Worldwide Disposable Surgical Electrodes Market — Strategic Briefing for 2026 Decision‑Makers

PW Consulting’s latest market study on Worldwide Disposable Surgical Electrodes delivers a concise, action-oriented briefing designed specifically for executive teams, corporate strategy groups, commercial leaders, and M&A professionals preparing 2026 roadmaps. This briefing highlights the report’s most consequential implications—market scale, growth trajectory, regulatory inflection points, competitive dynamics, and prioritized go‑to‑market moves—while preserving detailed sub‑segment datasets for subscribers to the full report.

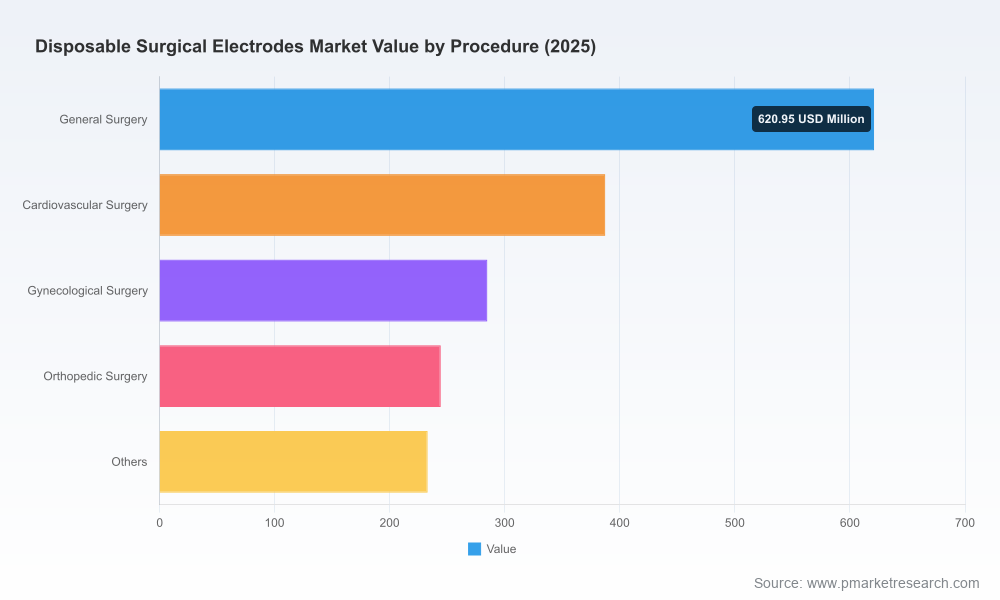

Worldwide Disposable Surgical Electrodes Market

Market snapshot: scale, growth and concentration

The disposable surgical electrodes market has moved from a sizable, stable industry to a clearly expanding opportunity set. Our analysis shows the global market increasing from approximately USD 1,320.5 Million in 2020 to USD 1,770.45 Million in 2025. Underpinning that expansion, the market is forecast to continue growing at a compound annual growth rate (CAGR) of 6.48% over the 2026–2032 forecast period, reaching roughly USD 2,747.64 Million by 2032.

Worldwide Disposable Surgical Electrodes Market

Concentration metrics indicate a moderately consolidated market: the top three players account for about 42.15% of market revenues, while the top five capture approximately 56.4%. For strategy teams, this presents a dual reality—meaningful competitive moats exist for established incumbents, while distinct niches and specialty product categories remain accessible to agile challengers and regional players.

Worldwide Disposable Surgical Electrodes Market

Why this matters for 2026 planning

- Investment timing: A steady 6.48% CAGR signals a market that rewards disciplined capacity expansion, targeted product investment, and clinical evidence generation rather than speculative scale‑up.

- Portfolio decisions: There is room to shape portfolio mix toward differentiated disposable electrodes (e.g., non‑stick coatings, specialty bipolar instruments, RF plasma platforms) that can command premium pricing and reduce commoditization risk.

- M&A and partnership playbook: Moderate concentration plus strong mid‑market presence makes bolt‑on acquisitions, technology licensing, and OEM partnerships efficient routes to scale and access to new procedure adjacencies.

Regulatory and standards environment: what to build into 2026 roadmaps

Disposable electrosurgical electrodes are governed by well‑established regulatory and safety regimes which should be integral to product and go‑to‑market planning. In the U.S., these devices are typically regulated as Class II devices (product code GEI) under 21 CFR 878.4400 and commonly require 510(k) clearance. Compliance with IEC electrical safety and performance standards (notably IEC 60601‑1, IEC 60601‑1‑2, and IEC 60601‑2‑2) is an industry baseline.

Operationally relevant realities we highlight:

- Regulatory predictability: The 510(k) pathway remains the primary route for market entry—expect consistent timelines but increasing scrutiny on electrical safety and clinical claim substantiation.

- Shelf‑life and sterilization: Many cleared single‑use electrodes use EO gas sterilization and are supported with multi‑year shelf lives; sterilization strategy must be explicit in product design and cost models.

- Standards and verification: Investing early in compliance testing to IEC norms reduces downstream delays and supports premium positioning in hospital procurement.

Technology and supply dynamics—where differentiation is happening

Three persistent technology drivers are defining winners and losers:

- Surface engineering and materials: PTFE and similar non‑stick coatings meaningfully reduce eschar build‑up and improve clinical throughput; suppliers who secure coating expertise and consistent supply chains can convert performance claims into preference at purchase.

- Disposable‑first product design: Electrode geometries optimized for laparoscopic, arthroscopic, ENT, and microsurgical use are expanding procedure coverage—modular single‑use electrodes that integrate with electrosurgical units (ESUs) are particularly attractive for OEM and platform partners.

- Adjacency devices and selective energy modalities: RF plasma, concentric needle disposables for rehabilitation/PMR, and single‑use bipolar platforms are emerging pockets of high growth and differentiated margin.

Competitive landscape: what the incumbent and emerging players indicate

The market comprises a mix of global medtech leaders, specialized surgical consumables firms, and nimble regional manufacturers. Key players profiled in our report include global incumbents such as Medtronic, CONMED, Johnson & Johnson MedTech (Ethicon), ERBE, and Olympus, alongside specialized and regionally strong names like Kirwan Surgical, Progressive Medical Inc., and a range of China‑based manufacturers focused on cost‑competitive disposable electrodes.

Strategic takeaways from company profiles and recent moves:

- Platform leverage matters: Large device companies integrate disposable electrodes into broader surgical energy portfolios and leverage installed base relationships with hospitals to maintain share.

- Niche specialization wins in procedure adjacencies: Companies focused on microsurgical bipolar/disposable non‑stick electrodes, or on ENT and arthroscopic disposables, maintain defensible positions through clinician relationships and tailored product form factors.

- Regulatory clearances accelerate entry: Recent 510(k) approvals for single‑use electrodes and devices (notably several clearances in 2024–2026) demonstrate that regulatory pathways are active and can be used strategically to enter new procedure categories.

Recent notable regulatory and product developments we track include multiple 510(k) clearances across 2024–2026 for single‑use electrode systems and RF/needle disposables, reinforcing that FDA review is proceeding for innovative disposable device formats.

What the full report contains — practical, executable outputs

PW Consulting’s full market study goes beyond directional commentary to deliver hands‑on deliverables your team can use immediately in 2026 planning cycles:

- Actionable market model: A transparent financial model with historicals and scenario forecasts through 2032 (with downloadable inputs) allowing you to stress‑test price, mix, and volume assumptions.

- Commercial playbooks: Channel and tender tactics for hospital procurement teams, differentiated value propositions, and competitive counters optimized for both developed and growth markets.

- Regulatory readiness checklist: Step‑by‑step 510(k) preparation templates, IEC testing roadmaps, and sterilization validation guidance tailored to single‑use electrode formats.

- Manufacturing and sourcing playbook: Cost‑of‑goods modeling, PTFE coating sourcing strategies, contract manufacturing evaluation criteria, and inventory/shelf‑life optimization frameworks.

- M&A and partnership screening tools: Prioritized target archetypes, valuation multipliers specific to disposable surgical consumables, and integration risk checklists focused on regulatory compliance, supply continuity, and clinician adoption.

- Clinical evidence and reimbursement templates: Study design guidance to support product claims and CPT/reimbursement navigation tools for hospital vs. clinic settings.

2026 strategic recommendations — prioritized and time‑bound

Based on our synthesis of market growth, concentration, regulation, and recent product clearances, we recommend the following prioritized actions for companies shaping strategy in 2026:

- Prioritize differentiated consumables: Target R&D and product launches on performance differentiators (e.g., non‑stick coatings, ergonomics for high‑throughput procedures, integrated single‑use bipolar solutions) where reimbursement and clinician preference can support price premiums.

- De‑risk supply and coating tech: Secure PTFE or equivalent coating supply via multi‑year contracts or vertical integration to avoid raw material bottlenecks and protect margin assumptions in the model.

- Accelerate regulatory integration: Build IEC testing and 510(k) documentation into product development lifecycles to reduce time‑to‑market and enable staged geographic rollouts.

- Pursue targeted bolt‑ons: Use M&A to acquire niche product lines and clinician relationships in specialty surgery (ENT, arthroscopy, microsurgery) rather than broad market acquisitions that dilute focus.

- Invest in clinical evidence selectively: Sponsor short, high‑impact clinical or bench studies that directly support differentiated claims and hospital formulary acceptance; prioritize studies with clear procurement ROI signals.

- Refine pricing and channel playbooks by market: Model hospital vs. ambulatory surgery center economics and tailor value‑based selling materials accordingly, including product trials and outcome metrics that procurement teams require.

Limitations and how to get the full intelligence

This briefing intentionally omits detailed sub‑segment revenue splits and granular regional/application percentages—data we reserve for subscribers to the full report. The complete report includes the full segmentation model (by region, product type, and procedure), downloadable datasets, supplier scorecards, and an editable financial model you can adapt to your specific strategic scenarios.

If your 2026 investment, product development, or M&A decisions rely on precise market sizing by product type, region, or procedure, the full report and accompanying data packs are the only source that provide the level of granularity and executable templates covered in this summary.

Next steps

- For commercial teams: Request the commercial playbook extract to align your 2026 tender strategy and pricing experiments with forecasted demand curves.

- For R&D and regulatory leaders: Access the regulatory readiness and IEC testing annex to compress your time‑to‑clearance roadmap.

- For corporate development teams: Obtain the M&A screening pack and financial model to identify high‑priority bolt‑on targets that accelerate specialty market entry.

PW Consulting’s full Worldwide Disposable Surgical Electrodes Market report is structured to meet boardroom needs while equipping front‑line teams with executable tools for 2026. For access to the full dataset, detailed segmentation, and the editable financial model, please visit the report landing page or contact our client services team to arrange a briefing and data license.

For detailed analysis of this topic, please visit the official page:Worldwide Disposable Surgical Electrodes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com