Microwave Radio Networks Market to Reach $16.32 Billion by 2035

Other |

2026-06-18 10:02:36

PW Consulting’s latest Worldwide Grinding Machine With Moving Table Market report (base year 2025) delivers a forward-looking playbook designed for procurement chiefs, plant managers, investors, and OEM strategists who must make capital and operational decisions in 2026 and beyond. The global market has shown steady expansion from an estimated USD 2,895.4 Million in 2023 to USD 3,145.5 Million in 2025, and our model projects continued growth to about USD 4,309.35 Million by 2032 — an aggregate trajectory driven by a compound annual growth rate (CAGR) of approximately 4.62% across the 2026–2032 forecast window. These topline metrics frame an environment where measured investment, targeted modernization, and supply‑chain resilience separate winners from laggards.

Worldwide Grinding Machine With Moving Table Market

Capital allocation: With moderate, predictable growth and an industry that blends traditional heavy‑duty machinery with rising digital capabilities, 2026 is a year for calibrated CAPEX. Organizations deciding between retrofitting existing fleets versus buying next‑generation machines need granular TCO and productivity evidence — precisely the outputs this report provides.

Worldwide Grinding Machine With Moving Table Market

Cost and input risk management: Upstream material pressures are material to machine builders and end users alike. Our analysis integrates recent commodity movements — for example, iron price benchmarks observed in early 2026 and notable increases in global scrap prices — and translates those dynamics into realistic cost scenarios for machine frames, beds, and structural castings.

Worldwide Grinding Machine With Moving Table Market

Regulatory and operational drivers: Industry 4.0, energy‑efficiency mandates, and workforce constraints are accelerating adoption of IoT, predictive maintenance, and automation in grinding machine fleets. The report quantifies the value levers from reduced downtime, unattended operation, and energy savings that inform 2026 procurement requirements and payback calculations.

PW Consulting designed this report as an applied toolkit for executives who must act in 2026. Key practical elements include:

Raw materials and cost inflation: Benchmarks observed in early 2026 show elevated iron inputs and a rise in scrap values across regions, which meaningfully affect the cost base for machine frames and tables. Buyers and OEMs must bake these inputs into procurement contracts and long‑lead negotiations.

Industry 4.0 and automation: The drive to unattended grinding, predictive maintenance, and process optimization is not theoretical — it is a commercially material productivity lever. Customers are increasingly valuing machines that ship with edge connectivity, analytics packages, and upgrade pathways to digital twins.

Sustainability and energy efficiency: Regulatory momentum toward lower consumption and optimized cooling systems is forcing both OEMs and end users to re‑evaluate machine specifications. Energy‑aware buying criteria are now part of procurement scoring matrices in several major buyer industries.

Aftermarket and services: With moderate market concentration and long equipment lifecycles, aftermarket services (maintenance contracts, spare parts distribution, retrofits) represent an increasingly attractive margin pool and a strategic lever for customer retention.

The grinding‑with‑moving‑table segment is diverse: global multi‑product machine tool groups coexist with specialist builders focused on roll grinding, cylindrical applications, and surface grinding systems. Market concentration is moderate — the top three players account for roughly 31% of the market, while the top five approach the mid‑40s percentile — a structure that supports both competitive pricing and pockets of premium positioning.

Notably, the report documents a recent commercial momentum example: a customer expansion that included a Danobat universal OD grinding machine delivered in March 2026 — a tangible signal of sustained investment in precision capability among gear and transmission manufacturers.

Prioritize retrofit pilots: Run limited retrofit programs that add sensorization and remote monitoring to critical moving‑table grinders to validate predictive maintenance value before committing to full fleet replacement.

Negotiate input‑cost collars and longer lead agreements: Given recent volatility in iron and scrap benchmarks, secure medium‑term supply agreements or price collars for critical castings and structural steel to stabilize CAPEX forecasts.

Adopt modular procurement specifications: Demand modular control and I/O architectures that enable staged Industry 4.0 upgrades; require OEMs to provide transparent upgrade paths and software licensing models.

Align energy targets with procurement scoring: Incorporate measured energy consumption and cooling efficiency into supplier selection to de‑risk compliance with emerging mandates and to capture operating savings.

Build aftermarket strategies: OEMs and service providers should expand predictive service offers and spare‑parts subscriptions; buyers should evaluate service‑level differentiation as part of lifetime cost calculations.

Use M&A and partnerships strategically: For industrial groups seeking footprint or capability expansion, prioritize targets with complementary automation packages, niche roll‑grinding tech, or strong aftermarket networks rather than only volume players.

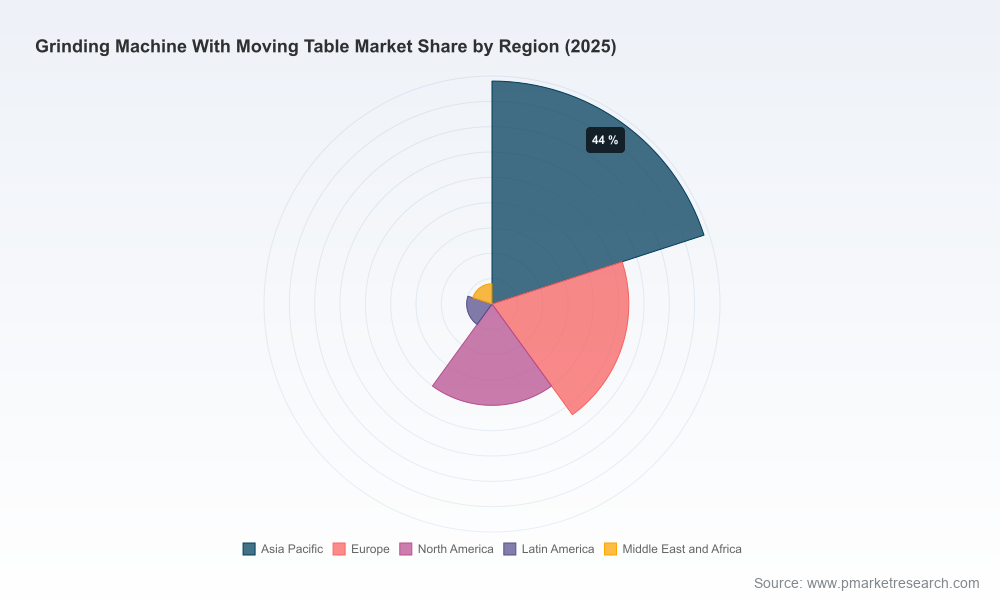

In keeping with the “trailer” principle for this release, we present high‑confidence, executive‑grade findings — but we deliberately withhold the detailed regional and application splits, granular segment price‑by‑model matrices, and the model workbooks that underpin our forecast scenarios. Those deliverables are included in the full report and the accompanying data pack, which also contains downloadable TCO calculators, supplier scorecards, and the complete methodology (primary interviews, plant audits, and bottom‑up revenue aggregation by machine class).

If you are planning capital deployment, supplier consolidation, or a service‑model pivot in 2026, PW Consulting’s full report and bespoke advisory engagements translate the market intelligence above into executable plans: procurement scorecards, retrofit roadmaps, and prioritized supplier negotiations. Contact our Industrial Machinery practice to schedule a briefing or to request the full report and data license.

For detailed analysis of this topic, please visit the official page:Worldwide Grinding Machine With Moving Table Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com