance: growth trajectory and structural signals

The global hypersomnia drug market has moved from niche specialty demand to a fast‑growing therapeutic category. Our base‑year analysis (2025) estimates the global market at approximately USD 5.0 billion, and our forecast models project a compound annual growth rate (CAGR) of 10.5% through 2032. By the end of the forecast horizon the market is projected to exceed USD 10 billion under our central scenario. This growth reflects a convergence of drivers: new mechanism‑of‑action entrants (notably orexin receptor agonists), expanded label and off‑label clinical adoption for certain oxybate formulations, broader diagnostic recognition, and more sophisticated payer and provider pathways for hypersomnia disorders.

Worldwide Hypersomnia Drug Market

At the same time, concentration metrics indicate a market structure dominated by a handful of incumbent and late‑entrant players. That combination — rapid expansion with high concentration — creates asymmetric opportunity: meaningful commercial upside for successful new entrants, but significant downside for programs that misread access dynamics or underestimate pricing erosion from authorized generics and ANDA entrants.

Worldwide Hypersomnia Drug Market

Why this report is indispensable for 2026 planning

- Timing matters: 2026 is a fulcrum year. Several Phase‑3 readouts, new NDA/PDUFA milestones and strategic M&A moves are converging, creating windows of opportunity for licensing, defensive filings, or accelerated commercialization.

- Access complexity: regulatory constraints (e.g., REMS for certain oxybate products), controlled‑substance scheduling and payer reimbursement decisions will materially influence launch sequencing and revenue realization.

- Competitive displacement risk: authorized generics and full generics are already shifting the pricing baseline in some markets; companies must plan for immediate and sustained margin pressure post‑entry.

- Evidence imperative: payers and specialists increasingly require robust real‑world effectiveness and value demonstrations beyond classical clinical endpoints; early investment in pragmatic evidence generation is a gating factor for premium contracting.

Report contents — operational, decision‑ready deliverables

PW Consulting’s full report combines market analytics with executable playbooks developed from commercial due diligence engagements across CNS and rare disease portfolios. Key components include:

- Top‑down market forecasts and probabilistic scenario models (2026–2032) — central, upside and downside cases with sensitivity to pricing, uptake and regulatory outcomes.

- Product‑level launch planning tools — go‑to‑market timing, supply scaling matrices, REMS compliance checklists and channel strategies tailored to controlled substances and oral CNS agents.

- Payer & reimbursement playbooks — evidence requirements mapped to likely payer segmentation, value dossier templates and win/risk thresholds for different contracting strategies.

- Clinical & commercial risk frameworks — probability‑adjusted NPV models incorporating pipeline readouts, label expansion potential, and generic entry timing scenarios.

- Competitive intelligence dossiers — strategic positioning analyses for leading and emerging players, platform strengths, partnership fit, and likely defensive moves.

- M&A and licensing scorecards — checklist frameworks and valuation sensitivities for targets across development stages.

- Real‑world evidence (RWE) design blueprints — prescriber and patient cohort identification, endpoints aligned with payer needs, and pragmatic trial costings suitable for 12–18 month evidence windows.

Competitive landscape — thematic analysis (what to watch)

The market is shaped by a mix of established specialty pharma, generic manufacturers, biotech innovators, and near‑term strategic acquirers. Collectively, the top three to five organizations currently capture a dominant share of market value, a fact that raises entry barriers but also creates partnership opportunities for niche players.

- Specialty innovators: Companies marketing oxybate formulations and non‑stimulant wake‑promoting agents occupy advantaged positions through established clinician relationships, REMS infrastructure, and label breadth. Their strategic choices — defend premium pricing, pursue label extensions (e.g., idiopathic hypersomnia indications), or pursue line extensions — will dictate competitive posture.

- Generics & authorized generics: Recent ANDA approvals and authorized generic launches have already re‑set the affordability baseline in core markets. This trend reduces price elasticity for some segments but also expands volume potential by improving access.

- Next‑generation mechanism players: Orexin receptor agonists and selective OX2R candidates represent the most disruptive technical risk to incumbent molecules. Regulatory designations and breakthrough statuses granted to several developers reflect the clinical community’s appetite for differentiated symptomatic control.

- Strategic acquirers and capital flows: Recent acquisition activity demonstrates that larger pharma is positioning to own late‑stage orexin pipelines; this increases the probability of consolidation and accelerates timelines for commercialization scale‑up once approvals are secured.

For commercial teams, the implications are clear: defend market share where you have clinical or distribution advantage; pursue partnerships where scale or regulatory complexity exceeds internal capabilities; and invest in payer evidence to protect launch economics.

Near‑term catalysts and downside scenarios for 2026

Several concrete events and trends will define competitive dynamics through 2026:

- Clinical readouts and regulatory timelines: Phase‑3 completions and NDA/PDUFA milestones scheduled around mid‑2026 will create inflection points for labeling and access. Prepare modular launch plans that can be activated or deferred based on readout outcomes.

- M&A and pipeline consolidation: Strategic acquisitions of orexin programs and other CNS assets have accelerated, changing the competitive calculus for in‑licensing and cross‑border commercialization deals.

- Generic price pressure: The entrance of lower‑cost authorized generics alters payer negotiations and may force branded manufacturers to re‑price, increase rebates or pursue value‑based contracting.

- Regulatory and REMS complexity: Controlled‑substance scheduling and restricted distribution programs remain a persistent operational burden. Companies that master REMS logistics and compliance will secure a material advantage in distribution reliability and payer confidence.

Actionable recommendations for corporate leadership in 2026

- Prioritize investments in payer‑facing evidence now: Build RWE frameworks and cost‑effectiveness models before launch; timing is critical to win early formulary placement.

- Design flexible commercialization models: Outsource REMS administration or partner with experienced specialty distributors to reduce operational ramp risk and compliance cost.

- Model multiple price‑access outcomes: Maintain a suite of pricing and contracting playbooks, from premium specialty access to aggressive volume pricing with narrow networks.

- Accelerate M&A diligence on selective targets: With acquirers active, identify targets that unlock distribution, regulatory capabilities or complementary pipelines and prepare rapid diligence packs.

- Defend clinical footprint through label expansion: If you are incumbent on oxybate or wake‑promoting agents, invest in post‑approval evidence generating idiopathic hypersomnia data to preserve prescriber preference against new mechanisms.

- Invest in clinician and patient education: Differentiation will be partly behavioral — educate specialists and patients on comparative benefits, safety profiles and practical administration to accelerate adoption.

How to use PW Consulting’s full report (and what’s intentionally withheld here)

This release follows a “trailer” principle: we surface the strategic implications, timing windows and practical playbooks you need to evaluate decisions in 2026, while withholding granular segmented tables and product‑level forecasts that are proprietary to the full report. The complete analysis includes detailed regional and indication segmentation, product and formulation revenue splits, channel margins, and downloadable scenario dashboards used to stress‑test commercial plans.

If your team needs: (a) adjustable financial models ready for Board review, (b) competitor share maps at the molecule and country level, (c) payer contract templates and expected net price curves under multiple generic scenarios, or (d) a tailored M&A target shortlist with valuation sensitivities — the full report and our executive briefing sessions will provide these tactical deliverables.

Closing — the strategic imperative for 2026

As the hypersomnia drug market shifts from incremental therapeutic management toward mechanism‑based disruption, 2026 will reward organizations that combine clinical differentiation with pragmatic commercialization capability. PW Consulting’s analysis demonstrates that the upside is substantial, but so are the operational, regulatory and access hurdles. Companies that sequence their investments correctly — prioritizing payer evidence, REMS readiness, and flexible partner models — will convert the growing market into durable value.

For access to the full dataset, segmented forecasts and customizable scenario models that underpin these recommendations, request PW Consulting’s Worldwide Hypersomnia Drug Market report and schedule an executive briefing to align your 2026 corporate plan with the market’s most likely pathways.

For detailed analysis of this topic, please visit the official page:Worldwide Hypersomnia Drug Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com