Worldwide Prescription Diet Pet Food Market — Strategic Outlook for 2026 Decision-Makers

Executive summary

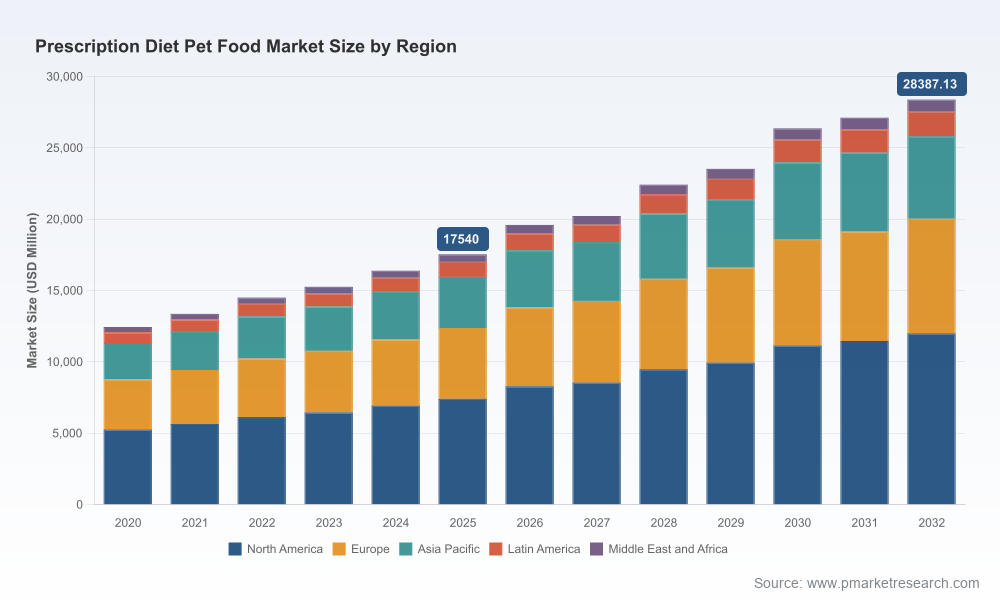

As veterinary nutrition moves from niche therapy into an established commercial category, the worldwide prescription diet pet food market is entering a decisive phase for corporate strategy. Our latest PW Consulting report—anchored on a 2025 base and spanning a historical window (2020–2025) with a forward-looking 2026–2032 forecast—demonstrates a sustained, above-market expansion path underpinned by clinical adoption, channel maturation, and product innovation. The market reached a significant milestone in 2025 (reported in USD, revenue unit: Million) and is projected to expand at a compound annual growth rate (CAGR) of 7.12% through the 2026–2032 forecast period, resulting in notable scale by 2032.

Worldwide Prescription Diet Pet Food Market

For executive teams preparing 2026 budgets and three-year strategic plans, the implications are clear: the category is large enough to justify dedicated R&D, commercial investment, and targeted M&A, yet concentrated enough that competitive positioning and channel influence materially shape outcomes. Our analysis blends top-down market dynamics with practitioner-ready tools so that leadership teams can convert market momentum into profitable, defensible growth.

Worldwide Prescription Diet Pet Food Market

Why this report matters for 2026 decisions

- Actionable market sizing and pacing: We provide a robust macro growth trajectory (2020–2025 historic base with a 2026–2032 forecast at a 7.12% CAGR) to inform capacity planning, capital allocation, and portfolio prioritization.

- Concentration-aware strategy: The category exhibits a high degree of concentration among leading veterinary nutrition brands, informing competitive and partnership strategies in 2026 and beyond.

- Regulatory and input-cost risk baked into scenarios: The report models regulatory constraints and raw-material volatility—essential inputs when building resilient procurement and pricing strategies for 2026.

- Commercial playbooks for vet channels: Practical guidance on orchestrating veterinarian relationships, optimizing product listings, and leveraging clinical data to accelerate uptake in 2026 rollouts.

What’s inside the report — practical content for implementation

- Market architecture and growth drivers: A synthesis of demand-side forces (clinical prevalence, pet-owner willingness to pay, and channel dynamics) and supply-side enablers (manufacturing scale, therapeutic R&D).

- Five-path strategic framework: Clear decision trees for pursuing premium therapeutic innovation, portfolio rationalization, channel expansion, cost leadership, or bolt-on M&A.

- Regulatory & compliance checklist: A region-aware mapping of veterinarian authorization requirements, labeling standards, and manufacturing controls to include in 2026 launch gate reviews.

- Scenario toolkits: Scenario-based P&L and NPV templates that incorporate a baseline CAGR and alternative downside/upside ingredient price and regulatory scenarios.

- Commercial playbooks: Tactical approaches to trade terms, veterinary education programs, and digital enablement to improve prescription conversion and refill adherence.

- Risk register and mitigation plans: Practical controls for supply-chain disruption, reputational risk from therapeutic claims, and cross-contact allergen compliance.

Competitive landscape — what the leaders are doing and what it means for challengers

The prescription diet segment is dominated by a small group of global veterinary nutrition specialists and integrated petcare conglomerates. Our competitive assessment focuses on four core players—each with distinct strengths that inform different competitive responses.

Worldwide Prescription Diet Pet Food Market

- Hill’s Pet Nutrition (Topeka, Kansas, USA): Hill’s Prescription Diet portfolio remains differentiated by breadth of therapeutic formulas and deep clinical positioning with veterinary channels. Recent product introductions—such as new kidney-support wet formats—signal continued investment in clinically-validated SKUs that support market share defense among practitioners.

- Royal Canin (Aimargues, France): Royal Canin’s Veterinary Diet range emphasizes formulation depth and global veterinary reach. Tactical moves such as expanding package-size options reflect an optimization approach to improving affordability and compliance—an area aspirants can replicate via targeted pack innovations.

- Nestlé Purina PetCare (St. Louis, Missouri, USA): Purina leverages brand equity and global distribution muscle to accelerate adoption of its Pro Plan Veterinary Diets. Visibility at major trade events and refreshed formula portfolios suggest an intent to blend clinical credibility with consumer-oriented messaging—creating headwinds for pure-play specialists that lack strong consumer-facing assets.

- Virbac (Carros, France): Virbac’s Veterinary HPM line targets specific therapeutic niches such as obesity and dermatology, maintaining a prescription-only, veterinarian-centric go-to-market model. Its narrower focus offers a playbook for mid-sized players to build defensible niches without attempting full-spectrum competition.

Together, these firms create a high barrier to entry on the basis of veterinarian relationships, clinical data libraries, and scale manufacturing. Our market concentration analysis corroborates that a handful of players command the majority of volume and influence, which has direct implications for partnership and channel strategies in 2026.

Regulatory and input dynamics shaping 2026 strategies

Three non-market forces are particularly influential for next-year planning:

- Regulatory gatekeeping: Prescription diets require veterinary authorization in several major markets per veterinary and regulatory guidance. Compliance with regional registration and additive limits—especially for cross-border trade into the EU—must be a go/no-go checklist item for 2026 market entries.

- Manufacturing controls and labeling standards: National standards for nutrient adequacy statements and strict preventive controls (including allergen cross-contact prevention) increase the cost and complexity of new product introductions, favoring firms with GMP-scale facilities or contract manufacturers capable of certified production lines.

- Raw-material volatility: Recent commodity disruptions—exemplified by upward pressure on key ingredients—underscore the need for procurement hedges, alternative sourcing strategies, and margin-protection levers in pricing models for 2026.

Strategic plays for 2026 — recommended actions by priority

- Prioritize therapeutic breadth where you have clinical credibility: Invest in one or two high-evidence indications and build dossier-level clinical support; use these as beachheads for practitioner trust and formulary placement.

- Channel orchestration over channel expansion: Deepen veterinarian relationships with education, patient-support tools, and refill-subscription models rather than broadening distribution prematurely. Prescription conversion and adherence lift outcomes and compounding lifetime value.

- De-risk supply with multi-sourcing and formula elasticity: Introduce formulation variants that allow switching between homologous raw materials without sacrificing label claims. Lock in strategic supplier contracts and build contingency inventory buffers for critical ingredients.

- Explore bolt-on M&A to fill capability gaps: Given category concentration, small- to mid-cap acquisitions focused on niche therapeutic IP, specialty manufacturing, or regional veterinarian networks can accelerate scale more predictably than organic growth alone.

- Embed regulatory and labeling readiness into product launch timelines: Treat regulatory registration and FSMA/AAFCO compliance as path-dependent gating items in product launch roadmaps to avoid costly market delays.

How to use this report in your 2026 planning cycle

Use the PW Consulting report as both a strategic compass and an execution manual. At a minimum, leadership teams should extract four outputs for 2026 planning: a) a prioritized list of therapeutic investments with cost-to-clinical-validation estimates; b) a channel activation plan for veterinarians; c) a supply risk dashboard with supplier concentration and price-sensitivity thresholds; and d) scenario-modeled financials that incorporate the baseline CAGR and upside/downside ingredient scenarios.

Our report intentionally provides the full set of segmented tables, regional breakdowns, and SKU-level market intelligence behind a gated dataset to allow you to calibrate these outputs to your P&L and regional priorities. The executive synopsis here highlights the decision-useful takeaways while reserving detailed cell-level data for subscribing clients—consistent with our “trailer” approach to preserve the strategic value of proprietary segmentation.

Next steps

For teams finalizing 2026 AOPs, the immediate priorities are clear: lock procurement protections for critical ingredients, finalize at least one clinical dossier for a core therapeutic indication, and execute a veterinarian engagement pilot that can be scaled. PW Consulting is available to run bespoke scenario workshops, validate M&A targets against clinic-level economics, and deploy go-to-market blueprints that translate the macro growth trajectory into executable plans.

To access the complete dataset, regional segmentations, and practitioner-level benchmarks that underpin these conclusions, please visit the report landing page or contact your PW Consulting account lead. The full report delivers the granular intelligence and modeling templates required to operationalize the strategies outlined here and to ensure your 2026 decisions are defensible, data-driven, and forward-looking.

For detailed analysis of this topic, please visit the official page:Worldwide Prescription Diet Pet Food Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com