Silicone Fabrics Market: Insights and Competitive Analysis

Other |

2026-03-11 06:42:04

As aerospace and cryogenic applications accelerate into a new phase of programmatic and commercial activity, the market for silver coated FEP (fluorinated ethylene propylene) films is emerging as a strategic input whose availability, specification and total cost materially affect program outcomes. PW Consulting’s new market study — anchored to a 2025 base year and forecasting through 2032 — shows a clear trajectory: the global market expanded from just over USD 100 million in 2020 to roughly USD 144 million in 2025 and is modelled to approach USD 229 million by 2032, reflecting a compound annual growth rate of 6.82% over the 2026–2032 forecast window.

Worldwide Silver Coated FEP Film Market

This briefing highlights why those figures should matter to procurement, product and strategy teams preparing 2026 plans. It also explains what practical insights our full report contains, and why visiting the report page to access the primary datasets and supplier scorecards is a necessary next step for any organization that relies on high‑performance thermal control films.

Worldwide Silver Coated FEP Film Market

Performance leverage: Silver coated FEP films remain a first‑order solution for satellite thermal control, multi‑layer insulation (MLI), second‑surface mirrors and high‑performance cryogenic insulation. Small specification changes (coating type, thickness, overcoat) can materially change thermal emissivity and survivability in severe environments.

Worldwide Silver Coated FEP Film Market

Supply chain sensitivity: Producers are exposed to precious‑metal volatility and specialty polymer supply constraints. Our modelling shows that platinum‑group and silver price movements materially change landed unit costs for prime contractors and integrators, creating budgeting and contractual risk for capital programs beginning procurement in 2026.

Consolidated supplier base: The market demonstrates notable concentration among a handful of established players; the top three firms account for a meaningful majority of supply, and the top five capture an even larger share. That structure creates both stability and potential bottlenecks — a duality that should shape sourcing and contingency plans.

Between 2020 and 2025 the global silver coated FEP film market recorded steady expansion. Our forecast to 2032 projects continued, consistent growth with mid‑single digit CAGR through the forecast horizon. For organizations planning 2026 investments, the implication is twofold: volume demand is growing sufficiently to justify supplier qualification efforts and longer‑duration supply agreements, but procurers must incorporate price and delivery volatility into total cost of ownership models.

Concrete program decisions affected by this outlook include: when to lock multi‑year supply agreements versus spot procure small pilot contracts; how to stage inventory and acceptance testing; and where to prioritize investments in in‑house coating or value‑added finishing capabilities versus outsourcing to established suppliers. PW Consulting’s scenario models translate the headline CAGR and market-size trajectory into discrete budget range outcomes for representative program sizes, enabling finance and procurement to stress‑test capital plans against raw‑material shocks and schedule slippages.

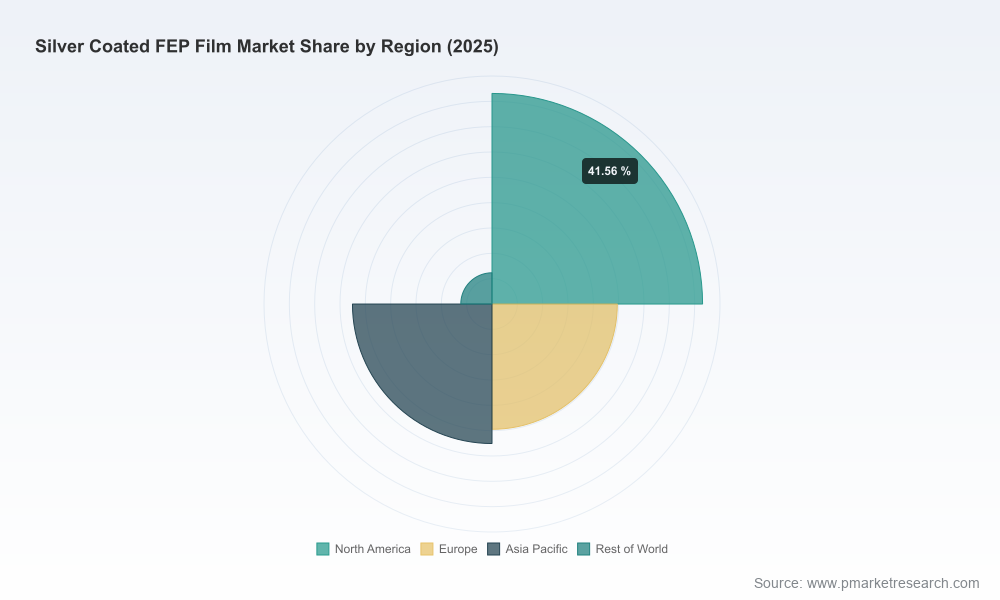

The full report explains market segmentation by region, film thickness and application class and describes how each axis drives different supplier economics and technical requirements. To preserve the strategic value of the study for our subscribers, this briefing intentionally avoids disclosing the granular percentage splits on those segments; however, three broad structural points are essential for 2026 planning:

Different thicknesses and coating technologies (including ITO and dielectric overcoats) are treated as discrete product families by buyers and command distinct qualification paths and price elasticities.

Application demand (satellite thermal control, exploration missions, cryogenics and advanced optics) imposes different warranty, testing and cleanliness specifications — each of which affects lead time and unit cost.

Raw‑material exposure is non‑trivial: industry analyses point to elevated silver prices in 2025 and further upward pressure in early 2026 (consensus forecasts referenced in our supplier risk module point to mid‑range averages around the low‑to‑mid $80/oz band for 2026, with spot spikes reported as high as the mid‑$90s/oz). Our procurement playbook models the impact of these price paths on landed film cost and program margins.

The field is dominated by specialized manufacturers with long experience in aerospace coatings and tight quality processes. Key participants profiled in the report include:

Dunmore Aerospace (Bristol, Pennsylvania, USA) — a longstanding maker of silver coated FEP films and variants (including ITO and SiO2 silver FEP) focused on thermal control, MLI and second surface mirror applications. Their depth of aerospace experience and vertically integrated finishing capability make them a strategic partner for high‑assurance programs.

SQUID3 Space (USA) — a specialist supplier of silver Teflon FEP tapes and ITO coated variants, serving spacecraft thermal control, flexible optical solar reflectors, cryogenic and optical systems for space and defense. Their product set is positioned to serve both bespoke and larger‑volume programs.

Sheldahl (historical operations, Northfield, Minnesota, USA) — historically known for silver coated FEP films and tapes with Inconel overcoat for second surface mirrors and related MLI applications; the company’s legacy technology and installed base remain relevant where heritage specifications dominate procurement choices.

Market concentration metrics in the report indicate a concentrated supplier structure (top‑three share and top‑five share metrics are provided), which suggests buyers should prioritize supplier relationship management, dual‑sourcing where feasible, and structured qualification timelines to mitigate single‑sourcing exposures.

PW Consulting’s study is designed for immediate application in 2026 planning cycles. Among the deliverables and tools included:

Procurement: Initiate hybrid contracting—combine fixed‑price, long‑lead purchase agreements for core volumes with a capped‑spot tranche to capture possible price dips. Build silver price clauses and pass‑through mechanics into master agreements; our templates reduce negotiation cycles.

Supply risk: Qualify at least two suppliers per critical product family and develop a short list for toll‑coating arrangements to add capacity without heavy CAPEX. For mission‑critical programs, consider inventory consignment or strategic pooling with supplier partners to ensure continuity through spikes.

Product strategy: Where thermal performance differentiates product offers, invest in specification testing for advanced coatings (ITO, SiO2 and thin dielectric overcoats) and document the value premium. For cost‑sensitive deployments, standardize on a narrower set of qualified thicknesses to reduce SKU complexity.

Investment & M&A: Focus on targets that either provide additional in‑house coating capabilities, secure upstream polymer feedstock, or offer complementary finishing and assembly services for satellite and cryogenic subsystems.

Commercial alignment: Align proposal timelines with supplier qualification lead times described in this study and price to a conservative silver forecast in 2026 to avoid margin erosion on fixed‑price contracts.

The principal value of this study is operationalization: it translates market forecasts and supplier intelligence into procurement templates, test plans and scenario economics that reduce decision latency. For example, our stress‑testing framework converts a ±20% swing in silver into an explicit impact on program NPV and unit BOM for three archetypal platforms; this allows program managers to set budget contingencies and contractual hedge triggers rather than relying on ad‑hoc responses.

This briefing demonstrates why silver coated FEP film is a lever for program-level strategy in 2026. To access the full report, interactive dashboards, supplier scorecards, and the scenario modelling workbook, visit PW Consulting’s report page. The full dataset includes the detailed regional, thickness and application splits, supplier financials, and downloadable RFP templates that operational teams need to execute in 2026 and beyond.

For procurement, program management and corporate development teams preparing 2026 roadmaps, the comprehensive study and its annexes provide the actionable detail to convert market trends into executable supply and commercial strategies.

For detailed analysis of this topic, please visit the official page:Worldwide Silver Coated FEP Film Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com