Worldwide Aircraft Windows Market 2026: Strategic Briefing for Decision-Makers

Executive snapshot

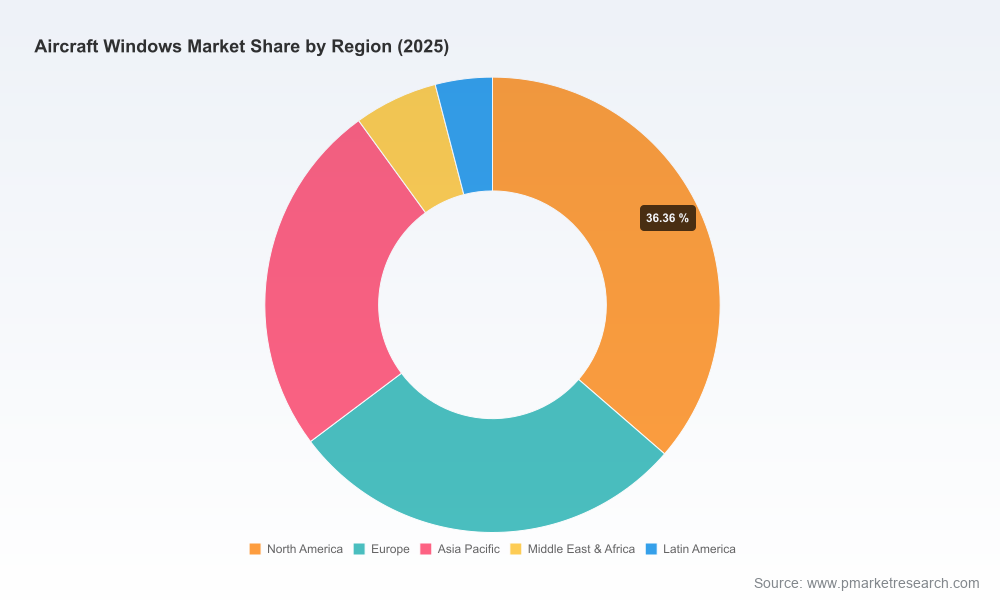

PW Consulting’s new Worldwide Aircraft Windows Market report (base year 2025; forecast 2026–2032) provides pragmatic, board-ready intelligence for executives shaping 2026 strategies across OEMs, Tier‑1 suppliers, materials producers, MRO operators, and investors. Our analysis estimates the global aircraft windows market reached USD 868.42 Million in 2025 and, under a central-case projection, will grow at a 4.25% CAGR through 2032 — reaching a market value in excess of USD 1.16 Billion by the end of the forecast horizon. The trajectory from 2020 to 2025 shows steady recovery and structural uplift, and the 2026 inflection point will reward decisive, insight-driven action.

Worldwide Aircraft Windows Market

Top-line implications for 2026 decision cycles

- Demand continuity driven by sustained passenger traffic growth and robust narrowbody deliveries underpins near-term replacement and new-build windows procurement.

- Materials choices and coating capabilities will materially influence competitive positioning — both for OEM win rates and aftermarket margin capture.

- Regulatory pressure (FAA / EASA) is increasing windshield replacement cadence for certified fleets; MRO and parts suppliers should treat compliance cycles as recurring revenue levers.

- Market structure favors established transparency specialists, but targeted niches (business aviation, eVTOL/advanced air mobility) present fast-moving entry points for agile challengers.

Market dynamics: the forces shaping supplier economics in 2026

Three structural dynamics will shape supplier and buyer economics in 2026:

Worldwide Aircraft Windows Market

- Fleet growth and retrofit tailwinds. Global passenger demand projections and OEM delivery plans sustain both OEM windows orders and retrofit/MRO demand. Narrowbody production recovery creates predictable replacement and upgrade cycles that underpin multi-year procurement plans.

- Materials and weight optimization. Acrylics, glass laminates, and polycarbonate solutions present distinct trade-offs between optical fidelity, weight, and lifecycle costs. Lightweight polymer solutions continue to be attractive for fuel-efficiency programs and urban/advanced air mobility platforms, while glass-based laminates retain a premium position where optical performance and scratch resistance are prioritized.

- Regulation and safety-driven maintenance. Certification authorities are tightening oversight on windshield integrity and visibility standards; this elevates the commercial value of certified repair capability, aftermarket parts availability, and traceable supply chains.

Competitive landscape — who matters and why

The supplier universe is a mix of diversified coatings and materials players, specialist transparency manufacturers, and aftermarket/MRO service houses. The market demonstrates a concentration where a small set of established players control a meaningful share of production and aftermarket flows, creating both barriers and predictable sourcing pathways for airframe OEMs and airlines.

Worldwide Aircraft Windows Market

- PPG Aerospace (United States). A leading presence in OEM and aftermarket transparencies, PPG’s strength is dual: material science (coatings and UV-blocking technologies) and wide aftermarket reach. Their coatings roadmap is a differentiator for fleets targeting lifecycle performance and passenger comfort.

- GKN Aerospace (United Kingdom). Globally competitive in military transparency systems and a major commercial transparency supplier, GKN combines scale manufacturing with legacy relationships across airframers and defense procurement channels. Their in-service base supports aftermarket and MRO capture.

- Saint-Gobain Aerospace (France). Deep optics and laminate capability, combined with strategic partnerships in advanced air mobility (notably ongoing collaboration to supply transparencies for eVTOL programs), position the company to bridge conventional commercial demand with emergent platforms.

- Lee Aerospace, The NORDAM Group, Gentex and specialized regional players. These firms dominate FAA‑approved general and business aviation niches, and are critical service providers for operators seeking certified upgrades and rapid turn MRO. Their capability portfolios are attractive acquisition or partnership targets for companies seeking to expand aftermarket footprints.

- Specialist fabricators and PMA manufacturers. Long-tenured PMA suppliers to the GA market provide low-cost, compliant alternatives for older fleets; they are an important channel for spare-parts demand and liquidity in aftermarket pricing.

Strategic readers should note: partnerships between transparency specialists and new OEMs in advanced air mobility are accelerating. These alliances create cross-sector technology transfer opportunities — particularly for coatings, multi-layer laminates, and sensor-integration into transparencies.

Report contents — what PW Consulting provides to practitioners

The report is intentionally operational: it does not stop at insight, it supplies decision-ready tools and playbooks. Highlights include:

- Proprietary market sizing and a transparent forecasting model (2020–2032) with scenario toggles for production, retrofit, and MRO trajectories.

- Supply‑chain and raw material sensitivity analysis mapping acrylic, polycarbonate and glass laminate cost exposures and substitution thresholds.

- Regulatory impact matrix that translates FAA/EASA policy shifts into replacement-cycle assumptions and CAPEX timing for operators and MROs.

- Competitive scorecards and supplier heat-maps that evaluate manufacturing scale, coating IP, certification breadth, aftermarket reach, and strategic partnerships (includes diligence-ready profiles of leading players).

- MRO demand model: fleet-level replacement curves, parts consumption rates, and service-window economics to support pricing and capacity planning.

- Investment and M&A playbook: target archetypes, valuation pointers, and integration checklists for firms seeking to buy into niche segments or expand aftermarket capability.

- Commercial go-to-market modules for entrants into advanced air mobility and business aviation with commercial templates, sample RFx language, and certification timeline benchmarks.

Practical strategic recommendations for 2026

Our consulting work with OEMs, suppliers and MROs suggests five immediate, high-impact moves for 2026:

- Prioritize materials R&D linked to operating economics. Suppliers should allocate near-term capex to coatings and polymer formulations that demonstrably reduce weight or extend service life; buyers should include explicit lifecycle performance clauses in supplier contracts.

- Monetize regulatory-driven replacement cycles. MRO providers and parts suppliers should proactively build capacity and digital traceability to capture predictable replacement work born of heightened certification scrutiny.

- Segment go-to-market by platform maturity. Differentiate commercial strategies for narrowbody, widebody, business aviation and emergent AAM platforms — each demands tailored certification, pricing, and lead-time models.

- Use partnerships to bridge capability gaps quickly. Where internal R&D timelines are long, strategic partnerships (or bolt-on acquisitions) provide faster access to coatings IP, sensor integration, and certification expertise — especially relevant for suppliers targeting eVTOL transparencies.

- Lock down supply-chain visibility on critical polymers. Raw material availability and price volatility can compress margins; advanced procurement hedging and dual-sourcing are simple but underused mitigants.

Why PW Consulting’s report matters for capital allocation in 2026

Capital deployed without market-validated scenarios is high risk. Our forecast, combined with supplier scorecards and MRO demand modeling, provides the fact base CFOs and corporate development teams need to size investments in capacity, acquisitions, and R&D. For private equity and strategic investors, the report surfaces consolidation targets, margin pools in aftermarket services, and the timing of regulatory-driven replacement cycles that convert into predictable cash flows.

A final word — what we leave out (and why)

This briefing intentionally refrains from reproducing the report’s detailed segment tables and regional splits. PW Consulting’s “trailer” approach is deliberate: we demonstrate analytical depth and executive signal-to-noise, while preserving the full, granular datasets and model inputs for subscribers. The full report includes downloadable models, primary-interview transcripts, and the segmentation detail that underpins the forecasts — essential for procurement negotiations, M&A diligence, and product roadmap decisions.

Next steps

- If you are finalizing budgets, procurement strategies, or M&A pipelines in 2026, prioritize a short briefing with PW Consulting to map our model outputs against your balance sheet and production plans.

- To access the complete dataset, supplier scorecards, and the scenario model, visit the report download page or contact PW Consulting’s aerospace practice for a tailored briefing and data license.

PW Consulting remains available to run bespoke workshops that translate this market intelligence into executable 12–36 month plans: from supplier negotiation playbooks to MRO capacity build-outs and materials‑focused R&D roadmaps.

For detailed analysis of this topic, please visit the official page:Worldwide Aircraft Windows Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com