Electric Trucks Market Leaders and Key Company Profiles

Art |

2026-06-10 07:50:40

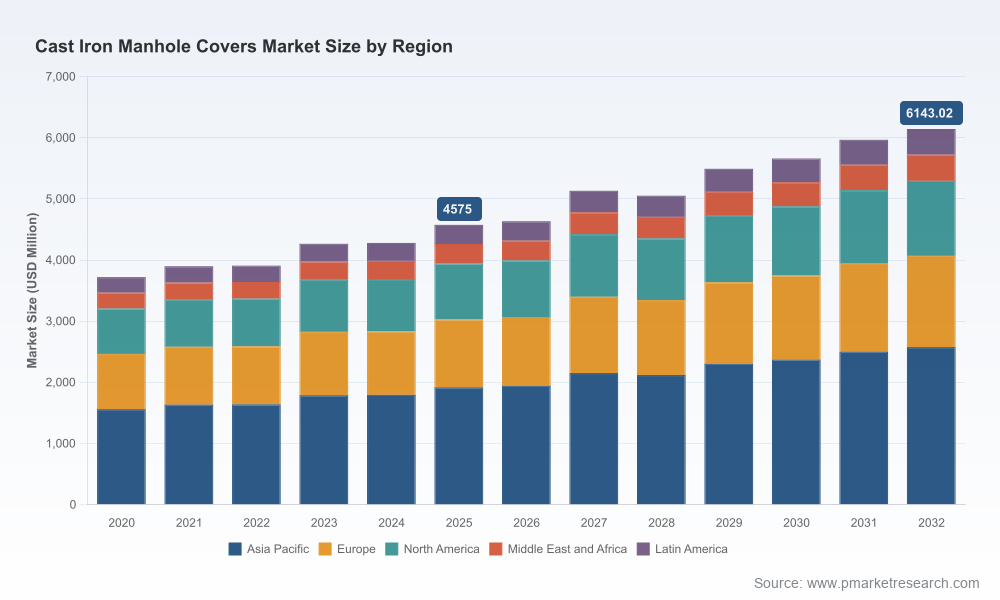

PW Consulting’s latest market study on the Worldwide Cast Iron Manhole Covers Market provides a forward‑looking framework to guide capital allocation, procurement, and go‑to‑market choices in 2026. The total market has continued to expand through the mid‑2020s and is projected to maintain steady compound annual growth (CAGR) of 4.3% over our 2026–2032 forecast window. Our base‑year analysis (2025) and granular scenario work are designed to convert industry complexity into executable options for manufacturers, infrastructure owners, and investors — without giving away the proprietary segmentation that underpins our valuation. This press release outlines the strategic insights buyers and suppliers need now, while reserving the full data tables and breakouts for the full report.

Worldwide Cast Iron Manhole Covers Market

Infrastructure renewal cycles in mature markets and accelerating urbanization in emerging markets continue to underpin demand for heavy‑duty manhole covers and frames.

Worldwide Cast Iron Manhole Covers Market

Medium‑term growth is durable: after a measured rebound in the early 2020s, the market is forecast to progress with low‑to‑mid single digit CAGR through 2032 — a profile that favors disciplined manufacturers and service providers who optimize cost, standards compliance, and aftermarket service.

Worldwide Cast Iron Manhole Covers Market

Market structure remains fragmented: the leading manufacturers collectively account for a modest share of global revenue, leaving sizeable regional and product niches open to focused entrants and roll‑up strategies.

Our topline metrics tell a simple story: steady expansion, predictable demand drivers, and persistent margin pressure from raw material volatility. The industry’s expansion path through 2025 establishes a reliable base for 2026 investment planning, but competitive advantage will not come from volume alone. Strategic differentiation will be driven by supply chain resilience, product specification leadership, and the ability to meet evolving standards and climate‑resilient requirements.

The full report is deliberately practical. It is organized to support immediate decision workflows in procurement, manufacturing planning, and corporate development:

Transparent market sizing and validated forecasts (base year 2025) to underpin budget and capacity decisions.

Scenario analyses modelling upside and downside demand drivers — including utility capex cycles, urban drainage programs, and reconstruction following extreme weather events.

Supply chain and input cost intelligence, with stress tests tying raw material price moves to margin outcomes under multiple procurement strategies.

Regulatory and standards mapping (regional and international), highlighting compliance pathways and certification timelines that materially affect tender eligibility.

Practical vendor selection and specification checklists for municipal and industrial procurement teams, reducing bid rejection and warranty risk.

M&A playbook: target profiles, integration priorities, and near‑term value capture levers for serial acquirers seeking to consolidate a fragmented field.

Producers face two immediate levers: raw material exposure and standards compliance. Recent data points illustrate the input price dynamic: cast iron scrap price indices have shown upward movements in early 2026, contributing to margin squeeze for foundries operating on fixed‑price contracts. Similarly, steel and scrap market cycles — evidenced by mill capacity utilization in the 75–80% range during much of 2025 — have amplified input volatility.

Recommended tactical responses for 2026 include hedged procurement contracts, forward scrap purchasing pools for aggregated small producers, and targeted CAPEX for in‑house scrap processing where G&A thresholds permit. These moves protect cashflow while delivering differentiated uptime and delivery reliability to major municipal customers.

Standards continue to be foundational to procurement and acceptance. European and national standards remain the primary gatekeepers for heavy‑traffic applications, and mandatory certification regimes in select markets (for example, national standards applicable in South Asia) create entry barriers that are both a challenge and an opportunity for compliant producers. At the product level, successful incumbents are pushing climate‑resilient and anti‑dislodgement designs into RFP specifications — a trend that will accelerate as extreme weather events become a procurement consideration.

The competitive map is diverse: global incumbents, regional specialists, and export‑oriented foundries coexist across multiple geographies. The report profiles key companies that set product, quality and distribution benchmarks. Among those we track closely are established North American manufacturers known for durable municipal products; large family‑owned foundries in South Asia with extensive export networks; and focused producers in the Gulf and Europe that combine regional distribution with customization capabilities.

Leading companies are deploying three common playbooks: product engineering to meet high load‑class standards; localized manufacturing to shorten lead times and reduce freight exposure; and channel partnerships to secure long‑term municipal and utility contracts. The report includes company profiles, recent strategic moves, and capability maps that allow executives to benchmark their own operations without exposing our underlying market math in this public summary.

New product introductions focused on climate resilience and ease of installation indicate procurement teams increasingly demand value beyond commodity castings.

Trade show participation and expanded export activity among several large foundries demonstrate ongoing appetite for international market share gains, even as local content rules in some jurisdictions complicate bidding strategies.

Input cost volatility, captured in recent producer price indices and mill utilization reports, is prompting manufacturers to reassess margin management and to accelerate productivity investments.

Reprice and renegotiate: Revisit long‑term contracts with indexed pricing or pass‑through mechanisms where exposure to scrap and steel is material.

Certify and differentiate: Prioritize certification pathways that unlock preferred supplier status in high‑value municipal programs and industrial tenders.

Localize selectively: Evaluate micro‑plant or toll‑manufacturing options in target regions to reduce lead times and comply with local procurement rules.

Pursue bolt‑on acquisitions: Target small, regional foundries with stable municipal relationships and under‑utilized capacity to accelerate market share and distribution.

Invest in extensions: Add services (installation training, warranty management, post‑sale inspection) to convert one‑time sales into multi‑year relationships with infrastructure owners.

Key downside risks to the base forecast include sustained raw material inflation, sudden shifts in procurement specifications favoring alternative materials, and concentrated competition in select tenders that compress margins. The report quantifies these risks under multiple scenarios and recommends early detection triggers to pivot strategy before value erodes.

In keeping with PW Consulting’s “trailer” approach, this release highlights the strategic conclusions and recommended actions without reproducing the proprietary segment tables and regional revenue splits that form the foundation of our analysis. The full report contains:

Granular regional and application segmentation with time‑series data (historical and forecast) to support market entry and pricing plans.

Detailed competitor benchmarking and facility‑level capability assessment.

Price‑to‑cost sensitivity models and supplier scorecards you can apply to contract negotiations.

Appendices with standards compliance matrices and an up‑to‑date vendor directory to streamline procurement RFPs.

For executives making capital or procurement decisions in 2026, the choice is not whether the market grows but how to capture durable value as it does. Companies that combine disciplined cost management, standards‑driven product design, and selective geographic footprint strategies will outpace peers in margin and market share expansion. PW Consulting’s full market study equips leadership teams with the calibrated intelligence needed to execute those moves with conviction.

For organizations seeking the full dataset, models, and executable templates referenced in this preview, PW Consulting provides tiered access to the report and bespoke advisory services to translate findings into a 90‑day action plan. Contact PW Consulting for access to the full Worldwide Cast Iron Manhole Covers Market report, including the complete segmentation and company appendices.

For detailed analysis of this topic, please visit the official page:Worldwide Cast Iron Manhole Covers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com