Beverage Industry Modernization Fueling the Carbonated Beverage Processing Equipment Market

Networking |

2026-06-12 07:35:23

PW Consulting’s newest market study on Worldwide Laminating Lithium‑ion Capacitors (base year 2025; forecast period 2026–2032) provides a concise, actionable intelligence package for executives who must decide on investment, sourcing, product roadmaps and M&A priorities this year. The laminated LIC market is on a rapid growth trajectory: our topline model shows revenue rising from USD 456.28 Million in 2025 to USD 1,500.67 Million by 2032 under the base forecast, reflecting a compound annual growth rate (CAGR) of 18.54% across the forecast window. This briefing highlights the strategic implications embedded in the report while preserving the proprietary segmentation detail that PW Consulting reserves for report subscribers.

Worldwide Laminating Lithium-ion Capacitor Market

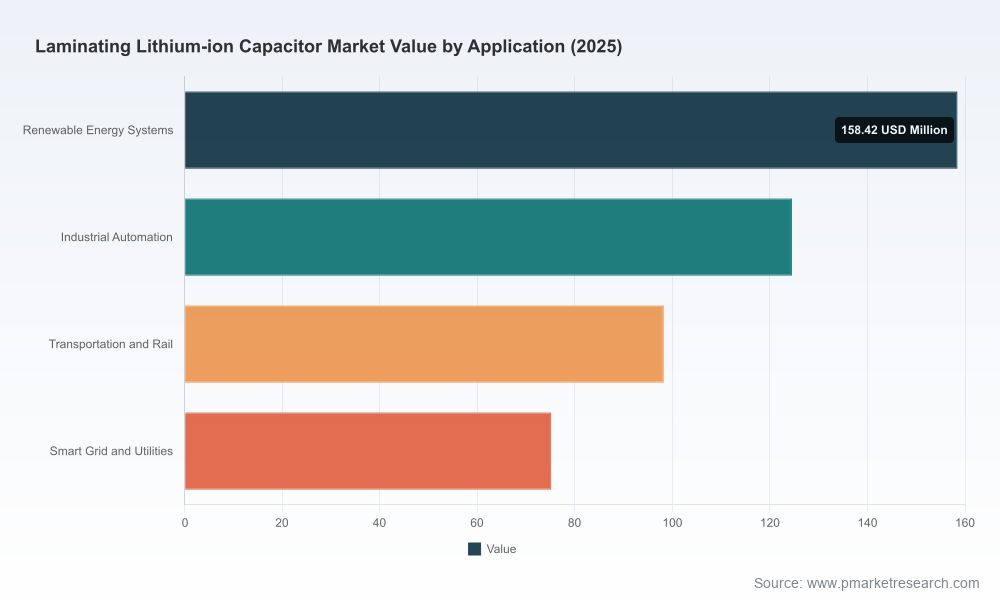

Fast-moving demand dynamics. Multiple end-markets — from renewable energy buffering to industrial automation and transportation — are shifting buyer priorities toward laminated pouch-form LICs because of their volumetric efficiency, cycle life and fast‑charge capability. The market’s near‑term expansion creates windows for first‑mover scale advantages and late‑mover niche plays.

Worldwide Laminating Lithium-ion Capacitor Market

Capital allocation decisions must be precise. With market value projected to more than triple from mid‑2020s levels by 2032, capital deployed into production lines, process licenses and supplier relationships will compound. Our models translate aggregate growth into staged capex and breakeven schedules for laminated manufacturing options.

Worldwide Laminating Lithium-ion Capacitor Market

Supply chain and raw material tension. The industry’s dependence on activated carbon precursors and lithium pre‑doping techniques introduces both cost and availability risk. Buyers and producers that secure resilient, flexible supply strategies will preserve margins as volumes rise.

Transparent top‑down and bottom‑up market sizing (historical 2020–2025 and forward to 2032) with scenario variants that isolate demand drivers by technology readiness, certificate timelines, and OEM adoption curves.

Proprietary financial templates: stepped capex schedules for laminated pouch production, unit economics by cell format, sensitivity models for key inputs (activated carbon, pre‑doped lithium, packaging), and go/no‑go thresholds for greenfield vs contract manufacture.

Supply‑chain heatmaps and nearshoring opportunity matrices that rank geographies by input security, tariff exposure, logistics cost and workforce readiness—built to be integrated into procurement RFx and board‑level playbooks.

Technology and manufacturing playbooks: practical guidance on licensing options, dry electrode vs wet processes, lamination process control, roll‑to‑roll conversion economics, and quality assurance checkpoints needed to meet industrial and automotive requirements.

Commercial and regulatory roadmaps that align certification timing (safety listings, UL/ETL analogues, automotive Q‑series) with product launches, minimizing time‑to‑market risk.

Competitive benchmarking and M&A pipeline: scored profiles of established producers, scale challengers and component specialists, plus a screened list of potential bolt‑on targets for three archetypal buyers (materials company, battery OEM, systems integrator).

The laminated LIC market exhibits moderate to high concentration: the top three incumbents account for a material majority of revenue, and the top five approach three‑quarters of industry receipts. That concentration has two implications: first, selective scale plays can deliver meaningful pricing power; second, specialized technology or process niches remain available for challengers to exploit.

LICAP Technologies, Inc. (Sacramento) — strength in dry activated electrode processes and rapid scale‑up capability. Recent facility expansion in early 2026 and announced manufacturing collaboration with Nissan demonstrate a transition from pilot to commercial scale for automotive and grid markets.

Musashi Energy Solutions / JM Energy (Japan) — established mass production footprint for hybrid supercapacitor/LIC formats and demonstrated product safety certification useful for energy storage system OEMs.

SPEL Technologies (India) — competitive on cost and thin‑form pouch products; a compelling partner for companies seeking low‑cost, high‑throughput laminated supply in Asia.

VINATech (Korea/Vietnam), JTEKT (Japan), Taiyo Yuden (Japan), and several China‑based producers — collectively represent the spectrum of process approaches (laminated pouch, prismatic, cylindrical) and the tradeoffs between volumetric energy, power density, thermal tolerance and manufacturing maturity.

Smaller specialists and regional players (including boutique European and North American providers) fill the high‑power, high‑reliability niche for industrial, rail and defense applications.

Facility and process investments are accelerating: a notable U.S. player expanded manufacturing footprint in March 2026 to scale dry electrode production—an inflection that reduces cost and delivery risk for domestic OEMs.

Industrial certifications are gating adoption: a Japanese supplier received a major energy‑storage safety listing in 2025, underscoring that certification timing can be the difference between winning system‑level contracts and losing them.

Collaborative manufacturing advances (e.g., partnerships between material innovators and automakers) are shortening commercialization cycles for laminated LIC designs and create templates for OEM‑supplier partnerships.

The laminated LIC ecosystem is sensitive to a few concentrated inputs. Activated carbon remains a dominant electrode precursor: industry sourcing in 2024 showed heavy reliance on biomass‑derived feedstocks, with coconut‑shell based activated carbon representing a substantial share of supply. Current pricing pressure—market prices sitting above the long‑run economic threshold for many cell designs—highlights the need for multi‑tier sourcing and process innovation.

Raw material stress test. Build purchase and hedging strategies around activated carbon at current market prices, with break‑evens modeled for <$10/kg recovery scenarios versus present reads (~$15/kg in many markets).

Tech licensing as a lever. Industry licensing of lithium pre‑doping technology has started to lower capex and process complexity for LICs; selective licensing or collaboration can remove barriers for firms adopting standard battery equipment.

Geopolitical mitigation. Tariff dynamics and critical‑material geopolitics mean advanced buyers should evaluate nearshoring/dual sourcing for strategic components, and incorporate tariff pass‑through into pricing models.

We model three practical scenarios that materially alter optimal strategy:

Base Case (our central forecast): sustained adoption across renewable integration, industrial automation and transit accessory markets drives an 18.54% CAGR from 2026 to 2032. This supports staged greenfield investments and selective supplier contracts tied to volume milestones.

Upside Case: faster certification and EV/hybrid vehicle accessory adoption drive earlier replacement cycles and premium pricing for high‑power laminated forms; strategic buyers should front‑load capacity and accelerate vertical integration.

Downside Case: prolonged raw material shortages or protectionist measures raise costs and extend qualification timelines; operational flexibility and contract manufacturing become preferred tactics.

OEMs (automotive, energy systems): prioritize design‑for‑supply with laminated LICs where cycle life and fast response are differentiators; lock conditional offtake with producers that have certification roadmaps.

Component and materials suppliers: invest in carbon feedstock diversification, pilot partnerships on dry electrode processes, and evaluate licensing pathways that unlock larger production addresses.

Investors and strategic acquirers: focus on mid‑market suppliers with scalable laminated lines, proven quality systems and regional footprint advantages; use our M&A scorecard to triage targets.

Contract manufacturers and EMS players: offer turnkey laminated cell lines with demonstrated process control and inspection suites to capture OEMs unwilling to commit to greenfield capex.

Week 1–4: Plug the provided financial templates into current product roadmaps to derive break‑even production volumes and sensitivity to activated carbon pricing.

Week 5–8: Run supplier heatmap exercises using our procurement framework to identify three primary and two alternate suppliers with delivery and tariff strategies aligned to your launch calendar.

Week 9–12: Execute a go/no‑go board briefing built from our scenario outputs and M&A shortlist; finalize certification and sample schedules with preferred suppliers.

The laminated lithium‑ion capacitor market is entering a phase in which timely investments and smart supplier relationships will define winners and losers. With market size expanding rapidly from mid‑2020s levels to well over USD 1.5 billion by 2032 under our base forecast, the choices companies make this year about technology, supply partners, and siting will materially affect market share and margins over the next decade. PW Consulting’s report packages the models, scenario stress tests and transaction playbooks needed to make those choices with confidence.

To access the full dataset, segmented intelligence and executable M&A/partnering lists that underpin these findings, visit the PW Consulting report page for Worldwide Laminating Lithium‑ion Capacitor Market. Our team is available for executive briefings, customized scenario work and procurement workshops to translate insight into a 100‑day implementation plan.

For detailed analysis of this topic, please visit the official page:Worldwide Laminating Lithium-ion Capacitor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com