The Rise of Smart HVAC Solutions in Northeast Georgia

Other |

2026-05-14 09:37:04

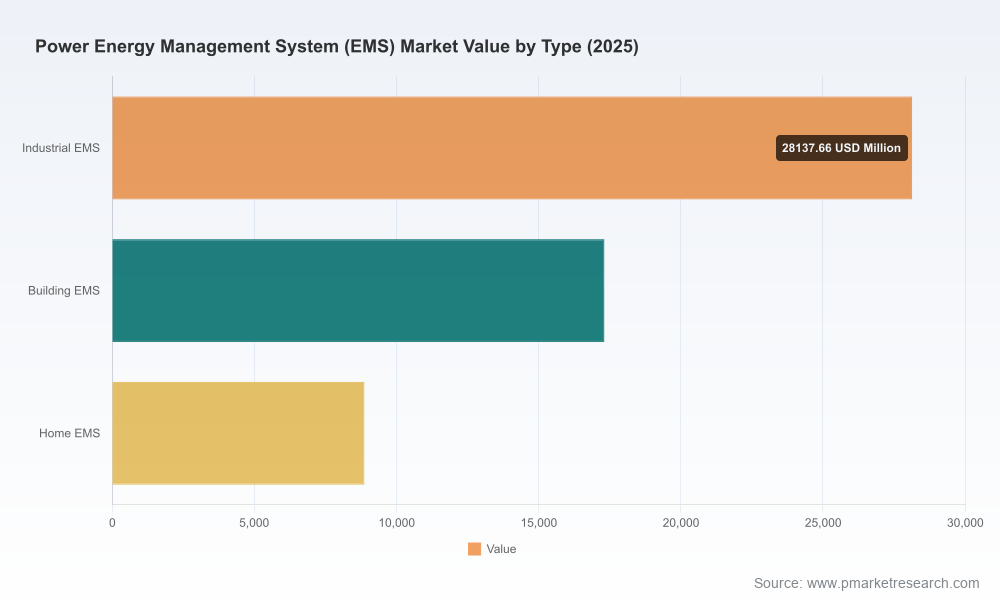

PW Consulting’s latest market study on the Worldwide Power Energy Management System (EMS) market provides a focused, operationally oriented intelligence package designed to shape capital allocation, sourcing, and technology roadmaps in 2026. Built on a 2025 base year and a 2026–2032 forecast horizon, the model captures a market that grew from roughly USD 29.5 billion in 2020 to about USD 54.3 billion in 2025 and is projected to expand to approximately USD 132.0 billion by 2032 — a compound annual growth rate of 13.52%. This trajectory validates EMS as a strategic procurement and investment priority for utilities, industrials, commercial real estate owners, and digital infrastructure operators as they pursue resilience, decarbonization, and distributed energy integration.

Worldwide Power Energy Management System (EMS) Market

Perspective that connects enterprise choices to system-level outcomes: the study translates macro growth and regulatory inflections into actionable scenarios that matter to CFOs, energy managers and CIOs — e.g., how EMS platform selection affects DER integration costs, resilience metrics and compliance exposure.

Worldwide Power Energy Management System (EMS) Market

Decision-ready vendor intelligence: rather than a high-level vendor list, the report provides operational scorecards, deployment archetypes and risk matrices that let procurement teams shorten vendor evaluation cycles and reduce integration uncertainty.

Worldwide Power Energy Management System (EMS) Market

Time-phased implementation guidance: with a clear 2026 vantage point, the report maps where pilot investments should occur this year versus where to commit to scaled rollouts later in the forecast window.

Executive-playbook: a concise, prioritized set of choices for capital projects, vendor selection and procurement clauses (including recommended SLAs and interoperability requirements).

Technology roadmaps: modular architectures for integrating EMS software, edge controllers and services across utility, industrial and commercial estates — including guidance on API-first approaches and data models for DER orchestration.

Vendor scorecards and procurement templates: comparative matrices that assess technology maturity, software licensing models (SaaS vs. on-prem), service capabilities and integration risk — designed to plug into RFP processes.

Regulatory-impact matrix: a concise assessment of near-term compliance drivers (codes, standards, and regional programs) and the design choices needed to mitigate compliance risk while unlocking new revenue streams like VPP participation.

Financial tools: TCO estimators, payback sensitivity models and scenario-based ROI calculators calibrated to short (1–3 year) and medium (3–7 year) investment horizons.

Use-case playbooks: deployment patterns and KPIs for five archetypal buyers (utilities, large manufacturers, data centres, healthcare campuses and commercial portfolios), with failure-mode analyses and mitigation tactics.

Market maps and consolidation watchlist: non-public annexes identifying strategic acquisition targets and partnership opportunities for adjacent software, analytics and DER orchestration providers.

The EMS market’s accelerating growth is driven by a convergence of technology, policy, and demand-side change. Key dynamics include rapid DER penetration and the need for safe, power‑flow based control; grid modernization investments to support electrification and large flexible loads; and enterprise-level decarbonization programs that tie energy management directly to corporate GHG targets. Standards and codes are tightening the compliance envelope, while new grid services such as Virtual Power Plants (VPPs) and frequency response create monetizable pathways for advanced EMS deployments.

Regulatory inflection points: The 2026 National Electrical Code (NEC) update’s relocation of EMS provisions into a new article introduces clear distinctions between EMS and Power Control Systems (PCS), reshaping compliance requirements for DER integration and safety-certified power flow control. Separately, national and regional strategies — from VPP roadmaps to transmission expansion programs — are increasing the operational and economic value of EMS platforms.

Capital and industrial trends: Significant capex for factory modernization and digital service expansion, together with large transmission investment programs in select markets, are expanding addressable demand for EMS functionality beyond traditional utility control rooms.

Commercialization of grid services: Policy and market reforms enabling aggregated DER capacity and ancillary service participation mean EMS platforms are evolving from monitoring tools to revenue-enabling orchestrators.

The market illustrates a mix of established industrial automation leaders, grid-focused integrators and software-centric entrants. Market concentration is moderate: the top three providers account for roughly one‑third of market share, and the top five for just over half, highlighting room for differentiated players and targeted consolidation.

Siemens AG — Munich: a leader in utility-scale EMS with platforms that prioritize grid control, generation and renewables integration. Siemens remains a go‑to for large system operators and major transmission projects where deep domain expertise and scale matter.

Schneider Electric SE — Paris: strong in integrated power management across buildings and electro‑intensive customers. Recent major investments into North American manufacturing and digital services underscore its push to capture service-led growth.

ABB Ltd — Zurich: notable for industrial EMS and real‑time energy optimization in manufacturing and large facilities, with solutions positioned to bridge automation and energy domains.

GE Vernova — Boston: grid solutions and digital EMS offerings aimed at transmission and generation asset owners, with emphasis on integration with fleet management and asset performance systems.

Honeywell, Eaton, Emerson, Johnson Controls, Rockwell, Mitsubishi, Yokogawa and Hitachi Energy — these firms collectively span industrial control, building systems and utility-grade EMS. Each has distinct strengths: Honeywell in industrial optimization, Eaton in reliable distribution hardware integration, Johnson Controls in building energy solutions, and Hitachi Energy in advanced grid stability and renewable integration.

Strategically, incumbent vendors are pairing product roadmaps with services and cloud analytics to defend share, while smaller specialists are focusing on interoperability, AI-driven orchestration and niche market entry via partnerships and regional projects.

CAISO’s EMS upgrade approvals signal ongoing investment by system operators in mission‑critical capabilities and set benchmarks for performance and resilience expected of modern EMS platforms.

Standards updates (e.g., NEC Article changes) are materially increasing the compliance requirements for EMS–PCS interactions; buyers must reconcile product roadmaps with updated safety and interconnection obligations.

Supplier investments and financial performance — including large capital commitments to factory upgrades and double‑digit sales growth in building solutions — indicate supplier focus on North American expansion and service-led revenue models.

Policy trajectories such as national VPP targets and major grid expansion programs are creating near-term procurement opportunities for EMS that support aggregation, market participation and congestion management.

Define use-case first, technology second: start procurement with mapped operational outcomes (e.g., FCR provision, islanding, demand charge reduction) and let those outcomes drive architecture and contractual terms.

Accept modularity as the default: prioritize solutions with open APIs, standard data models and clear edge/cloud delineation to avoid vendor lock-in and to allow phased rollouts aligned with budget cycles.

Consider SaaS plus managed services for early-stage VPP and DER programs to reduce upfront integration risk while retaining pathways to on‑prem control where regulatory or latency constraints require it.

Embed compliance and cybersecurity into procurement: require evidence of NEC/PCS alignment, IEC and ISO conformance where applicable, and include cybersecurity testing and incident-response SLAs in contracts.

Use staged pilots to de‑risk procurement: validate integration, performance and revenue models with short-term pilots linked to measurable KPIs and pre-agreed expansion gates.

Monitor consolidation targets: mid‑sized analytics and orchestration vendors remain attractive acquisition or partnership candidates for incumbents, offering leverage points for rapid capability acquisition.

For 2026 decision cycles, PW Consulting recommends a two-track approach: immediate triage to align existing EMS investments with new code and market participation requirements; and a medium-term program to standardize data, procure modular EMS components and pursue pilots that validate value streams such as VPP aggregation and peak shaving. Detailed, executable guidance — including vendor benchmarks, market forecasts by deployment archetype, and customizable TCO models — are contained in the full PW Consulting report.

To access the full dataset, regional forecasts, vendor scorecards and our scenario-driven financial models that underpin these strategic recommendations, visit the PW Consulting report page or contact our advisory team for a tailored executive briefing. The summary here is purposely concise: the full report contains the granular, actionable intelligence you will need to execute with confidence in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Power Energy Management System (EMS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com