Mahadev Book - Get Instant Access To Top Betting Markets And Games

Games |

2026-04-21 12:21:27

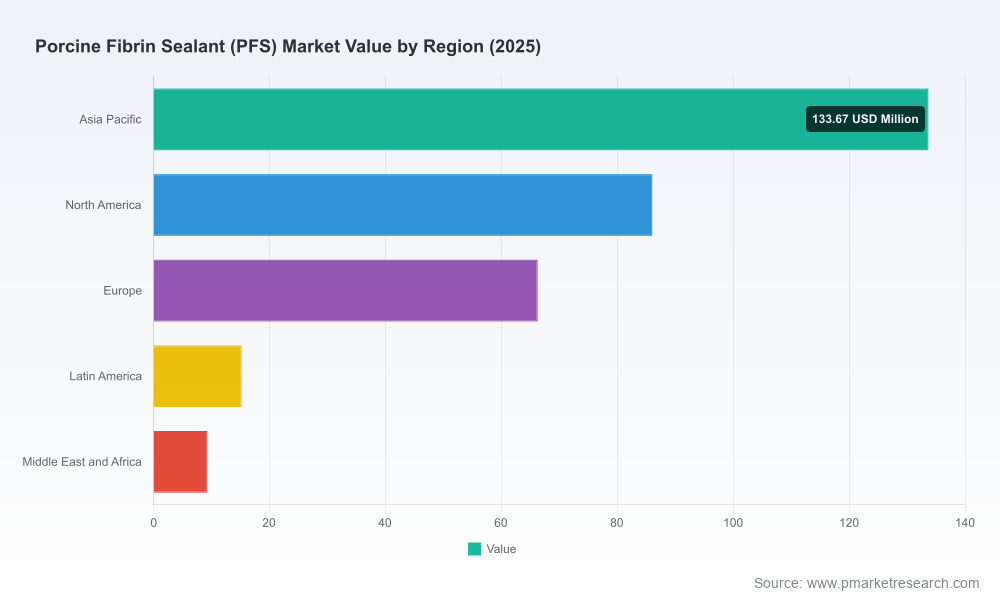

PW Consulting’s newest market intelligence, the Worldwide Porcine Fibrin Sealant (PFS) Market Report (base year 2025), delivers a strategic roadmap for executive teams preparing to make high‑stakes commercial, clinical and regulatory decisions in 2026. The report synthesizes a five‑year historical baseline (2020–2025) and a forward forecast window (2026–2032) to quantify market momentum: global PFS market value rose from USD 220.15 Million in 2020 to USD 310.5 Million in 2025, and under our central scenario is projected to expand to USD 505.15 Million by 2032, reflecting a compound annual growth rate (CAGR) of 7.2% across the forecast period.

Worldwide Porcine Fibrin Sealant (PFS) Market

Acceleration of surgical demand and constrained hospital budgets are reshaping procurement priorities. PFS products are increasingly evaluated on a blend of clinical efficacy, time‑to‑hemostasis, inventory footprint and overall episode cost rather than unit price alone.

Worldwide Porcine Fibrin Sealant (PFS) Market

Regulatory and reimbursement inflection points—most notably how jurisdictions handle zoonotic risk mitigation and virus‑inactivation validation—will determine which offerings can access public hospitals at scale and qualify for favorable insurance negotiation pathways.

Worldwide Porcine Fibrin Sealant (PFS) Market

Consolidation dynamics and localized champions are altering competitive playbooks. Our concentration analysis shows a market where the top three players control a substantial majority (CR3 ≈ 68.45%), and the top five drive an even larger share (CR5 ≈ 84.2%), creating both competitive barriers and selective partnership openings.

The report is built for action. Beyond headline market sizing and forecasts, PW Consulting provides:

Transparent methodology and a reconciled historical time series (2020–2025) that allows clients to reproduce core outputs and test alternative scenarios.

Commercial playbooks: hospital procurement decision trees, prioritized clinical specialties for pilot programs, and templated value dossiers tailored to national payer archetypes.

Regulatory and market‑access maps: country‑level approval pathways, required virus‑inactivation evidence, and negotiation levers for public hospital formularies.

Supply‑chain and raw‑material risk models: sensitivity analyses addressing porcine plasma availability, processing capacity, and price volatility.

Clinical evidence gap analysis and an investment matrix to prioritize randomized trials, registry builds, and real‑world‑evidence programs that accelerate adoption.

Competitive due diligence templates and M&A scenario planning, including valuation drivers, integration risks and post‑merger synergies specific to biologic sealants.

PFS is served by a mix of domestic champions and multinational entrants; each profile implies distinct go‑to‑market choices.

Shanghai Haohai Biological Technology Co., Ltd. — Positioned as an agile domestic innovator, Haohai’s Kangrui Gel (porcine fibrin sealant kit) achieved notable early commercial traction. The product’s inclusion in Shanghai’s New and Quality Medical Devices catalog opened a green channel for hospital access and positioned the company for priority local reimbursement talks. These moves accelerated initial revenue generation and illustrate how regulatory and procurement designations can materially change adoption curves in key provinces.

Guangzhou Bioseal Biotech Co., Ltd. (acquired by Johnson & Johnson/Ethicon) — The acquisition pathway highlights multinational strategies to acquire locally validated biologics with established clinical records. Bioseal’s virus‑inactivated porcine plasma technology and documented use in neurosurgical and vascular settings make it a high‑value component for global portfolio rationalization and cross‑selling into broader surgical franchises.

Guangzhou Beixiu Biotechnology Co., Ltd. — As a regionally focused supplier, Beixiu exemplifies product portfolio breadth that addresses surgical hemostasis and anastomotic sealing, often bundled into combination tissue repair strategies. Such firms remain attractive partners for OEM supply, private label agreements and distribution alliances.

Guangzhou Baisew Biological Technology Co., Ltd. — Baisew’s kits, applied in minimally invasive pelvic and single‑port procedures, underscore the importance of procedural fit and operating‑room efficiency. Targeting specific surgical sub‑procedures where PFS delivers measurable OR time savings is a proven pathway to formulary adoption.

The reported CR3 and CR5 concentration metrics signal a market with dominant incumbents but meaningful whitespace for challengers that combine clinical evidence, favorable regulatory status, and targeted commercial execution. Entry barriers include validated virus‑inactivation processing, GMP manufacturing for plasma‑derived inputs, and the ability to sponsor clinical data that addresses high‑stake indications (e.g., dural closure, vascular anastomosis). Where multinational players acquire local innovators, expect acceleration in procurement access through established hospital networks.

Market access accelerants: Catalog inclusion and local reimbursement pathways materially shorten hospital adoption timelines. Firms that secure provincial or national catalog status in 2025–2026 will gain disproportionate momentum.

Clinical differentiation: Evidence that demonstrates reduced re‑operation, shorter OR times, or lower overall episode cost will be decisive for adoption among cost‑sensitive buyers.

Supply resilience: Manufacturing scale and validated virus‑inactivation workflows are non‑negotiable for sustaining hospital contracts and avoiding adverse safety perceptions.

Partnerships over pure organic scale: For many players, distribution alliances, OEM supply, or acquisition by global surgical platforms represent faster routes to national formulary inclusion than building commercial infrastructure from scratch.

We translate insights into six priority actions for executive teams planning capital allocation, commercial launches or competitive defense in 2026:

Lock down market‑access levers early: Prioritize catalog submissions and local‑payer negotiations in target provinces where green channels exist; design dossier evidence to align with purchaser KPIs.

Invest in validated virus‑inactivation and supply chain traceability: Certify processes, publish validation data and build supplier redundancy to neutralize zoonotic and supply‑disruption concerns.

Design indication‑specific RWE pilots: Deploy short, high‑impact pilots in 2–3 surgical specialties that influence hospital pharmacy & therapeutics committees; record OR time, transfusion rates and downstream cost impacts.

Use price architecture strategically: Move beyond unit price to bundled episode pricing or OR‑efficiency guarantees to align incentives with hospital buyers.

Target M&A and partnership windows: Evaluate acquisitions of regional players that offer regulatory access or manufacturing capacity; conversely, consider divestiture of non‑core biologic assets to focus R&D capital.

Scenario‑proof your plan: Build short‑ and medium‑term playbooks for tightening regulation, pricing pressure and raw‑material scarcity—each with clear triggers and response budgets.

Three downside scenarios deserve boardroom focus:

Regulatory tightening: Acceleration of virus‑inactivation standards or more stringent zoonotic controls could delay approvals and raise unit production costs.

Raw‑material shock: Disruptions in porcine plasma supply, whether from animal health issues or export controls, would favor vertically integrated manufacturers and could compress margins for others.

Competitive substitution: Advances in synthetic sealants or increased availability of human‑plasma derived options could cap pricing and slow adoption if clinical differentiation is not sustained.

By 2026, the PFS market will reward organizations that combine a defensible regulatory position, a targeted clinical evidence strategy, resilient supply chains and tactical commercial plays that reflect hospital purchasing economics. PW Consulting’s report equips leaders to quantify these tradeoffs, prioritize investments and identify partnership opportunities—without requiring them to guess the underlying segmented data.

The above is a high‑level distillation of our comprehensive analysis. The full report contains the granular models, segmented forecasts, country‑by‑country regulatory and reimbursement matrices, and downloadable financial scenarios that institutional buyers use to set 2026 budgets and M&A targets. For subscription and licensing information, or to arrange a bespoke briefing with our life‑sciences strategy team, visit our report landing page or contact your PW Consulting account lead.

For detailed analysis of this topic, please visit the official page:Worldwide Porcine Fibrin Sealant (PFS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com