Worldwide Ultrasonic Scissor Market — Strategic Insights for 2026 Decisions

As healthcare providers accelerate the shift toward minimally invasive and robot-assisted procedures, ultrasonic scissors have moved from niche adjuncts to core components of surgical energy toolkits. PW Consulting’s latest Worldwide Ultrasonic Scissor Market report (base year 2025) synthesizes seven years of historic performance, competitive intelligence and forward-looking scenarios to equip executives making high‑stakes product, regulatory and commercial decisions in 2026. This executive briefing highlights the report’s strategic value while preserving proprietary segmentation detail to encourage direct engagement with the full study.

Worldwide Ultrasonic Scissor Market

Market at a glance: scale, momentum and outlook

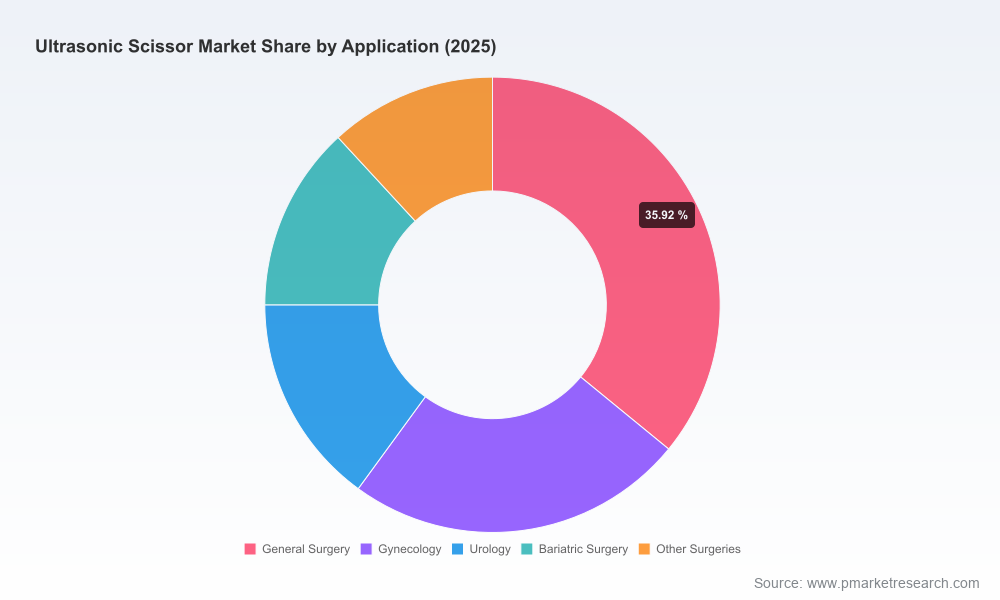

The ultrasonic scissor market demonstrated resilient growth through 2020–2025, reaching USD 1,452.5 Million in 2025. Our modelling projects continued expansion at a compound annual growth rate (CAGR) of 6.5% across the 2026–2032 forecast window, culminating in a market size above USD 2.2 Billion by 2032. That pace reflects a combination of procedure mix evolution, device innovation, and expanding adoption in emerging markets — dynamics that materially affect competitive positioning and investment timing.

Worldwide Ultrasonic Scissor Market

Why this matters for 2026 strategic planning

- Timing of adoption inflection points: The market’s steady CAGR masks inflection zones driven by product approvals, robotic platform integrations and reimbursement shifts. Executives who align product launches and evidence generation with those windows can capture disproportionate share.

- Concentration and competitive pressure: The market shows a high concentration among leading incumbents, underscoring both the advantages of scale and the risks to challengers that lack distribution or clinical partnerships. Consolidation and platform bundling are likely to intensify through 2026–2028.

- Regulatory clarity as an enabler: Recent 510(k) clearances and the codification of ultrasonic instruments under established FDA product codes de‑risk entry for companies with robust clinical programs, while also raising the bar on post‑market surveillance and labeling claims.

Key market dynamics shaping 2026 choices

- Clinical utility and workflow integration: Ultrasonic scissors deliver a combination of cutting and coagulation that shortens operative time and reduces instrument exchanges. The value narrative for hospital procurement teams increasingly emphasizes total cost of procedure rather than unit price alone.

- Robotics and platform play: Robotic surgical systems are incorporating advanced ultrasonic energy tools. The December 2024 launch of an ultrasonic dissector for a major robotic platform signals a new front on which device makers will compete: integration, sterility economics and instrumentation lifecycle management.

- Price and sourcing pressure: A bifurcated market is emerging — premium, platform‑integrated devices from established medtech firms versus cost‑competitive disposable or bundled offerings from regional manufacturers. Strategic sourcing programs at health systems will test supplier margin models in 2026.

- Regulatory and reimbursement evolution: Clearance pathways are established, but incremental claims (e.g., vessel sealing to larger diameters, reduced thermal spread) require targeted clinical evidence. Early regulatory wins translate into faster market access, particularly in cost‑sensitive channels.

- Service and sustainability considerations: Reusable vs. single‑use economics, reprocessing programs and environmentally driven procurement policies are shifting purchasing criteria — presenting opportunities for differentiated service bundles and circular‑economy positioning.

Competition: what incumbents and challengers are doing

Competitive dynamics blend global scale players with fast‑moving regional suppliers. Leading medtech companies offer mature ultrasonic portfolios integrated into broad surgical energy platforms, leveraging global distribution and clinical networks. At the same time, a cohort of agile device manufacturers — particularly from Asia — has secured certifications and clearances, enabling targeted penetration in price‑sensitive segments and specific procedure types.

Worldwide Ultrasonic Scissor Market

- Johnson & Johnson (Ethicon): Established incumbent with comprehensive HARMONIC product lines that emphasize precision, vessel sealing capability and single‑patient use convenience. Strengths include clinical adoption, surgical familiarity and platform bundling across minimally invasive procedures. (HQ: New Brunswick, USA — https://www.jnjmedtech.com)

- Medtronic: Focused on cordless and ergonomic ultrasonic dissectors aimed at simplifying OR workflows and enabling hybrid procedure adoption. Strong global reach and integration with hospital contracts are competitive advantages. (HQ: Dublin, Ireland — https://www.medtronic.com)

- Olympus Corporation: Leverages endoscopic and laparoscopic leadership to position ultrasonic devices for endoscopic energy requirements, with particular strength in scope‑based workflows. (HQ: Tokyo, Japan — https://www.olympus-global.com)

- Stryker Corporation and B. Braun: Both participate in the ultrasonic ecosystem through productization, reprocessing and channel partnerships; their involvement underscores the value of aftermarket and service models in preserving share. (Stryker HQ: Kalamazoo, USA — https://www.stryker.com; B. Braun HQ: Melsungen, Germany — https://www.bbraun.com)

- Regional Innovators (China): A group of manufacturers have ramped clinical evidence and regulatory clearances, offering lower‑cost alternatives and rapid customization. Several have obtained CE and FDA recognitions and are pushing into adjacent device platforms and bundled energy solutions.

Market concentration metrics in our study indicate that the top three and top five suppliers account for a substantial majority of revenue, reinforcing the scale advantage incumbents enjoy while highlighting the runway for consolidation and niche disruption.

Practical content in the PW Consulting report — what executives will find

The full report is built for decision‑makers needing executable insights, not academic overviews. Core deliverables include:

- TAM and serviceable market models with scenario analyses (optimistic, base, conservative) and sensitivity to key variables such as procedure mix, hospital buying cycles and robotic adoption rates.

- Seven‑year historic performance (2020–2025) and detailed forecast (2026–2032) with transparent modelling assumptions and Monte Carlo stress tests for downside risk planning.

- Competitive benchmarking: product feature matrices, go‑to‑market archetypes, pricing ladders, and SWOT profiles for incumbent and challenger firms.

- Regulatory pathway mapping and checklist for 510(k) submissions, including typical evidence packages and post‑market surveillance expectations by jurisdiction.

- Clinical evidence compendium that consolidates peer‑reviewed outcomes, procedural efficiency studies, and real‑world hospital case reports relevant to ultrasonic scissors.

- Commercial playbooks: tender and GPO engagement strategies, hospital value‑case calculators, and segmentation of buying personas (OR directors, procurement leads, clinical champions).

- M&A and partnership advisory: target screening criteria, valuation templates adapted to device lifecycle economics, and integration checklists for rapid post‑deal value capture.

- Operational readiness tools: manufacturing scale‑up roadmaps, cost‑of‑goods sensitivity analysis, supplier risk matrices and guidance on reprocessing vs disposable decisions.

Five strategic moves to prioritize in 2026

- Accelerate evidence generation tied to procurement levers — targeted randomized or registry data that quantify OR time savings and disposables reduction will unlock favorable contract terms.

- Negotiate platform partnerships with robotic system providers or endoscope manufacturers to secure integration pathways and preferred supplier status ahead of competitors.

- Revisit pricing models to reflect total cost of ownership; consider outcome‑based pilots or bundled pricing to demonstrate superior economics to health systems.

- Strengthen regulatory and quality infrastructures to shorten time‑to‑clearance for incremental claims; early engagement with regulators reduces launch risk and credibility barriers.

- Use M&A tactically to acquire narrow technical capabilities (e.g., improved sealing tech) or regional distribution where organic entry would be slower and costlier.

Case signals and recent milestones

- Robotic integration: A late‑2024 launch of an ultrasonic dissector for a surgical robot underscores the near‑term importance of platform compatibility in procurement decisions.

- Regulatory momentum: Recent 510(k) clearance for a disposable ultrasonic shears system highlights that credible, lower‑cost entrants can achieve U.S. market access when they align clinical evidence and quality systems.

- Product innovation: New offerings that extend vessel sealing capability and improve ergonomics are being introduced — these incremental improvements materially influence surgeon preference and hospital adoption rates.

Conclusion — positioning for outsized value in 2026

By 2026, companies that combine credible clinical evidence, platform partnerships and commercially savvy pricing will capture the lion’s share of the market growth opened up by procedural shifts and robotic adoption. PW Consulting’s report provides the empirical backbone and tactical roadmaps to prioritize investments, manage regulatory timelines and structure commercial rollouts. The research is intentionally detailed in method and prescriptive in execution — while selective in publishing proprietary segment breakouts — so that subscribers get exclusive, actionable intelligence.

Next steps

For boards, corporate strategy teams and business unit leaders planning 2026 initiatives, PW Consulting recommends commissioning the full report and accompanying advisory workshop. The full deliverable contains the granular segment forecasts, pricing matrices, and supplier‑level intelligence required to operationalize the five strategic moves above. Contact PW Consulting to schedule a briefing and obtain the proprietary datasets that support investment, M&A and launch decisions in the worldwide ultrasonic scissor market.

For detailed analysis of this topic, please visit the official page:Worldwide Ultrasonic Scissor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com