Global Dried Grapes Market Expands with Rising Natural Food Consumption

Other |

2026-05-04 13:03:00

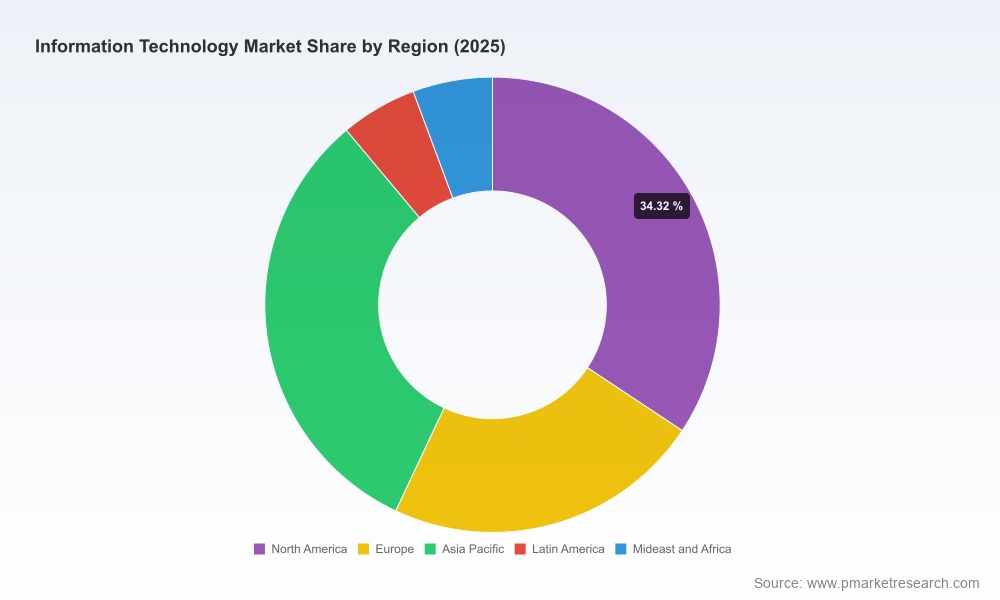

PW Consulting’s latest Worldwide Information Technology Market report (base year 2025, forecast 2026–2032) crystallizes what corporate leaders must understand as they commit capital, partnerships, and talent in 2026. The global IT market crossed roughly USD 5.7 trillion in 2025 and — with a modeled compound annual growth rate of 8.25% — is on a trajectory toward nearly USD 9.9–10.0 trillion by the end of our 2032 forecast horizon. These headline metrics reflect not only scale but a window of strategic opportunity: the market is large, accelerating, and structurally evolving in ways that will rewrite sourcing, product roadmaps, and competitive moats for the next decade.

Worldwide Information Technology Market

Actionable foresight, not abstraction — We translate macro growth into decision-ready scenarios (capital phasing, procurement schedules, partner selection frameworks, and risk buffers) that CIOs and CFOs can apply immediately in 2026 planning cycles.

Worldwide Information Technology Market

Correlated signals across supply, demand and policy — The report triangulates vendor moves, infrastructure investment trends, and regulatory headwinds to produce prioritized strategic imperatives rather than a long list of technobabble.

Worldwide Information Technology Market

Practical toolkits — We provide templates for total cost of ownership modeling, phased cloud migration playbooks, AI-readiness assessments, and vendor negotiation checklists designed for use in board-level and procurement processes.

The 2025 baseline and the 8.25% CAGR establish a planning envelope that is both growth-enabling and materially uncertain. In short: the market is expanding fast enough to warrant accelerated investment, yet diffuse enough that single-vendor bets or rigid long-term CapEx without modular flexibility are risky. Our analysis also shows a relatively decentralized vendor footprint — concentration metrics indicate that even the largest vendors together do not dominate the space, underscoring the importance of ecosystem orchestration rather than outright vendor consolidation strategies.

AI as an infrastructure multiplier — AI deployment is the leading demand driver for 2025–26, catalyzing cloud consumption, specialized accelerators, and data center modernization. The effect is multiplicative: investments in compute and storage ripple into software, services, and managed operations.

Hardware and semiconductor tailwinds with supply constraints — Broader industry forecasts point to unprecedented growth in semiconductor revenues and concentrated investment in memory and accelerators. Enterprises must plan for price volatility and longer lead times, building sourcing resilience and expanding procurement windows.

Hybrid-edge architectures mainstream — Firms are shifting from “cloud-first” to “cloud-AND-edge” architectures to balance latency, cost, and data sovereignty. This architectural shift changes vendor selection criteria and emphasizes interoperability and orchestration capabilities.

Regulatory and geopolitical friction — Tariff policy, export controls and localization requirements are elevating the premium on supply chain transparency, multi-sourcing, and sovereign cloud strategies.

Sectoral capex reallocation — Telecom, hyperscalers and service providers are accelerating investments in fiber, data centers and network densification driven by AI workloads and rising connectivity demand.

Executive synthesis — Top-line implications for board-level strategy and 90-day priorities for CIOs and CDOs.

Methodology and macro model — Transparent assumptions and scenario variants for topline sizing (base, upside, downside), including sensitivity tests you can re-run with your own inputs.

Demand-driver deep dives — Use-case economics for AI, cloud migration, workplace modernization, and industry-specific digitalization (finance, healthcare, retail, manufacturing).

Vendor landscape and competitive playbooks — Strategic positioning, capabilities matrix, and ‘when to partner vs build’ guidance for platform vendors, services firms and specialist hardware providers.

Procurement and contracting playbooks — Clause-level guidance for SLAs, data residency, supply-chain contingency clauses and performance-linked commercial terms.

IT operating model templates — Phased migration plans, organization and talent mapping, and cost-to-serve calculators for hybrid operations.

Risk and scenario annex — Geopolitical, regulatory and supplier failure scenarios with quantified financial exposure models and recommended mitigation paths.

The global IT vendor ecosystem is diverse and evolving into differentiated specialist clusters alongside broad horizontal platform providers. Rather than grade vendors on a single dimension, effective strategy requires mapping them against four business functions: platform and infrastructure provision, AI and compute enablement, enterprise applications and workflows, and systems integration & managed services. Below is a concise strategic read on core players you will encounter in our vendor playbooks.

Platform & Productivity Titans — Microsoft remains central for enterprises that prioritize integrated productivity and hybrid-cloud stacks. Its strength lies in unifying identity, collaboration, and cloud infrastructure for enterprise consumers.

Hardware-OS Ecosystems — Apple continues to push in premium device ecosystems and silicon optimization; for industries where endpoint security and integrated hardware/software experiences matter, its role is strategic rather than purely transactional.

Cloud Infrastructure Leaders — AWS and Google Cloud persist as the primary global infrastructure providers; their differentiation in data services, AI toolkits and global footprints will determine networked enterprise architectures.

AI compute and platform accelerators — NVIDIA has become the de facto standard for high-performance AI compute stacks; enterprises with serious AI ambitions must plan around its roadmap and the broader accelerator ecosystem.

Enterprise software and databases — Oracle and SAP continue to anchor large transactional applications and ERP deployments; the strategic questions for 2026 are how these platforms evolve into cloud-native, composable services.

Services and systems integration — Accenture, TCS and Infosys lead in large-scale transformation execution. Their value proposition is increasingly judged on rapid AI ops, cloud migration velocity, and the ability to operationalize data governance at scale.

Hybrid and specialist incumbents — IBM retains strengths in hybrid cloud and industry-tailored offerings (and in areas like quantum and niche AI tooling), while Oracle and SAP double down on autonomous operations for enterprise systems.

Crucially, market concentration remains relatively low compared with many other tech sectors — the top vendors do not command a majority of the market on their own. That fragmentation creates room for bespoke partnerships, targeted acquisitions, and vendor arbitrage in 2026.

Prioritize modular capital allocation — Stage CapEx into convertible tranches tied to performance gates for AI pilots and data center modernization to avoid being locked into suboptimal hardware cycles.

Mandate vendor interoperability and exit options — Procurement must insist on standardized APIs, data exportability, and pre-agreed migration pathways to prevent strategic lock-in as platforms proliferate.

Operationalize AI governance now — Adopt model lifecycle management, data lineage, and validation frameworks to move from experimental kits to safe, auditable AI services.

Build supply-chain resilience roadmaps — Diversify component sourcing, expand strategic inventory for critical parts, and use multi-region cloud and data strategies to mitigate tariff/regulatory shocks.

Re-skill and re-organize — Embed cloud, AI and data engineering capabilities into business units with clear accountability for outcomes rather than relying solely on centralized IT.

Beyond strategic counsel, our report is paired with implementation modules: bespoke scenario modeling workshops, vendor negotiation support, and deployment acceleration squads that co-manage the first 90–180 days of rollout. We help executives convert the forecast envelope into executable, measurable roadmaps aligned to both growth and risk tolerances.

This article is a strategic preview designed to inform board and executive conversations as you prepare 2026 budgets and transformation programs. The full PW Consulting Worldwide Information Technology Market report contains granular tables, regional and segment breakouts, vendor heatmaps, downloadable TCO models and scenario worksheets — all curated to support procurement, IT, and corporate-strategy teams.

To access the complete dataset and toolkits, please visit the report page on PW Consulting’s website. Our analysts are also available for briefing sessions tailored to your industry vertical and transformation timeline.

PW Consulting — translating market scale into decisive, executable strategy for the enterprise. Make 2026 the year your IT investments unlock sustained competitive advantage.

For detailed analysis of this topic, please visit the official page:Worldwide Information Technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com