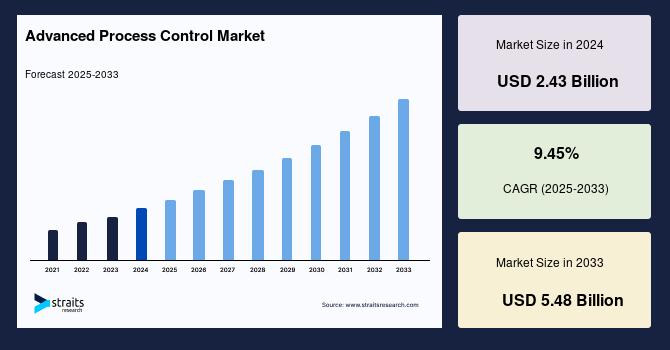

高度なプロセス制御市場は、産業の自動化と運用効率の需要によって推進され、5.48によって2033億ドルに達する

Causes |

2026-04-21 11:53:26

PW Consulting’s latest market research, "Worldwide Pharma Grade Ibrutinib Market," synthesizes five years of historical performance (2020–2025) and projects forward through 2032. The global pharma-grade ibrutinib market reached an estimated USD 954.9 Million in our 2025 base year and is modelled to grow at a compound annual growth rate (CAGR) of 3.88% across the 2026–2032 forecast window, reaching approximately USD 1,246.3 Million by 2032. For life‑science executives, investors, and procurement leaders preparing strategic plans for 2026, the report is designed as an operational playbook: it exposes the forces that will most materially influence revenue pools, pricing dynamics, and competitive positioning while preserving the granular subsegment tables and transaction-level intelligence for subscribers only.

Worldwide Pharma Grade Ibrutinib Market

2026 will be a turning point for companies exposed to the ibrutinib value chain. Our modelling captures a post‑reimbursement, post‑patent reality in key markets and quantifies the net effect on revenue trajectories, supplier economics, and clinical adoption scenarios. The combination of moderated market growth (mid-single digits) and concentrated supplier power means that strategic choices—ranging from when to expand generic offerings to how to structure long‑term API sourcing contracts—will determine winners and losers.

Worldwide Pharma Grade Ibrutinib Market

Actionable timing: With the report’s base year anchored in 2025 and forecasts starting in 2026, the analysis is directly aligned to the operational planning cycles of commercial, regulatory, and supply chain functions.

Worldwide Pharma Grade Ibrutinib Market

Scenario granularity: We translate headline CAGR and topline forecasts into three practical scenarios—conservative, base, and upside—that reflect patent lifecycles, reimbursement shocks, and rates of therapeutic substitution.

Commercial playbook: The study links market-size projections to commercial levers such as formulary access, tender dynamics, and differentiated product formulations (e.g., oral suspension vs. tablet) so executives can prioritise investments that preserve margin under price pressure.

Reimbursement shock: The U.S. Medicare negotiation outcomes built into our base case materially compress list-price economics. Specifically, the negotiated maximum fair price for a 30‑day supply of oral ibrutinib under Medicare Part D is modelled into the 2026 revenue baseline—an outcome we treat as a structural shift for U.S. payor contracting and global reference pricing strategies.

Patent and exclusivity timing: Our report overlays the public patent timeline with expected regulatory exclusivities and known secondary patent filings. While core composition patents in certain jurisdictions are nearing expiry, remaining patent barriers and linked exclusivity provisions shape the earliest feasible generic entry scenarios; these dynamics are embedded in our forecasts and scenario matrices.

Supply economics and raw material pressure: We model API transaction-price bands and their sensitivity to order quantity and destination market. Procurement leaders will find the report’s supplier-cost curves and margin-impact simulations immediately usable when negotiating three‑to‑five‑year supply agreements.

Clinical and label evolution: Recent clinical data and label updates—including fixed‑duration combination strategies presented in late 2025 and expanded oral-suspension labelling—are assessed for their likely impact on prescribing patterns and average treatment duration assumptions.

Robust market sizing and forecasting (2020–2032): historical performance, 2025 base-year calibration, and a granular forecast model that translates volume and price drivers into revenue outcomes.

Risk-adjusted scenario modelling: tailored cases that quantify upside and downside potential from patent litigation outcomes, reimbursement policy shifts, and rapid generic penetration in select geographies.

Commercial and procurement playbooks: go‑to‑market recommendations, tender response templates, and API-sourcing strategies that incorporate supplier qualification, dual-sourcing thresholds, and inventory optimisation for high-cost oncology APIs.

Regulatory timeline mapping: jurisdiction-level exclusivity calendars, anticipated filing windows for generics, and a tracker of label-change events with estimated commercial impact.

Competitive intelligence and benchmarking: CR3 and CR5 concentration metrics, capability maps for branded innovators versus generic/API manufacturers, and a comparative assessment of manufacturing footprints and regulatory approvals.

Financial sensitivity tools: downloadable models that let commercial teams stress-test pricing scenarios against reimbursement outcomes and patient‑mix changes.

The branded originators retain a dominant commercial position in multiple major markets, supported by a deep evidence base and distribution reach. Our analysis profiles the joint originators’ portfolio strategy, recent lifecycle-management activity, and clinical data readouts that could moderate treatment duration or expand specific formulation usage. Meanwhile, a diversified set of generics and API suppliers—primarily headquartered in Asia and Eastern Europe—are actively participating across manufacturing, regulatory filings, and supply agreements. The market exhibits meaningful concentration: the combined share of the top-three and top-five companies is a critical structural parameter in our modelling and informs counterparty risk assessments for procurement and alliance teams.

Incumbent innovators: Branded developers maintain leadership via clinical stewardship, formulation diversity (including oral suspensions and extended-dosing options), and active lifecycle management. Recent label expansions and late‑stage clinical data presentations are evaluated for their potential to influence prescribing preferences and average treatment duration.

Generics & API players: A broad group of established pharmaceutical manufacturers and API houses are positioned to scale generic supply and competitive pricing once regulatory windows permit. Their capabilities—ranging from GMP-compliant API production to dossier readiness for multiple markets—are mapped and scored in the report to support supplier selection and M&A screening.

Regional entrants: Local manufacturers in major emerging markets have already leveraged earlier patent expiries or local regulatory pathways to introduce authorised generics. Our report assesses the commercial spillover risk from these dynamics into global pricing benchmarks and tender outcomes.

For branded originators: Prioritise value-based contracting pilots and indication‑specific evidence generation to preserve premium placements. Accelerate programme timelines for differentiated formulations and combinations that can justify higher net prices amid tightening payor scrutiny.

For generic/API manufacturers: Lock in capacity and dual-source agreements now. Our price‑sensitivity analysis shows that early scale and validated supply credentials translate to outsized tender wins when entry windows open.

For private equity and M&A teams: Use the report’s scenario models to stress-test acquisition targets under negotiated‑price regimes. Look for targets with integrated API-to‑finished-dosage capabilities, and validated regulatory filings in high‑priority markets.

For hospital systems and large purchasers: Revisit contracting timelines and consider multi‑year frameworks that incorporate volume flexes, shared-savings mechanisms, and supplier continuity clauses to mitigate disruption when product switching accelerates.

To preserve the report’s role as an operational intelligence product, detailed subsegment tables—regional share breakdowns, application-level revenue slices, and per-strength pricing ladders—are reserved for subscribers. Those datasets are the analytical engines beneath the strategic recommendations above; they enable customisable supply‑chain simulations, formulary impact quantification, and deal valuation workstreams. This briefing surfaces the strategic thesis and the high-impact levers; the full report unlocks the transaction-level inputs and provider-level maps that commercial and procurement teams need to execute decisions in 2026.

Regulatory and clinical events through late 2025 are incorporated, including recent tentative approvals for generic formulations in major markets and late‑stage clinical trial readouts affecting treatment paradigms.

Reimbursement policy shifts, notably negotiated price sinks modelled for U.S. Medicare frameworks starting in 2026, are reflected across our price scenarios and profitability estimates.

Supply-side cost inputs—our models include observed API transaction-price ranges and export‑market differentials—are used to stress-test gross‑margin sensitivity across suppliers and finished‑dosage manufacturers.

The ibrutinib market in 2026 is not a single event but a confluence of policy, patent, clinical and supply dynamics. The topline growth profile is modest but resilient; the strategic questions for leaders are not whether the market will exist, but who will capture value within it. PW Consulting’s "Worldwide Pharma Grade Ibrutinib Market" report turns public headlines into executable choices—prioritising actions that protect margin, secure supply, and position organisations to capitalise on the windows of opportunity that will open as exclusivity landscapes shift.

For access to the full dataset, segment-level models, supplier scorecards, and the downloadable scenario tools that support 2026 planning cycles, please visit the PW Consulting report page and request the complete Worldwide Pharma Grade Ibrutinib Market report.

For detailed analysis of this topic, please visit the official page:Worldwide Pharma Grade Ibrutinib Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com