Arrhythmia Monitoring Devices Market Size, Share, Trends, and Forecast by 2032

Other |

2026-07-03 06:34:06

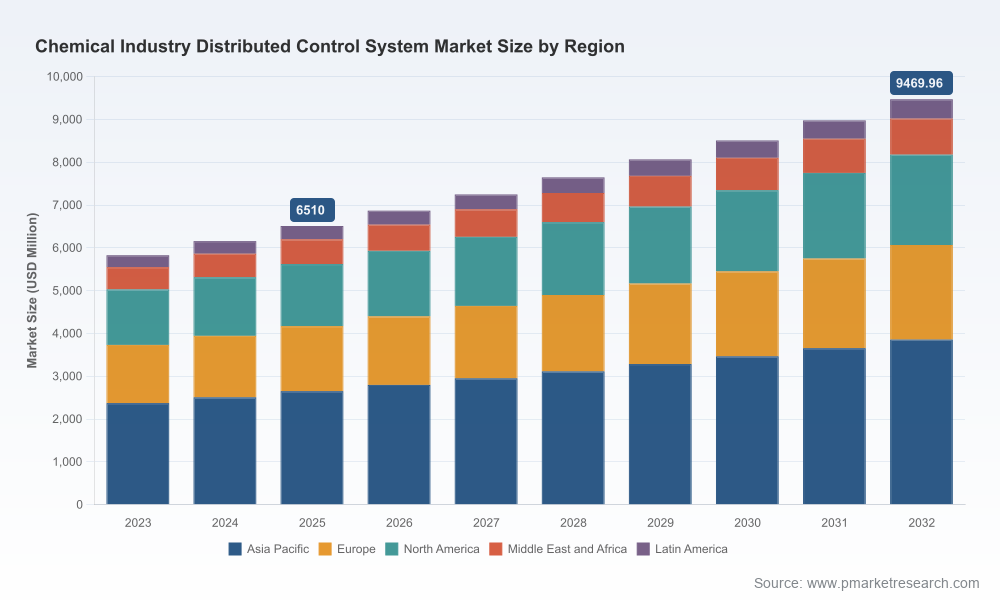

PW Consulting’s new market study on Distributed Control Systems (DCS) in the chemical industry frames 2026 as a pivotal year for operators, system integrators, and technology vendors. Our analysis shows the global DCS market serving chemical manufacturing has matured into a steady-growth segment — reaching USD 6,510 Million in 2025 and tracking to a roughly 5.5% compound annual growth rate (CAGR) across the 2026–2032 forecast window, with a projected market size approaching USD 9,470 Million by 2032. These headline metrics underscore that DCS remains a core investment for process reliability, safety and digital transformation even as vendors and end users re-architect value chains around software-defined automation, cybersecurity and sustainability constraints.

Worldwide Chemical Industry Distributed Control System Market

Timing investment and modernization: With growth steady rather than explosive, 2026 is a year to be surgical about where to commit capital — prioritizing projects that unlock measurable OEE (overall equipment effectiveness) gains, accelerate product quality improvements in specialty and fine chemicals, or materially reduce operating risk.

Worldwide Chemical Industry Distributed Control System Market

De-risking supplier selection: Market concentration indicators show a moderately consolidated vendor landscape. This creates both stability and negotiation opportunity — incumbent vendors bring long-term support and proven PlantPAx/DeltaV/PCS7-class capabilities, while newer software-defined entrants create leverage for price and service innovation.

Worldwide Chemical Industry Distributed Control System Market

Aligning digital and regulatory calendars: Emerging regulatory pressures and decarbonization requirements demand DCS projects to be designed with compliance, traceability and retrofit paths in mind, not as isolated automation upgrades.

This study was built to be a practitioner’s tool. It goes beyond topline forecasting to provide:

A validated market-sizing model (base year 2025) and scenario-based forecasts through 2032 that translate high-level CAGR into capex planning assumptions.

A vendor benchmarking framework that scores suppliers on upgrade/migration support, cybersecurity posture, software licensing flexibility, and lifecycle TCO.

Use-case playbooks for chemical sub-sectors — from high-throughput petrochemical crackers to low-volume specialty chemical batches — showing technology pathways for modernization, integration, and operationalizing AI-assisted control loops.

Procurement and contracting templates (RFP checklists, service-level constructs, and migration phasing plans) to reduce procurement cycle times and lower integration risk.

An operational cybersecurity checklist aligned to software-defined DCS architectures and to regulatory risk scenarios such as refrigerant/chemical handling restrictions that affect plant utility systems and mechanical refrigerants.

ROI calculators and business-case exemplars that help translate controlroom upgrades into ROI timelines and balance-sheet impacts for 3–7 year planning horizons.

The market remains anchored by established automation majors, each carving distinct routes to capture modernization and digital transformation budgets:

Emerson Electric Co. has advanced its DeltaV platform into software-defined capabilities, focusing on batch process control and cybersecurity enhancements that are attractive to complex chemical reaction environments where product quality and traceability are critical.

Honeywell International continues to position Experion PKS as a reliability- and safety-focused DCS, layered with AI-assisted operations to reduce unplanned downtime and support compliance in high-hazard installations.

ABB is emphasizing modernization pathways — enhancing field device integration and OPC UA connectivity — to simplify incremental upgrades in brownfield chemical plants where rip-and-replace is impractical.

Siemens is leveraging its PCS 7 portfolio to bridge today’s control needs with broader digitalization agendas, often tying DCS upgrades to plant-wide digitization in ethylene and large-scale chemical assets.

Yokogawa focuses on durable, long-life DCS architectures and autonomy-enabling features that appeal to operators valuing long-term stability and predictable lifecycle support.

Schneider Electric and Rockwell Automation are both pivoting towards software-defined, flexible DCS offerings and migration toolchains that lower upfront capex and accelerate returns for hybrid process industries.

Japanese incumbents (Mitsubishi, Azbil, Hitachi) continue to provide regionally strong, integrated automation suites that combine DCS core control with plant-level equipment automation for tighter OEE and energy optimization.

Several product releases and upgrades through late 2025 and early 2026 crystallize three strategic shifts:

Software-defined DCS is mainstreaming: Multiple vendors released software-first or software-enhanced DCS versions (notably Schneider’s and Emerson’s product announcements in early 2026). Buyers should interpret this as an inflection point where software licensing models, containerization, and edge/cloud interoperability become central procurement levers.

Modular modernization over greenfield replacement: ABB’s Symphony Plus updates and Yokogawa’s CENTUM refresh emphasize phased modernization and device-level connectivity — a strong signal that vendors expect more brownfield modernization demand than wholesale system replacement.

Security and autonomy are table stakes: Across upgraded releases there is consistent embedding of cybersecurity features and autonomy-enabling capabilities, reinforcing the view that any future-proof DCS must couple resilient control with secure, data-rich operations.

Regulatory actions — for example the phasedown of certain high-GWP refrigerants under recent U.S. environmental measures — have operational knock-on effects that reach into DCS planning. Changes in refrigerant usage, HVAC systems and other utility controls can trigger DCS I/O changes, new interlocks, and compliance monitoring requirements. Our report maps scenarios where regulatory-driven retrofits alter project scopes and recommends contingency allowances in project budgets and timelines to avoid scope creep and late-stage compliance headaches.

We recommend a three-step, risk-calibrated decision framework for chemical operators and technology investors in 2026:

Assess (0–3 months): Perform a control-system risk and value audit that links DCS capability gaps to product quality, safety and regulatory risk. Use a vendor-agnostic checklist to quantify lifecycle costs, cyber maturity, and upgrade complexity.

Prioritize (3–9 months): Rank projects by expected value realization — favor staged modernization in brownfield assets that deliver near-term OPEX reductions or safety risk mitigation. Allocate a portion of the modernization budget to cyber hardening and to integration middleware that supports multivendor coexistence.

Execute (9–36 months): Adopt phased rollouts with factory acceptance testing, fallback strategies, and managed services contracts that guarantee long-term patching and support. Negotiate contractual rights for containerized deployments and define clear exit and migration clauses to prevent vendor lock-in.

Licensing and deployment flexibility: Favor offerings that support hybrid on-premise/cloud architectures and clear licensing for virtualized/edge environments.

Migration tooling and brownfield expertise: Choose partners with proven cutover methodologies and strong local systems-integration ecosystems to reduce downtime risk.

Cybersecurity commitments and SLA clarity: Demand explicit, measurable security SLAs and transparency on patch cadences and incident response playbooks.

Open data and interoperability: Prioritize vendors embracing standards (e.g., OPC UA) and offering open APIs to enable data-driven operations and third-party analytics.

Market concentration metrics indicate that the largest three players control a meaningful portion of the market, with the top five increasing that share further. For purchasers, this means suppliers bring scale and deep domain expertise, but there is also leverage for buyers willing to evaluate newer, software-centric providers. Our recommended negotiation posture is to use staged pilots and proof-of-value projects to validate claims, then apply competitive leverage to secure favorable licensing, maintenance and migration terms.

PW Consulting’s Worldwide Chemical Industry Distributed Control System Market report is written to be prescriptive: to turn market insight into executable plans. The full report includes detailed segmentation analyses, vendor scorecards, scenario modeling (including sensitivity to regulatory shocks and supply-chain volatility), and downloadable tools to build your own capex and ROI cases. To access the complete dataset, methodology and proprietary appendices — including actionable procurement templates and risk matrices — visit the PW Consulting report page.

For 2026, DCS is no longer a purely operational technology line item — it is a strategic lever for compliance, resilience, and product differentiation in chemical manufacturing. With a stable growth profile underpinned by a 5.5% CAGR and a market approaching USD 9,470 Million by 2032, the right mix of modernization, cybersecurity, and vendor strategy will determine which operators convert automation spend into measurable enterprise value. PW Consulting’s report is designed to accelerate that conversion by giving decision-makers the frameworks, vendor intelligence and practical tools needed to act with confidence in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Chemical Industry Distributed Control System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com