Worldwide Ceramic Wafer Boat Market: Strategic Intelligence to Guide 2026 Decisions

PW Consulting’s latest market study on the Worldwide Ceramic Wafer Boat market is designed as a decision-grade intelligence product for executives planning capital allocation, supply chain adjustments, or technology bets entering 2026. Our analysis synthesizes a robust historical series (2020–2025), a clearly defined base year of 2025, and a forward-looking forecast horizon (2026–2032). The headline: the market is expanding at a sustained pace, underpinned by strong demand for high-temperature, low-contamination wafer handling solutions across modern semiconductor fabrication processes.

Worldwide Ceramic Wafer Boat Market

Market Trajectory and Key Macro Metrics

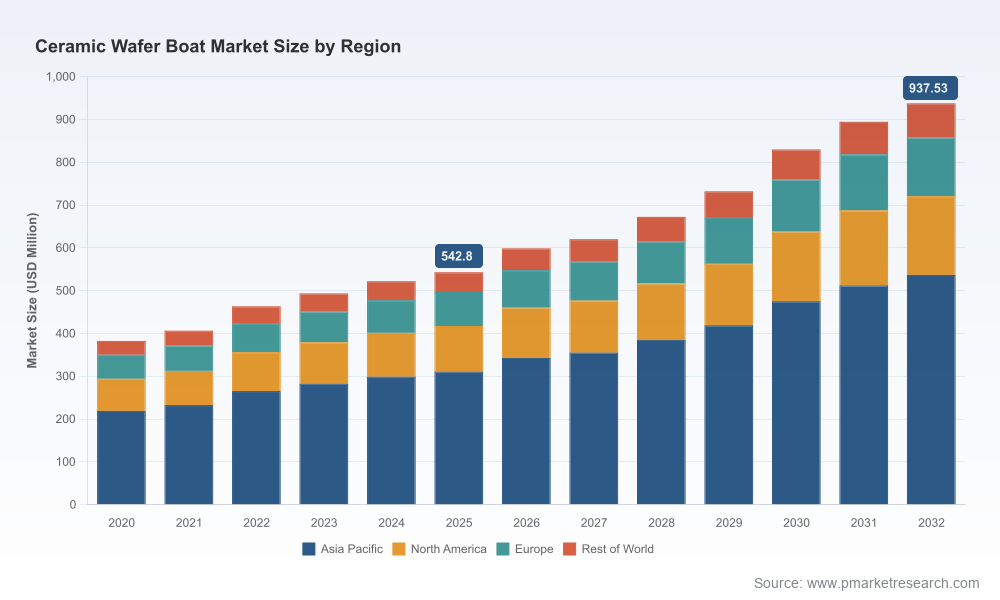

Understanding the macro trajectory is a prerequisite for any strategic move. Our report documents a clear, multi-year expansion in global market value. The total market progressed from USD 382.4 Million in 2020 to USD 542.8 Million in the 2025 base year, with a projected increase to USD 598.5 Million in 2026 and a long-term projection reaching approximately USD 937.5 Million by 2032. These figures translate into a compound annual growth rate (CAGR) of 8.12% across the forecast window (2026–2032), signaling attractive growth dynamics for suppliers and integrators who can align product portfolios with next-generation process requirements.

Worldwide Ceramic Wafer Boat Market

Two structural facts are particularly relevant for executives: (1) demand is driven not merely by wafer volumes, but by technology nodes and process chemistries that place increasing premium on thermal stability and low particulate generation; and (2) market concentration is meaningful — the top three and five players together hold near-majority shares, creating both competitive barriers and acquisition opportunities for market entrants and tier-two suppliers. PW Consulting’s detailed concentration analysis provides numeric thresholds and competitive scenarios that should be read in conjunction with corporate strategy sessions.

Worldwide Ceramic Wafer Boat Market

Why This Matters for 2026 Planning

- CapEx alignment for fabs: Procurement cycles for ceramic wafer boats are synchronous with tool qualification and process ramp plans. Misaligned lead times or incorrect material selection can materially delay node migration.

- Supplier selection and risk: Given the modest-to-moderate market concentration and specialized manufacturing capabilities required, supplier continuity and dual-sourcing strategies are actionable imperatives.

- Materials and technology bets: The differentiation between advanced silicon carbide (SiC) solutions and legacy quartz or alumina-based boats is no longer academic — it affects process windows, contamination profiles, and total cost of ownership.

Key Market Dynamics Shaping Strategy

Our fieldwork and primary interviews reveal four convergent dynamics that will determine winners and losers through 2026 and beyond:

- Materials as a technology lever: Silicon carbide continues to be recognized as the core component for high-performance wafer boats, offering thermal stability well above traditional quartz and reducing contamination risk in harsh oxidation and diffusion environments. At the same time, high-purity quartz and engineered alumina remain relevant in less demanding thermal processes where cost and availability are decisive.

- Regulatory overlay and export control risk: Evolving export control regimes — including refinements to rules covering foreign-produced items tied to semiconductor manufacturing — introduce non-trivial supply chain compliance burdens. This affects sourcing decisions, onshoring strategies, and contingency planning for both OEMs and materials suppliers.

- Regional capacity growth: Fabrication expansions in several geographies are driving incremental demand for ceramic wafer boats. Procurement and qualification calendars are therefore concentrated in the near term; companies that can shorten qualification cycles will capture a disproportionate share of next-wave orders.

- Product innovation and differentiation: Coating technologies (e.g., CVD SiC coatings), recrystallized SiC material forms, and engineering approaches to reduce particle generation are proliferating. Product roadmaps that combine material science advancements with tighter QA/CIM integration will command pricing and loyalty.

Competitive Landscape: Profiles and Strategic Postures

Our competitive assessment covers established global firms and fast-scaling regional players. The market incumbents combine deep ceramics expertise, process-level know-how, and long-standing relationships with tool OEMs and wafer fabs. PW Consulting highlights several archetypal competitors and what they imply for market dynamics.

- Kyocera Corporation (Kyoto, Japan): A strengths-based player with an emphasis on high-purity sapphire and advanced ceramics. Kyocera’s engineering focus on plasma and heat resistance and low particle generation keeps it competitive in premium tool segments.

- CoorsTek, Inc. (Golden, Colorado, USA): Brings global scale in engineered ceramics and a reputation for thermal and chemical resilience, making it a go-to for high-temperature process segments and for customers placing a premium on material pedigree.

- Ferrotec Corporation (Santa Clara, USA; operations in Japan and Taiwan): Differentiates through a breadth of materials — including quartz and SiC — and the systems-level integration experience important for tool-level OEM qualification.

- China-based specialist manufacturers (e.g., Semicorex, Semicera, 3X Ceramic Parts, VeTek, Shenyang Starlight, Gorgeous Ceramic, Hunan DeZhi): These firms are scaling rapidly, offering close-to-market custom solutions and competitive pricing. Several have developed coated variants and custom geometries tailored to regional fab requirements, and they are increasingly central to supply resilience discussions.

PW Consulting’s report examines each company’s vertical strengths, capacity footprints, IP posture, recent product introductions, and route-to-market tactics. We also overlay M&A and partnership scenarios that could materially alter market structure during the forecast window.

Recent Market Signals (Selected)

- Aug 2025 — Engineering Ceramic Co., Ltd. launched recrystallized SiC wafer boats with CVD-SiC coating options in multiple material variants, signaling continued product innovation and customization for advanced processes.

- Mar 2025 — Ningbo VET Energy updated its product catalog emphasizing premium SiC solutions and manufacturing capabilities, reflecting the ongoing upgrade cycle among equipment and fab customers.

- Jan 2026 — Shenyang Starlight demonstrated its SiC portfolio at a major advanced ceramics exhibition, underscoring regional technology maturation and commercial outreach.

What Our Report Delivers — Practical, Actionable, Proprietary

PW Consulting positions this study as a strategic toolkit for 2026 decision-makers. The report blends rigorous quantitative modeling with qualitative intelligence and is organized to support immediate operational and strategic actions:

- Market sizing and trajectory with transparent methodology: historical series (2020–2025), base-year detail (2025), and scenario-based forecasts (2026–2032) reflecting alternative demand and regulatory pathways.

- Competitive heat maps and supplier scorecards: capability assessments across materials, manufacturing scale, coating technologies, geographic footprint, and compliance readiness.

- Technology readiness matrix: side-by-side comparisons of SiC forms (e.g., recrystallized, SiSiC), coated vs. uncoated solutions, and process compatibility (e.g., high-temperature diffusion vs. lower-temperature anneal).

- Procurement playbook: risk-adjusted supplier selection frameworks, qualification time reduction tactics, contract clauses for export-control compliance, and inventory buffers calibrated to lead-time volatility.

- Investment and M&A scenarios: valuations, synergies, and market-entry strategies informed by CR metrics and regional capacity trends.

- Case studies and supplier negotiation scripts drawn from PW Consulting’s primary engagements with fabs, tool OEMs, and ceramic manufacturers.

Note: To preserve commercial confidentiality and to encourage direct engagement, the report intentionally refrains from publishing granular regional or application-specific revenue slices in open summaries. The full report contains the complete segmentation tables and downloadable data sets for licensed clients.

Strategic Imperatives — Actions to Take Before Q2 2026

- Fabs and OEMs: Re-evaluate material specs for slated process ramps, prioritizing qualification of SiC-based options where thermal and contamination constraints are critical. Initiate dual-sourcing for any high-readiness tool lines and lock in supply agreements that include compliance clauses for export-control regimes.

- Ceramic manufacturers: Invest selectively in coating and recrystallized SiC capabilities, and pursue targeted certifications with leading tool OEMs. Consider JV or toll-manufacturing models to reduce customer switching costs.

- Procurement teams: Implement a risk-weighted inventory strategy that balances just-in-time efficiency against the potential for regulatory-induced supply disruptions. Prioritize suppliers with proven traceability and compliance processes.

- Investors and private equity: Use the market concentration and growth profile to screen for roll-up targets that can centralize coating R&D, scale production, and internationalize distribution to capture near-term demand.

Next Steps

PW Consulting’s Worldwide Ceramic Wafer Boat Market report is built to be an operational asset for strategy teams preparing for 2026. Our public-facing summary intentionally showcases the analytical depth and practical frameworks while reserving full segmentation tables, supplier-level revenue breakdowns, and downloadable datasets for licensed report access. Clients who require scenario workshops, supplier diligence packages, or bespoke market decomposition for procurement RFPs can commission executive briefings and interactive model access.

For firms that need to accelerate decision timelines ahead of 2026 procurement cycles, this study provides the context, contingencies, and playbooks necessary to turn market growth into durable advantage.

For detailed analysis of this topic, please visit the official page:Worldwide Ceramic Wafer Boat Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com