PW Consulting Strategic Preview: Worldwide IT Infrastructure Outsourcing Service Market — Essential Intelligence for 2026 Decision-Makers

Executive summary

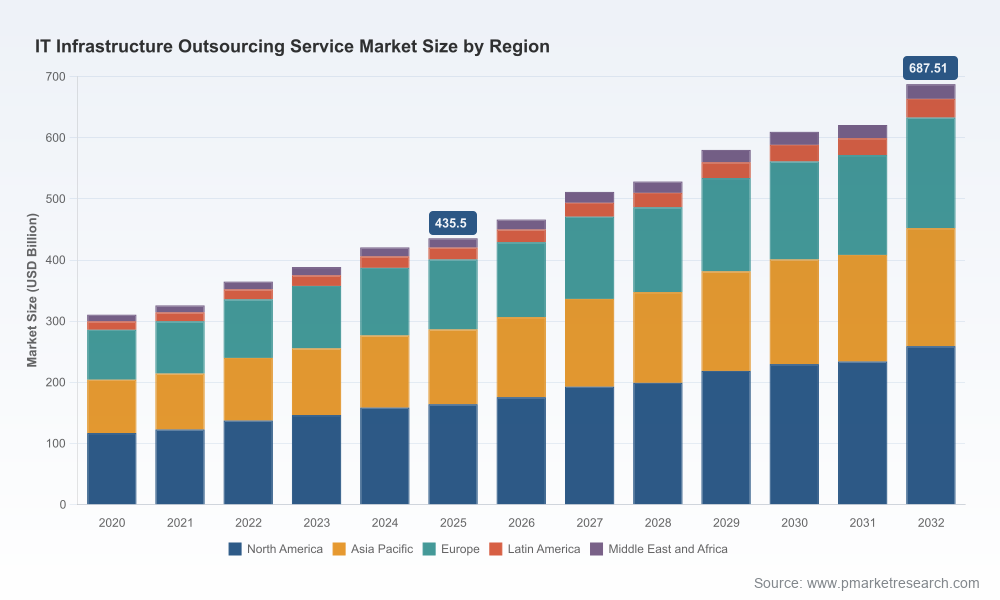

As enterprises finalize 2026 sourcing strategies, the IT infrastructure outsourcing (IITO) market presents both scale and structural complexity that demand disciplined strategic choices. PW Consulting’s latest market model—anchored to a 2025 base year—estimates the global IITO market at USD 435.5 billion in 2025 and projects growth at a compound annual growth rate (CAGR) of 6.74% through our 2026–2032 forecast horizon. By 2026 the market is expected to exceed USD 466 billion and to approach roughly USD 688 billion by 2032. This expansion reflects a secular shift: cloud and security become baseline expectations; AI and automation reshape delivery economics; and regulatory, labor‑cost and data‑residency pressures reconfigure sourcing footprints.

Worldwide IT Infrastructure Outsourcing Service Market

Why this preview matters for 2026 strategic choices

Boardrooms and CIO offices face a compressed window in 2026 to convert market change into competitive advantage. Key dynamics to factor into sourcing strategy:

Worldwide IT Infrastructure Outsourcing Service Market

- Technology acceleration: Managed cloud, integrated security services and AI‑enabled operations are no longer experimental add‑ons — they are core components buyers expect in any meaningful outsourcing engagement.

- Cost and delivery model evolution: Rising labor costs in traditional offshore hubs are increasing the attractiveness of nearshoring, automation and outcome‑based commercial models.

- Regulatory and compliance intensity: New rules such as the U.S. DOJ Bulk Data Rule (effective April 2025), combined with persistent GDPR, HIPAA and sector standards, mean vendors must demonstrate continuous controls, vendor risk assessments and formal certifications (SOC 2, ISO 27001) — and buyers must bake those requirements into contract governance.

- Market structure: The market’s scale coexists with a moderate level of fragmentation; a relatively small share of the market is held by the largest incumbents, making vendor selection both an opportunity for specialization and a sourcing risk.

What the full report delivers (practical, action‑oriented content)

PW Consulting’s full Worldwide IT Infrastructure Outsourcing Service Market report is designed for immediate operational use by procurement, IT strategy and enterprise risk teams. The deliverables include:

Worldwide IT Infrastructure Outsourcing Service Market

- Robust market sizing and multi‑year forecasts (2020–2032) with scenario variants and sensitivity analysis to model inflation, labor shifts and contraction/expansion scenarios.

- Decision frameworks for sourcing (insource vs. outsource vs. hybrid), including an actionable supplier segmentation methodology and playbooks for small, mid and large engagements.

- TCO and ROI templates tailored for infrastructure outsourcing, integrating migration costs, continuous security, regulatory compliance and automation savings.

- Negotiation‑ready RFP/RFI templates, standardized SLA language, playbooks for data residency clauses and prescriptive governance models (including continuous vendor risk assessment schedules and compliance checkpoints).

- Vendor due‑diligence checklists and a comparative capability matrix that covers cloud operations, managed security, hybrid infrastructure and AI‑enabled delivery (note: detailed regional and service‑type revenue splits are contained in the full report and are intentionally omitted from this public preview).

- Implementation accelerators — migration roadmaps, runbook examples for AIops integration, and a security‑first transition protocol to avoid service disruptions during vendor changeovers.

Competitive landscape — what to watch and how vendors are positioning

The vendor field spans global consultancies, hyperscale integrators and specialist infrastructure players. Each cohort is adapting to three imperatives: integrate AI and automation into delivery; embed security and compliance as a managed offering; and reshape delivery footprints in response to labor cost pressures.

- Global consultancies and systems integrators (e.g., Accenture, IBM, Deloitte, Capgemini) — These firms emphasize end‑to‑end transformation, combining cloud migration, hybrid operations and cybersecurity advisory with large account management. Recent M&A and capability builds underscore a move to bundle agentic AI capabilities with infrastructure services.

- Indian majors (e.g., TCS, Infosys, Wipro, HCLTech, Tech Mahindra) — These providers continue to offer scale and cost arbitrage while accelerating productization of managed services and AI ops. Strategic partnerships with AI platform vendors and targeted acquisitions are shifting the value proposition from pure labor arbitrage to outcome‑driven managed platforms.

- Infrastructure specialists and providers (e.g., Kyndryl, DXC Technology, NTT DATA, Fujitsu, Atos) — These firms focus deeply on data center outsourcing, hybrid cloud operations and verticalized compliance practices for regulated sectors. Their advantage is operational depth and long‑term managed services relationships.

Recent moves underline these trends. In mid‑2025 a major European integrator completed a sizable acquisition to aggressively embed agentic AI across business‑process and infrastructure services; an Indian engineering leader announced a strategic partnership with a leading AI platform to strengthen AI‑powered delivery; and a regional specialist made targeted acquisitions to expand cybersecurity and industry‑specific capabilities. Collectively these actions signal an industry pivot from transactional outsourcing to outcomes‑based, AI‑enabled, and compliance‑infused managed services.

Strategic implications for enterprise decision‑makers in 2026

Enterprises must adopt a risk‑calibrated, opportunity‑focused approach to IITO that aligns with both near‑term operational needs and medium‑term transformation goals. PW Consulting recommends a prioritized action set:

- Run a compliance‑first estate segmentation: classify workloads by data sensitivity, regulatory exposure and modernization urgency. Use this segmentation to determine whether to retain, nearshore, or outsource.

- Lock in security and compliance as contract preconditions: require continuous vendor risk assessments, SOC 2/ISO 27001 evidence, explicit data residency commitments and AI governance clauses for any AI‑enabled service.

- Design commercial models that reward automation and outcomes: shift to shared‑savings or indexed benchmarking for AI/automation uplift rather than purely headcount‑based pricing.

- Accelerate pilot programs for AIops and managed security: prioritize low‑risk but high‑learning pilots to validate savings and operational readiness before broad rollouts.

- Reconfigure delivery footprint strategically: evaluate nearshoring and hybrid delivery to balance talent cost, continuity and regulatory constraints, and plan transition buffers to avoid capacity gaps.

- Strengthen governance and vendor management: implement continuous monitoring, quarterly risk reviews, and an escalation matrix tied to compliance milestones and incident response SLAs.

- Build scenario plans for regulatory shocks: incorporate the operational impact of rules like the DOJ Bulk Data Rule and potential jurisdictional restrictions into contingency plans and contracts.

How PW Consulting supports 2026 execution

PW Consulting combines market intelligence with execution capabilities. For organizations preparing for 2026 we provide:

- Custom benchmarking against peers and vendor capability gap analysis.

- Tailored RFP design and vendor selection advisory that embeds compliance, AI governance and automation KPIs.

- Contract negotiation support focused on risk allocation, performance incentives and data‑residency protections.

- Transformation roadmaps and migration playbooks to transition workloads with minimal operational disruption and measurable cost/reliability targets.

- Implementation oversight, including security validation, compliance audits and post‑transition vendor performance management.

Final note — why access the full report

This preview outlines the strategic contours every executive should weigh in 2026. PW Consulting’s full report provides the granular datasets, regional and service‑type splits, vendor scoring matrices and templates you need to execute with confidence. If your 2026 plan touches infrastructure outsourcing — whether to reduce cost, accelerate cloud adoption, harden security or deploy AI in operations — the full report delivers the actionable detail to move from intent to outcomes.

To obtain the full dataset, detailed segmentation and executable tools, access the report page on PW Consulting’s website and download the comprehensive Worldwide IT Infrastructure Outsourcing Service Market study.

For detailed analysis of this topic, please visit the official page:Worldwide IT Infrastructure Outsourcing Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com