Worldwide Solenoid Reversing Valve Market — Strategic Outlook for 2026

PW Consulting’s newest market study on the Worldwide Solenoid Reversing Valve Market delivers a targeted, decision-ready intelligence package tailored for executives, product leaders, procurement heads, and M&A teams planning actions in 2026. Grounded in a comprehensive base-year review (2025) and a seven-year forecast window (2026–2032), the analysis blends empirical market sizing with supplier benchmarking, cost-sensitivity modeling, and regulatory-risk scenarios to convert market trends into near-term commercial priorities. The global market, measured in USD (Million), reached a robust base in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 5.24% through the forecast horizon — a profile that signals steady growth but also a competitive environment in which timing, supplier strategy, and product positioning will determine winners.

Worldwide Solenoid Reversing Valve Market

Market snapshot: where the industry stands entering 2026

After multi-year expansion through 2020–2025, the solenoid reversing valve market is positioned at an inflection point. Our base-year assessment captures the combined effect of accelerating heat pump adoption, refrigerant transitions toward lower-GWP options and naturals, and incremental improvements in valve materials and controls. The model projects steady growth across 2026–2032 under a medium-risk macro scenario, with a clear upward trajectory in nominal market value by the end of the forecast period. This macro outlook frames 2026 as a pivotal year for capacity decisions, product launches, and supplier consolidation strategies.

Worldwide Solenoid Reversing Valve Market

Dynamics shaping strategic choices in 2026

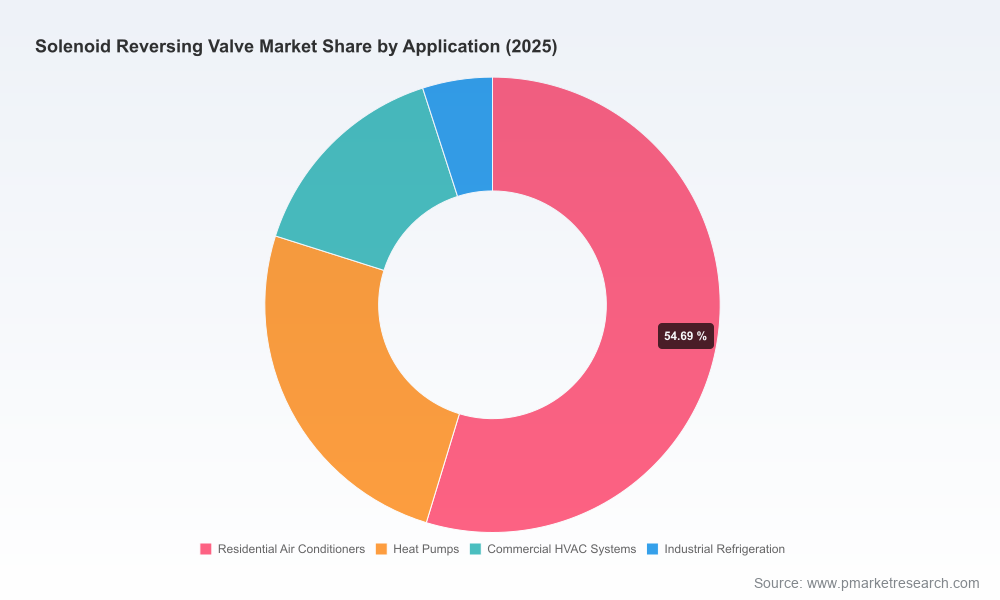

- Technology and product compatibility: Four‑way reversing valves remain central to heat pump and reversible HVAC systems. Vendors that accelerate materials upgrades (stainless constructions, advanced slide and sealing systems) and explicitly certify compatibility with low‑GWP and natural refrigerants will capture early-adopter demand as heat pump conversions accelerate.

- Regulatory and safety constraints: Reversing valves must meet established safety and performance benchmarks across target markets — including recognised UL listings and maximum operating pressure ratings compatible with common refrigerants — and manufacturers that fast-track compliance testing can reduce go‑to‑market friction.

- Raw-material and component cost pressure: The industry is experiencing material-price variability that directly affects valve body and component costs. Spot markets for hot-rolled coil (HRC) steel showed material price swings in 2025 and early 2026, creating a clear incentive to deploy hedging strategies, longer-term purchase agreements, or alternative material sourcing where technically feasible.

- Concentration and channel dynamics: The supply base shows meaningful consolidation; the top-tier suppliers command a high combined market share. This concentration creates dual strategic implications: established suppliers can leverage scale in procurement and R&D, while niche innovators can win share by addressing specialized applications (e.g., geothermal heat pumps, industrial refrigeration).

- Integration of controls and service offerings: The intersection of electromechanical valve design with intelligent controls (position sensing, predictive maintenance) is creating a higher-value product tier. Organizations that align valve hardware with digital service models can expand margins via aftermarket revenues.

What the report delivers — practical, translatable outputs

This study is intentionally operational. It provides the tools and narratives decision-makers need to act in 2026 without wading through raw tables at first glance. Highlights include:

Worldwide Solenoid Reversing Valve Market

- Forward-looking demand model with scenario toggles for refrigerant policy, heat-pump adoption rates, and industrial capex cycles.

- Cost-pass-through templates and sensitivity analyses that translate steel and component price moves into margin scenarios for OEMs and contract manufacturers.

- Supplier heatmaps linking production footprint, technology capabilities, and procurement risk exposure; includes assessment of lead times and single‑sourcing vulnerabilities.

- Regulatory compliance matrix cross-referencing pressure ratings, material certifications, and market-entry requirements across major regulatory regimes.

- Playbooks for product roadmaps (materials, sealing technologies, control integration) and go‑to‑market routes (OEM partnerships, distributor engagement, aftermarket service models).

- M&A screening filters and valuation comparables to support acquisitive strategies in 2026 and beyond.

Competition: where incumbents and challengers are positioning

The market exhibits a clear top-tier of global suppliers and a competitive middle tier of regionally focused specialists. Our competitive benchmarking emphasizes product breadth, manufacturing scale, material-technology leadership, and channel access.

- Sanhua Holding Group (Hangzhou, China): Recognised as a dominant global supplier of four‑way reversing valves for HVAC and heat pumps. Recent product evolution toward stainless-steel ranges and next‑generation series reflects an explicit strategy to align with natural refrigerant compatibility and higher durability expectations.

- Danfoss (Nordborg, Denmark): Offers a wide portfolio spanning solenoids and reversing valves; strengths lie in integrated refrigeration solutions and established OEM relationships in commercial and industrial channels.

- Parker Hannifin (Cleveland, USA) and Bosch Rexroth (Lohr am Main, Germany): Both bring industrial hydraulic and pneumatic valve expertise — an advantage in industrial refrigeration and mobile/industrial applications requiring rugged directional control solutions.

- Robertshaw (Itasca, USA) and Wilspec (Oklahoma City, USA): Specialist players that focus on heat pump reversing mechanisms and geothermal applications respectively; their designs emphasize reliable seasonal switching and application-specific durability.

- DunAn (Zhuji, China), SMC Corporation (Tokyo, Japan), ASCO (Emerson, Florham Park, USA), and Shandong Yikaide: These firms round out the competitive set with scale in OEM supply, pneumatic control interfaces, and hydraulic reversing valves for industrial systems.

Notable recent moves include the release of a next‑generation stainless steel series by a market leader in late 2025 and high-profile trade show participation in early 2026 — activities that signal a shift toward higher‑performance materials and more integrated control demonstrations at customer touchpoints.

Strategic playbook for 2026 — recommended actions

- Prioritise product-certification roadmaps: Expedite UL and pressure‑rating validations that enable cross-market sales and compatibility with emerging refrigerants.

- Mitigate raw-material exposure: Implement purchasing strategies that combine spot-market monitoring, multi-year contracts, and supplier partnerships to smooth cost volatility.

- Segment go‑to‑market by value capture: Differentiate routes for standard HVAC commodity valves versus premium stainless and control-integrated products for heat pumps and industrial clients.

- Accelerate digital service pilots: Bundle sensors and remote diagnostics to create aftermarket revenue and reduce churn for large OEM customers.

- Use concentration metrics to guide M&A and partnership targets: High market concentration at the top creates buy-or-partner opportunities for mid‑tier suppliers seeking scale and for tier‑one players seeking niche tech.

- Operationalize scenario planning: Prepare 90‑, 180‑, and 360‑day response plans for raw material price shocks or supply interruptions that could materially affect 2026 margins.

Why PW Consulting’s report is strategically material for 2026

2026 is a year where product compatibility, sourcing discipline, and channel economics converge. The market trajectory — a steady growth path underpinned by energy-efficiency adoption and refrigerant transition — rewards early movers who can demonstrate certified product performance, secure resilient supply chains, and monetize aftermarket services. PW Consulting’s report converts the underlying numbers and competitive dynamics into executable playbooks: not just who the incumbents are, but how to act against them, when to invest in higher‑value valves, and how to structure procurement to protect margins.

What we intentionally omit from this summary — and why

In keeping with our “trailer” approach, this release showcases the analytical depth and operational relevance of the study while deliberately withholding granular segment-by-segment revenue figures and other proprietary split data. Those guarded deliverables — including region-and-application level revenue breakdowns, customer-level contract exposure, and full interactive financial models — are included in the full report package and in our client workshops, where we walk teams through tailored scenarios and implementation plans.

Next steps

For teams preparing capital allocation, product roadmap decisions, or sourcing actions in 2026, the full PW Consulting report provides the exact datasets, scenario tools, and supplier scorecards necessary to translate this overview into firm decisions. Access to the complete study also unlocks our interactive models and a limited number of bespoke briefing sessions designed to orient leadership teams to the specific risks and opportunities in their operating footprint.

Contact PW Consulting to request the full Worldwide Solenoid Reversing Valve Market report and to schedule a tailored executive briefing that aligns the study’s findings to your 2026 strategy.

For detailed analysis of this topic, please visit the official page:Worldwide Solenoid Reversing Valve Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com