Worldwide Industrial Flexible Hose Market: Strategic Imperatives for 2026 — PW Consulting Insight

Executive snapshot

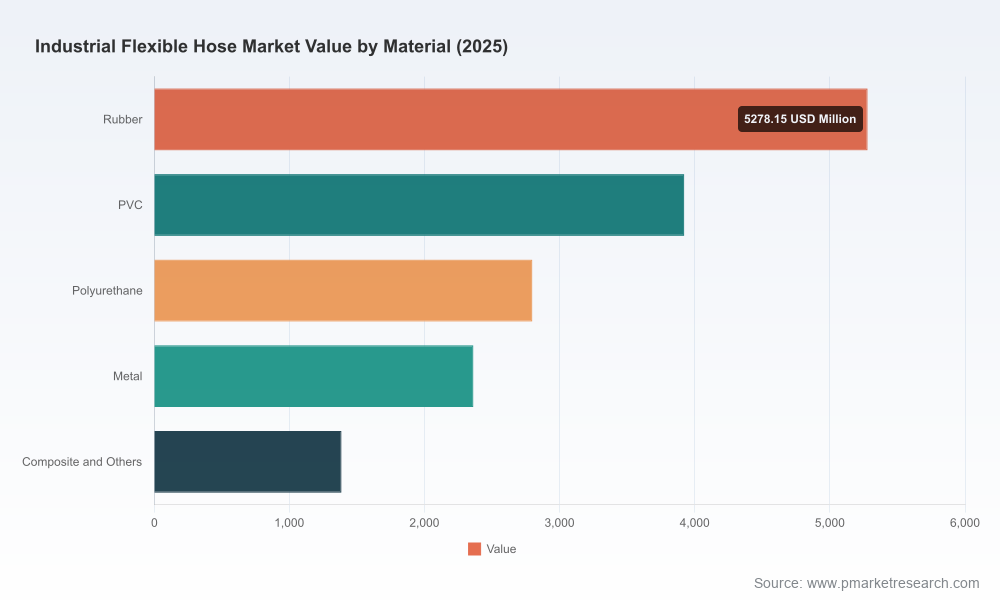

The industrial flexible hose market completed a steady recovery and expansion cycle through the first half of this decade, rising from USD 12,050.4 Million in 2020 to USD 15,744.0 Million in 2025. Our latest modelling projects a near-term step-up to USD 17,073.14 Million in 2026 and a continuation of steady expansion through 2032, with a compound annual growth rate of 5.12% over the 2026–2032 forecast window (ending at an anticipated USD 22,331.23 Million in 2032). These headline numbers belie a market that is simultaneously mature, technologically active, and structurally fragmented — conditions that create specific strategic opportunities and risks for manufacturers, distributors, and industrial users heading into 2026.

Worldwide Industrial Flexible Hose Market

Why the 2026 planning cycle needs this market view

- Capital allocation: companies deciding where to invest R&D, capacity, or M&A capital need forward-looking demand trajectories tied to real capex flows (notable oil & gas reinvestment plans are a key driver), and the report maps those flows to hose demand profiles.

- Cost and margin management: raw-material dynamics (rubber, PTFE/resins and other polymers) and labour-cost shifts materially affect unit economics; procurement and pricing strategies must be recalibrated for 2026.

- Regulatory and standards alignment: new and revised standards affect product specifications, warranty exposure and certification costs — all of which should be baked into product roadmaps and tender responses for 2026 contract cycles.

- Route-to-market and aftermarket: with increasing premiumisation and serviceable lifecycle revenues, go-to-market choices (direct vs distribution vs service) will determine margin capture in the medium term.

What the PW Consulting report delivers — practical, transaction-ready content

This report was written as a decision tool for corporate leaders. It combines rigorous market sizing with executable frameworks and toolkits:

Worldwide Industrial Flexible Hose Market

- Transparent sizing and methodology: full historical series (2020–2025) and granular forecasting routines (2026–2032) with adjustable inputs so teams can re-run scenarios against alternate macro assumptions.

- Demand-supply model and cost curves: end-user demand drivers mapped to manufacturing steps, with a calibrated cost build-up (raw material, labour, overhead, freight) to estimate true landed cost per hose family.

- Raw-material sensitivity analysis: scenario runs showing P&L and margin exposure to swings in key inputs. Our analysis highlights that natural rubber and fluoropolymer inputs are primary volatility levers for many constructions.

- Standards and compliance playbook: assessment of ISO and industry-specific standards (including the implications of ISO 1436:2022) and practical steps to de-risk certification timelines for 2026 tenders.

- Commercial toolkits: price-indexing templates, aftermarket service contract templates, OEM vs aftermarket margin matrices, and channel optimization blueprints tailored to different company types.

- M&A and partnership shortlist: a prioritized list of acquisition and JV targets with strategic rationales, integration risk checklists and likely valuation ranges (proprietary model outputs available in the full dossier).

- Supplier heatmaps and procurement playbook: dual-sourcing scorecards, inventory policy adjustments and hedging strategies for polymer and PTFE exposure.

To preserve the value of the proprietary segmentation models and to drive direct engagement, the report intentionally withholds the full set of granular regional and end-user splits from this summary; prospective clients can access these tables via the report page or by contacting PW Consulting.

Worldwide Industrial Flexible Hose Market

Market dynamics that will shape decisions in 2026

- Raw material volatility: natural rubber supply tightening pushed prices to approximately USD 1,800/metric ton by Q4 2024, and PTFE resin prices climbed to roughly USD 12,500/metric ton in 2024 — both trends directly compressing margin for conventional rubber and fluoropolymer constructions unless mitigated.

- Standards and certification: the ISO 1436:2022 revisions increase testing and documentation requirements for rubber hose assemblies operating with petroleum-based hydraulic fluids — a near-term compliance cost that also creates differentiation opportunities for certified suppliers.

- Macro capex pockets: elevated global oil & gas capex (projected at near USD 500 billion in 2025) and ongoing industrial investment cycles in heavy equipment and processing sectors will continue to underpin demand for specialized, chemical-resistant and high-pressure hoses.

- Input-cost and labour pressure: manufacturing wage inflation (for example, US hose-assembly labour rates climbed to about USD 28.50 per hour in 2024, a ~4.2% increase year-over-year) will push manufacturers to redesign processes or reallocate production footprints.

- Technology convergence: hybrid constructions, PTFE-lined assemblies, and metal-composite combinations are gaining adoption where durability, temperature and chemical resistance justify premium price points.

Competition and consolidation: what the leading players are doing

The sector is fragmented — the three largest suppliers account for roughly 18.5% of market revenues while the top five represent just over 28.1% — a structural fact that shapes strategic choices (scale matters for R&D and distribution, but local specialization wins many OEM contracts).

Key competitive positions and tactical moves to watch:

- Gates Corporation (Denver, USA): a global leader in rubber and thermoplastic hose solutions, with strong product breadth across hydraulic, air and chemical transfer. Gates’ recent product introductions for mining highlight a playbook of material science-led differentiation and aftermarket focus.

- Parker Hannifin (Cleveland, USA): excels in high-pressure fluid power systems and has invested in thermoplastic abrasion-resistant lines — product launches aimed at mining and construction indicate continued emphasis on durable, low-maintenance assemblies for heavy equipment OEMs.

- Eaton Corporation (Dublin, Ireland): through Aeroquip and Weatherhead, Eaton focuses on heavy-duty and mobile hydraulics segments; its recent trade-show activity signals supply-chain and channel consolidation efforts targeted at major equipment OEMs.

- Continental AG (Hanover, Germany): ContiTech’s strength is in process-industry hoses for chemical and food applications — its scale in industrial polymers and broad customer base gives it advantage in specification-driven markets.

- Trelleborg Group (Trelleborg, Sweden): plays the high-performance niche (PTFE-lined, high-temperature, corrosive media) and is investing visibly in subsea and offshore solutions; hybrid constructions are a signature area of innovation.

- European specialists (Alfagomma, Manuli, Aflex) and regional champions (Yokohama, Bridgestone, Ryco, Pacific Hoseflex, Novaflex, Goodall): these companies win on technical fit, responsiveness and local service — they are the most likely targets for strategic partnerships or bolt-on acquisitions.

Recent product and trade-show moves (new thermoplastic abrasion-resistant series, hybrid subsea hoses, high-burst-pressure mining hoses) confirm that incumbents are pushing both performance and aftermarket propositions. For buyers and investors, these signals indicate where premium margins and contract wins will concentrate in 2026.

What leaders should do in 2026 — prioritized action plan

- Protect margins through procurement playbooks: implement polymer-indexed contracts, expand qualified second-source suppliers, and use strategic stockpiling for critical inputs where financially prudent.

- Accelerate product premiumisation: prioritize hybrid and PTFE-lined offerings for corrosive and high-temperature niches; bundle warranties and maintenance contracts to capture lifecycle revenue.

- Service-first GTM: convert transactional aftermarket sales into subscription-style service agreements with predictive maintenance enabled by sensor retrofits or partner telemetry platforms.

- Targeted M&A and partnerships: pursue bolt-on acquisitions to consolidate distribution in key geographies, and partner with resin suppliers to secure preferential allocations or co-development programs.

- Compliance and certification roadmap: fast-track ISO 1436:2022 aligned product lines and pre-certify assemblies for major oil & gas and industrial OEMs to shorten procurement cycles.

- Manufacturing footprint optimization: evaluate near-shoring and automation investments to offset labour inflation and reduce lead-times for critical OEM contracts.

Scenario outlook and strategic contingencies

Our scenario framework models three plausible 2026 pathways: a baseline that follows central oil & gas and industrial capex assumptions (consistent with the 5.12% CAGR to 2032 embedded in our central forecast); an upside in which accelerated energy and infrastructure spends amplify demand for premium subsea and chemical-resistant hoses; and a downside where raw-material shocks and protectionist trade measures compress margins and slow replacement cycles.

For each scenario we provide actionable contingency plans — from dynamic pricing clauses and hedging strategies to rapid capacity reallocation playbooks — so that management teams can move from tactical response to strategic advantage within a single planning cycle.

Next steps and how to use the report for 2026 planning

PW Consulting’s Worldwide Industrial Flexible Hose Market report is designed as a working tool for executive committees, corporate development teams, procurement and product leaders. The full report includes the proprietary segmentation tables, company dossiers, M&A candidate valuations and an interactive model you can license for internal planning.

To access the complete dataset, detailed regional and end-user splits, or to commission a bespoke workshop translating these findings into a tailored 2026 action plan, please contact PW Consulting via our website or your client engagement lead. The market is moving from commodity competition to engineered resilience — early, well-calibrated decisions in 2026 will determine who captures the higher-margin growth available through 2032.

For detailed analysis of this topic, please visit the official page:Worldwide Industrial Flexible Hose Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com