Medical Spa and the Art of Subtle Enhancement

Health |

2026-04-01 09:26:47

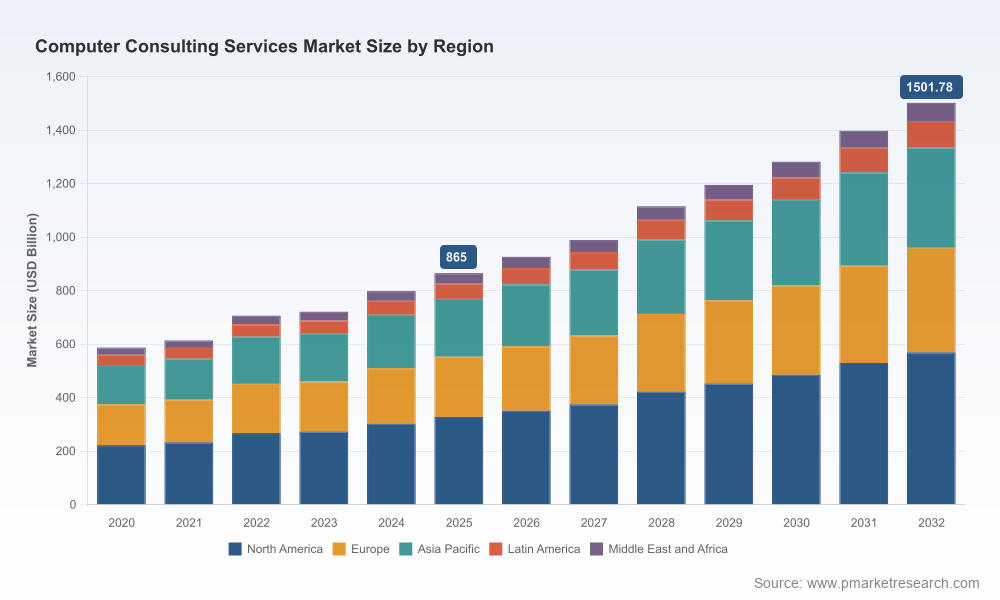

PW Consulting’s new Computer Consulting Services Market report (base year 2025) delivers a forward-looking playbook for enterprise leaders and investors preparing strategic moves in 2026. After a period of steady expansion from 2020 through 2025, the global market reached approximately USD 865.0 Billion in 2025 and is modeled to grow at a compound annual growth rate (CAGR) of 8.2% over the 2026–2032 forecast window, reaching roughly USD 1.5 Trillion by 2032. These headline numbers frame an industry in structural growth as digital transformation, cloud native architectures, real‑time data, and risk-resilient operations converge.

Computer Consulting Services Market

Actionable foresight, not just observation — our report links market trajectories to practical 90‑, 180‑ and 360‑day initiatives that procurement, CIOs, and strategy teams can operationalize immediately.

Computer Consulting Services Market

Regulatory and talent forces are now strategic levers — the study integrates the commercial implications of new compliance regimes and labor dynamics so leaders can align sourcing, pricing, and M&A plans to real constraints.

Computer Consulting Services Market

Vendor consolidation and specialization create opportunity windows — market concentration remains moderate (CR3 ~18.5%, CR5 ~24.1%), signaling buyer leverage but also the incentive for larger firms to accelerate inorganic growth.

Market sizing and forecast model: a transparent methodology anchored to annual historicals (2020–2025) and a scenario-based projection to 2032, enabling stress-testing of demand assumptions under different macro and regulatory shocks.

Go‑to‑market and vendor selection frameworks: vendor segmentation heuristics, decision matrices for build vs. buy, and negotiation playbooks calibrated to both global systems integrators and strong regional specialists.

Commercial and pricing templates: configurable contract language, outcome-based pricing constructs, and implementation milestone structures designed to protect both buyer ROI and vendor margins in long‑duration engagements.

Risk & compliance playbooks: an operational checklist mapping recent regulations to practical controls, audit cadence, and resilience testing approaches suitable for highly regulated industries.

Talent and cost models: integrated salary trajectory inputs and total cost of delivery models that translate labor market movements into program budget impact and vendor sourcing decisions.

Deal and M&A playbooks: criteria for target screening, integration risk profiles, and value-capture roadmaps to convert scale acquisitions into profitable growth.

Note: this public announcement purposefully omits the granular revenue tables and subsegment breakdowns that appear in the full report. Those proprietary tables — including detailed regional, service-type and end‑user splits — are available on the report landing page for clients and subscribers.

Cloud + AI becomes table stakes. Investment decisions in 2026 will be driven by the imperative to operationalize AI on resilient cloud platforms. Real‑time data orchestration and low-latency event-driven architectures are now essential components of enterprise AI delivery.

Data streaming and real‑time platforms accelerate strategic vendor plays. High-profile transactions in early 2026 underscore this trend and validate streaming as a strategic layer in enterprise architectures.

Regulatory resilience is a competitive advantage. With the EU’s DORA in force as of January 2026 and tighter U.S. rules governing bulk sensitive data, consulting engagements increasingly include regulatory remediation, resilience testing, and third‑party risk assurance as core deliverables.

Labor inflation is targeted but skill‑specific. Projected average salary growth in technology roles is moderate, while AI/ML and data science skills are appreciating at a faster clip — forcing firms to choose between localized hiring premiums, offshore/nearshore mixes, or accelerated automation of lower-value delivery tasks.

We profile established strategic vendors and system integrators and assess how their moves will affect buyer choices in 2026.

Accenture (Dublin, Ireland) — continues to lead with broad digital transformation and deep industry practices. Its scale and cross‑industry delivery model make it a go‑to partner for complex modernization programs.

IBM Consulting (Armonk, NY, USA) — positioning itself around hybrid cloud, AI and real‑time data integration. Recent strategic acquisitions highlight IBM’s intent to build a differentiated platform stack for enterprise AI.

Deloitte Consulting (New York, NY, USA) — leverages its advisory footprint to win transformational, cross‑risk engagements that combine strategy, technology and compliance workstreams.

Capgemini (Paris, France) — strong in industry engineering and cloud adoption, with a tighter integration of digital services and domain expertise.

Tata Consultancy Services (TCS) (Mumbai, India) — competing on scale and delivery economics, increasingly moving up the value chain into outcome‑based and productized services.

Cognizant (Teaneck, NJ, USA) — focused on digital engineering and verticalized solutions that pair cloud modernization with business process transformation.

Infosys (Bengaluru, India) — expanding its next‑gen capabilities in AI and cloud via partnerships and selective investments in IP.

Wipro (Bengaluru, India) — pursuing growth through a combination of services innovation and targeted acquisitions to shore up capabilities in cloud and engineering.

These incumbents are complemented by a large and active mid‑tier ecosystem. For clients, the strategic question in 2026 is when to leverage scale partners for end‑to‑end transformations and when to assemble best‑of‑breed specialty vendors to accelerate specific capabilities (for example, real‑time data streaming, cloud security, or generative AI proof-of-concepts).

Major acquisitions in early 2026 emphasize data and real‑time capabilities. Firms that secure platform-level data control will be advantaged in delivering AI at scale.

Regional activity in North America and Europe is increasingly compliance-driven. DORA’s enactment and U.S. rules on bulk data handling make third‑party risk and data governance a top board-level issue for 2026 engagements.

M&A among mid‑tier consolidators signals an opportunity for buyers to demand clearer path-to-value from sellers, including tangible cost offsets and automation roadmaps embedded in deals.

Prioritize near-term investments that unlock enterprise AI: focus first on data lineage, streaming infrastructure, and identity/security plumbing. These create durable optionality for future AI initiatives.

Embed compliance and resilience into transformation contracts. In regulated industries, require vendors to demonstrate DORA‑aligned controls and evidence of bulk‑data safeguards in deliverables.

Adopt a blended sourcing strategy. Use global integrators for platform consolidation and transformational risk, and specialist firms for rapid capability pulls where time‑to‑value matters most.

Reorient talent strategy: protect and grow scarce AI and data engineering skills through targeted premium hiring, rotational programs, and outcome‑linked partnerships with vendors that commit to skill transfer.

Prepare M&A deltas: if pursuing acquisitions, model synergy timelines conservatively and build a 12‑month rapid integration playbook that prioritizes customer continuity and retention.

Our report is deliberately structured to be a strategic toolkit. Clients receive not only market forecasts but a practical set of playbooks: vendor shortlists tailored to industry and program size, regulatory compliance checklists mapped to control objectives, and a set of ready-to-use commercial templates to accelerate contracting with clear risk allocation.

For leaders evaluating next-quarter budgets or multi-year transformation roadmaps, the report supplies the signal-to-noise separation required to make decisive choices in 2026 — while preserving proprietary subsegment detail for subscribers who need the exact inputs for procurement, budgeting, or M&A diligence.

Download the executive brief on our report page for a guided walkthrough of the 8.2% CAGR scenario and the actions we recommend for 2026.

Contact PW Consulting to commission a tailored workshop — we translate the market model into a 90‑day implementation plan aligned to your vendor landscape and regulatory exposure.

PW Consulting — translating market intelligence into executable strategy for ambitious enterprises. For the detailed subsegment tables, vendor scorecards, and industry‑specific playbooks referenced above, please visit the report landing page or contact our advisory team to request access.

For detailed analysis of this topic, please visit the official page:Computer Consulting Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com