Worldwide 2D Ablation Catheter Market — Strategic Preview for 2026 Decision-Makers

Executive summary

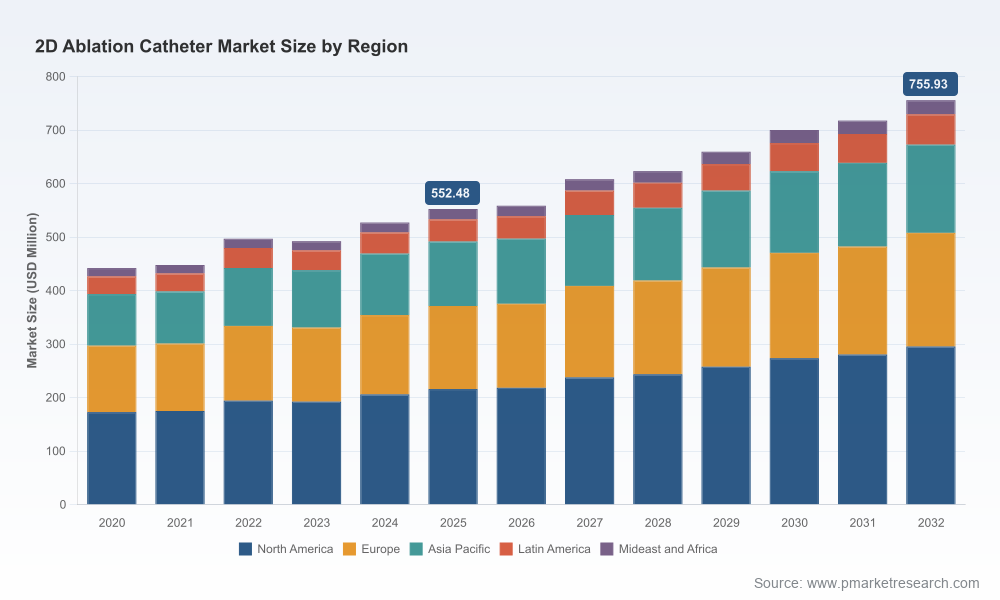

PW Consulting's latest market study on the Worldwide 2D Ablation Catheter market synthesizes clinical, regulatory, commercial and technology signals into an actionable blueprint for corporate strategy in 2026. The market has expanded from roughly USD 442 million in 2020 to about USD 552 million in our 2025 base year, and is forecast to grow at a steady 4.58% CAGR through 2032 — reaching roughly USD 756 million by the end of the forecast horizon. Market concentration is material: the top-three companies account for a clear majority of revenue, and the top-five approach near-complete dominance — a structural reality that shapes competitive tactics, M&A calculus and pricing power.

Worldwide 2D Ablation Catheter Market

Why this report matters for 2026

- It translates macro growth into commercial choices: realistic timelines for new product launches, country entry and scaled manufacturing.

- It aligns regulatory and reimbursement friction points with go-to-market sequences so you can prioritize limited commercial resources.

- It converts clinical innovation trajectories — especially multi-energy platforms (RF, cryo, PFA) and intracardiac echo (ICE) imaging — into addressable opportunities for product, channel and partnership strategies.

Market trajectory and structural implications

The 2D ablation catheter market is exhibiting steady, mid-single-digit growth driven by an aging population, expanding indications for catheter ablation, and continued adoption of image-guided workflows. Our base-year model normalizes historical volatility and clinical adoption curves to present a conservative yet actionable view: from a mid-five-hundred-million dollar industry in 2025, the market grows at about 4.6% annually to approach three-quarters of a billion dollars by 2032. That trajectory supports disciplined investment in differentiated technologies but cautions against broad, undifferentiated capacity expansion.

Worldwide 2D Ablation Catheter Market

Concentration metrics (CR3 ≈ 62.5%, CR5 ≈ 78%) indicate an oligopolistic supply side. Market leaders retain decisive advantages through integrated mapping platforms, broad clinical evidence portfolios and established procurement relationships with hospital systems. For challengers, this means the primary levers are narrow differentiation (technology, cost, service) and selective partnerships rather than competing head-on across every dimension.

Worldwide 2D Ablation Catheter Market

Key dynamics shaping vendor and hospital decisions

- Technology convergence: Electrophysiology is moving to hybrid energy architectures and enhanced imaging. Vendors that bundle mapping, contact-force sensing, energy delivery and 2D ICE guidance create higher switching costs for hospitals.

- Regulatory inertia with tactical openings: In the US, the 510(k) pathway continues to be the main route to market for many catheter and ICE products, with recent submissions emphasizing interoperability with mapping systems. For global players, divergent regulatory timelines (CE, NMPA, FDA) create staging opportunities for launches and evidence generation.

- Reimbursement nuance: Current procedural coding generally does not differentiate energy source or mapping complexity in a way that rewards all incremental functionality. However, specific billing treatments for imaging-only workflows and shifts in practice expense inputs under MS-DRG updates can create pockets of commercial advantage for higher-value, lower-cost workflows.

- Evidence and economics: Payers and hospital procurement increasingly demand demonstrable OR/EP lab efficiencies and patient outcome improvements, not only lesion durability. Cost-effectiveness models that show reductions in repeat procedures or shorter lab times materially influence adoption.

- Robotic and navigation adjacencies: Robotic navigation and magnetic guidance solutions are gaining credibility in complex cases, pushing the value profile from device-only to system-level procedural productivity.

Competitive landscape — strategic read across major players

Our report profiles leading manufacturers and synthesizes strategic implications for 2026. Below we summarize the competitive posture and tactical priorities of core players (profiles in full report).

- Biosense Webster (Johnson & Johnson MedTech) — Strengths: integrated 3D mapping platforms, strong electrophysiology clinician relationships, and new ICE imaging launches that increase procedural visualization. Strategic implication: competing on systems integration and clinician workflow entrenchment; attractive partner for firms seeking mapping interoperability.

- Boston Scientific — Strengths: established RF portfolios with irrigated, contact-force designs and active participation in pulsed field ablation. Strategic implication: focused R&D in energy diversification and continued investments to defend share in core hospital accounts.

- Abbott — Strengths: sensor-enabled contact force catheters and progress in pulsed field ablation regulatory clearances in 2026. Strategic implication: aggressive product evolution combined with broader cardiovascular franchise support to accelerate clinical adoption.

- Medtronic — Strengths: multi-energy systems and cryo platforms with deep hospital penetration. Strategic implication: leverages installed base to convert customers to newer multi-modality offers; pricing discipline and bundled-service go-to-market likely.

- Shanghai MicroPort EP — Strengths: rapid domestic approvals and multi-energy product introductions, plus mapping systems and robotics collaborations. Strategic implication: competitive low-cost alternative in Asia with an eye on technology parity through iterative innovation.

- Stereotaxis — Strengths: robotic magnetic navigation and recent US approvals for specialized use-cases. Strategic implication: appeals to centers of excellence and complex-case specialists; a natural acquisition target for platform players seeking procedural automation capabilities.

- Other players (Biotronik, Japan Lifeline, Osypka, APT Medical, CardioFocus, etc.) — Each brings niche strengths in material science (gold-tip technologies), disposable systems, or PFA balloon approaches. Strategic implication: niche or regional specialists can be attractive M&A targets or partners to fill product gaps.

Recent regulatory and product catalysts — implications for 2026

- Stereotaxis gained US approval for its magnetic interventional ablation catheter for complex congenital cases (Jan 2026) — this accelerates adoption of robotic navigation in specialist centers and raises the bar for systems integration and training support.

- Major vendors launched or expanded 2D ICE and PFA-enabled catheters in 2024–2026, improving imaging clarity and offering alternative energy profiles. These launches shift procurement conversations from "catheter price" to "procedure value."

- CE and NMPA approvals during 2025–2026 for sensor-enabled and PFA devices highlight a widening competitive set outside the US — a reminder that global strategy must be regionally nuanced.

What PW Consulting’s report delivers (practical, not theoretical)

- Robust market model (2020–2032) with scenario analysis: base, conservative and accelerated adoption paths that reflect energy-mix and imaging adoption assumptions.

- Proprietary procedure-volume and pricing models that translate adoption into revenue and unit forecasts at a regional level (full tables available in the report).

- Regulatory pathway maps and a reimbursement playbook that identify timing windows and coding opportunities for differentiated propositions.

- Commercial due-diligence tools: customer segmentation, hospital purchasing behavior, tender mechanics and a practical checklist for KOL engagement and evidence generation.

- Competitive benchmarking and buy-side M&A scorecard to prioritize targets by technology fit, regional footprint and integration complexity.

- Actionable GTM scenarios (three prioritized routes to market per company type) and an implementation roadmap for 12–24 month decision cycles.

Note: To preserve strategic confidentiality and encourage informed acquisition of primary data, detailed regional and application splits are available only in the full report.

Strategic playbook: recommendations for 2026 decision-makers

- Prioritize interoperable solutions: Invest in mapping and ICE compatibility rather than point-functionality. Systems vendors that enable plug-and-play workflows will gain premium pricing and stickier contracts.

- Target differentiated evidence not incremental specs: Focus RCTs or well-designed registries that demonstrate reductions in repeat procedures, lab time or total episode cost — the metrics that matter to procurement committees.

- Stage regulatory rollouts: Use CE/NMPA market entries to de-risk US submissions; sequence clinical publications to support payer conversations ahead of major launches.

- Consider targeted M&A or partnerships: For challengers, acquire narrow technology niches (robotics, ICE imaging, PFA consumables) to accelerate capability without the long tail of full systems development.

- Optimize pricing by procedure economics: Position offers around bundled value — disposables + mapping + training — to capture margin while aligning to hospital KPIs.

- Build sales incentives around lab throughput: Reps should sell time and outcomes, not only device specs. Training and proctoring programs that shorten the learning curve materially aid adoption.

Conclusion — how to use this intelligence in 2026

For executives planning capex, R&D roadmaps, M&A pipelines or commercial deployments in 2026, the PW Consulting 2D Ablation Catheter study provides a tightly calibrated view of where growth dollars will be earned and what capabilities will determine winners. The market’s steady expansion and concentrated supplier base reward focused differentiation, deliberate regulatory sequencing and evidence-led commercialization.

PW Consulting's full report contains the granular datasets, scenario models and supplier scorecards required to operationalize these recommendations. Senior leaders preparing budgets and board materials for 2026 should view this study as a decision-support tool: detailed enough to change plans, high-level enough here to preserve the competitive advantage you will secure by accessing the complete intelligence package.

Next steps

- Request a briefing with PW Consulting to map the model outputs to your P&L and build a 12–24 month strategic plan.

- Commission targeted deep-dives (pricing, regulatory or clinical evidence) that align to your immediate business questions.

- Download the full report to access regional and application splits, company scorecards and the proprietary forecasting workbook.

For detailed analysis of this topic, please visit the official page:Worldwide 2D Ablation Catheter Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com