Hazelnut market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-12 10:27:06

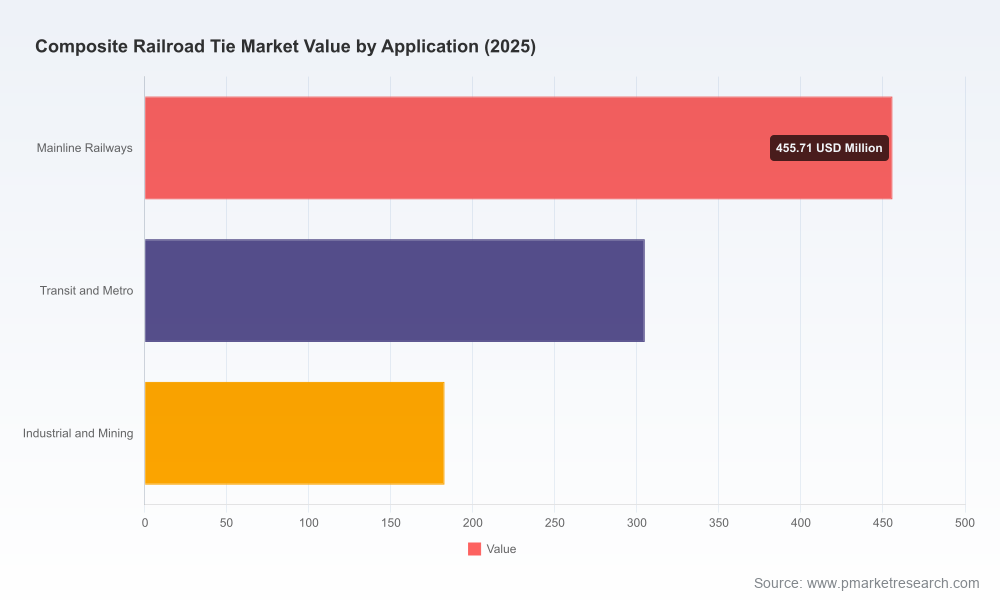

PW Consulting's new Worldwide Composite Railroad Tie Market report provides an indispensable strategic briefing for executives, procurement leaders, infrastructure investors and OEMs preparing actions in 2026 and beyond. The market for composite railroad ties has moved from a developmental niche into sustained commercial adoption: the market reached roughly USD 943 million in 2025 and, under the base-case forecast, is expected to expand at a compound annual growth rate (CAGR) of 6.12% through the 2026–2032 horizon, reaching about USD 1.43 billion by 2032. This preview outlines where value will be created, which capabilities determine winning positions, and how to convert field-trial momentum into repeatable commercial programs — while reserving the granular regional and application-level splits for the full report.

Worldwide Composite Railroad Tie Market

Proprietary market model and interactive scenario suite: a base-case and two stressed scenarios for demand, pricing and raw-material cost trajectories across 2026–2032, built from 2020–2025 historical calibration.

Worldwide Composite Railroad Tie Market

Lifecycle cost (TCO) analytic framework: standardized inputs and sensitivity levers that translate installation, maintenance, and disposal assumptions into procurement-ready TCO comparisons versus wood, concrete and alternative sleepers.

Worldwide Composite Railroad Tie Market

Supplier diligence pack: verified technology assessments, manufacturing footprint implications, approval and test-status trackers, and contract templates to accelerate trials and procurement.

Field-trial playbook and instrumentation protocols: KPIs, sampling plans, instrumentation suites and data collection templates that convert pilot installations into defensible, scalable decisions.

Regulatory and standards map: approval pathways and acceptance criteria for AREMA, AAR, Network Rail, and other national authorities — plus mitigation routes where local rules remain unclear.

Risk and resilience dashboard: raw-material dependency, recycling logistics, production lead-times and carbon-accounting scenarios to stress-test adoption strategies.

Policy and procurement shifts are changing the baseline. The withdrawal of creosote-treated softwood procurement by a major European infrastructure owner in 2024 has accelerated institutional openness to composite sleepers, and similar sustainability commitments are rippling across other jurisdictions.

Class I railroad programs and large-scale trials have matured from pilots to system-level validation. Recent multi-manufacturer installations under heavy-haul conditions showed installation compatibility with conventional replacement rates and near-term operational acceptability — creating a commercial window to scale.

Performance outcomes are converging with lifecycle promises. Several composite designs now meet or exceed AREMA strength/stiffness thresholds and some products have achieved AAR certification and manufacturer claims consistent with multi-decade service lives in high-decay environments — changing the math of replacement cycles and maintenance budgets.

Capital flows and partnerships are realigning the supply base. Strategic investments and commercial agreements announced in 2025–2026 are reducing execution risk for scale projects while creating new competitive concentrations in distribution and OEM access.

Make procurement decisions on lifecycle grounds, not first-cost. Use the report’s TCO model to quantify avoided maintenance, reduced possession time and environmental liabilities. The model is pre-populated with industry-validated degradation curves and field-trial outcomes to accelerate internal approvals.

Prioritize approvals and testing early. For projects intending to move beyond short-term pilots, secure pathway commitments from relevant authorities (AREMA/AAR/Network Rail or national equivalents) before committing to long-lead manufacturing orders — the report includes template test matrices keyed to jurisdictional acceptance.

Lock raw-material and recycling supply links. Composite solutions that scale require reliable post-consumer plastic feedstock and glass-fiber reinforcement supplies. Mitigate price and availability volatility by structuring offtake or upstream investments, co-locating processing with recycling hubs, or engaging toll-processing partners.

Leverage strategic partnering over one-off procurement. Commercial agreements that integrate materials expertise with distribution and engineering reach — for example, OEM-supplier commercial tie-ups — materially shorten time-to-deployment and reduce commercial friction. The report analyzes recent partnership archetypes and their implications for market access.

Design pilots with clear scale gates. Use the provided field-trial playbook to define objective go/no-go criteria (installation rates, tamping/maintenance compatibility, vibration and track geometry stability, and long-term degradation indicators) so pilots can convert quickly to volume contracts.

The competitive set blends long-established specialty manufacturers, advanced-material newcomers, and engineering/distribution giants. Key strategic archetypes include vertically-integrated recyclers-turned-manufacturers, long-tenured composite specialists with established approvals, and multi-product rail incumbents adding composite capabilities through partnership or acquisition.

Evertrak LLC (St. Louis, Missouri) — Known for a GFRP-based product designed for heavy-haul conditions; claims AAR certification and installations attesting to long service life. Strategic investor involvement has increased production upside for North America.

Sicut Enterprises (UK, with US operations) — Benefit from full product approvals with major national rail authorities and established metro procurements; attractive where regulatory alignment and warranty track records are decisive.

Pioonier GmbH (Germany) — Technology focus on recyclable plastic processing and an emphasis on European durability and sustainability requirements.

TieTek (EFG TieTek, Houston) — A market veteran with a long track record supplying composite ties and crossings; represents the incumbent-innovator class that institutional buyers recognize for reliability.

AGICO (China) — Cost-competitive manufacturing and metro system references across Asia make AGICO an important player for high-volume and price-sensitive projects.

Triton Group and Progress Rail partnership — A 2026 commercial agreement combining Triton’s materials with Progress Rail’s global sales and integration capabilities exemplifies the consolidation of technology and distribution power that will shape large-scale adoption.

Other notable players — Lankhorst, Sekisui, Axion (ECOTRAX), IntegriCo, and Vossloh — represent regional strengths, legacy product lines and complementary capabilities in concrete/composite portfolios.

The market is neither atomized nor tightly concentrated: a handful of technology leaders and regional champions collectively command strong positions while meaningful share remains accessible to challengers with demonstrable approvals, manufacturing scale or supply partnerships. For investors and corporate development teams, three themes emerge:

Buy access to approvals and distribution, not just product lines. Acquiring or partnering with firms that hold national approvals or strategic OEM relationships accelerates market entry and shortens payback.

Invest in circularity as a defensible moat. Control over recycled feedstock and end-of-life recyclability increases margins and reduces exposure to raw-material swings; it also aligns with procurement criteria tied to carbon and circular-economy objectives.

Consider bolt-on manufacturing to capture margin and secure lead-times. Near-term delivery capability is increasingly important for winning phased mainline replacements and transit projects.

Raw-material volatility: lock long-term offtake arrangements or co-invest in recycling capacity to stabilise input costs and ensure quality.

Standards divergence: actively track jurisdiction-specific acceptance criteria and fund joint testing programs to avoid fractured specifications that increase project complexity.

Installation and maintenance integration: ensure contractor training, tamping tool compatibility and signaling interface testing are included in contracts to avoid hidden lifecycle costs.

Recycling and end-of-life logistics: design closed-loop or take-back programs into contracts to preserve sustainability claims and avoid future disposal liabilities.

Clients use the report in five practical ways: to prioritize procurement pipelines by TCO advantage; to build supplier scorecards and negotiation levers; to scope pilot programs with measurable commercialization gates; to inform M&A and investment screening; and to integrate composite-tie strategies into broader decarbonization and asset-management plans. The deliverable set includes a ready-to-run TCO spreadsheet, field-trial templates, an approval-status matrix and a shortlist of vetted suppliers mapped to typical project archetypes.

Operational teams should commence two parallel streams in 2026: (1) a 12–18 month pilot program using the supplied playbook and (2) commercial negotiations to secure conditional production capacity with preferred suppliers, protecting schedule while retaining optionality.

Finance and strategy should stress-test capital allocations against the report’s scenarios to determine optimal timing for larger-scale replacements or factory investments.

Procurement should require lifecycle TCO submissions in all forthcoming tie solicitations and use the report’s RFP templates to standardize comparisons across technologies.

PW Consulting’s full report contains the granular market splits, country and application breakdowns, supplier scorecards and downloadable decision-support models that will operationalize the points summarized here. For teams preparing 2026 budgets, pilot programs and strategic partnerships, this report is the tactical field guide that turns field-trial momentum into durable procurement and investment choices.

For detailed analysis of this topic, please visit the official page:Worldwide Composite Railroad Tie Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com