How Is Ranch Water Drinks Market Becoming a Popular Alternative in the Ready-to-Drink Beverage Industry?

Networking |

2026-06-03 12:24:26

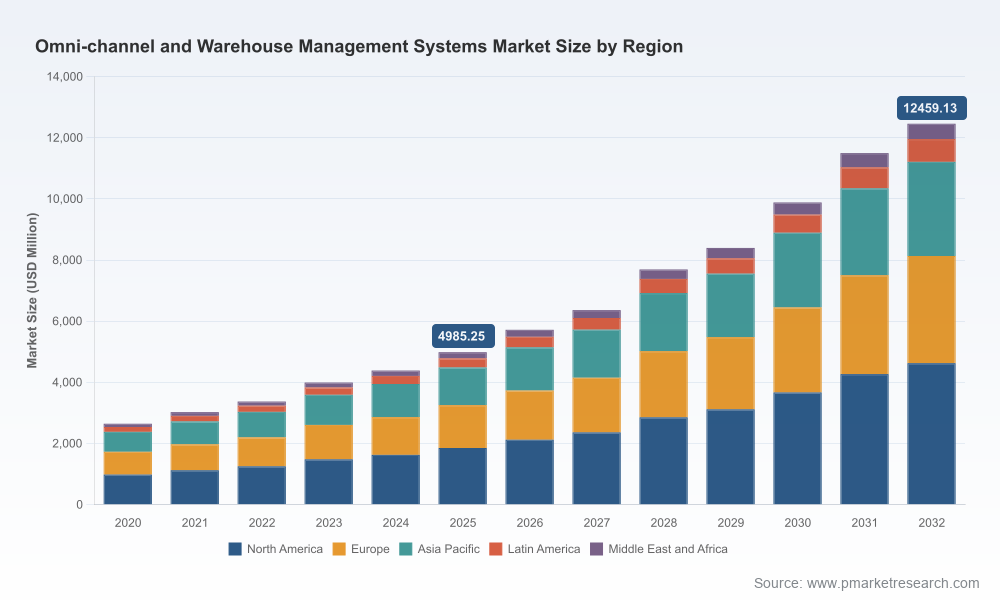

PW Consulting today releases an executive preview of our Worldwide Omni-channel and Warehouse Management Systems Market study — a strategic briefing that frames decision-making for enterprise supply chain leaders entering 2026. Drawing on five years of historical tracking and a seven-year forecast horizon, the report shows a market that accelerated through the pandemic era and is set for sustained expansion: the sector reached approximately USD 4,985 million in 2025 and is projected to grow at a 13.98% compound annual growth rate (CAGR) through to 2032, when total revenues are expected to top USD 12,459 million. For CIOs, COOs and supply chain executives, this trajectory creates both urgency and room for strategic maneuver: investment windows are opening for modernization, while vendor landscapes and technology architectures are shifting rapidly.

Worldwide Omni-channel and Warehouse Management Systems Market

Cloud momentum is maturing into mainstream deployment. Cloud-native WMS architectures have captured material market share, driven by lower upfront capital, elastic scalability and a continuous delivery model that simplifies upgrades and regulatory compliance. This is reshaping procurement timelines and the calculus for multi-year total cost of ownership.

Worldwide Omni-channel and Warehouse Management Systems Market

Execution-level orchestration is becoming a strategic differentiator. Warehouse Execution Systems (WES), advanced labor management, AI-driven orchestration and tighter TMS/WMS/OMS integration are enabling throughput improvements of a magnitude material enough to offset rising labor and logistics costs. Leading vendors and equipment partners now position real-time orchestration as part of an integrated fulfillment stack.

Worldwide Omni-channel and Warehouse Management Systems Market

Regulatory and data requirements elevate software choice beyond features. Stricter traceability mandates and data protection regimes increase demand for automated compliance, auditable trails and secure cloud architectures — particularly among pharmaceutical, food & beverage and regulated manufacturing clients.

Market structure shows selective consolidation. The competitive field remains diverse: global tier‑one suites coexist with specialized, modular vendors focused on 3PLs, mid-market distribution and niche verticals. This mix provides buyers with multiple implementation archetypes but also requires more sophisticated vendor selection frameworks.

Actionable executive summary with risk-adjusted investment scenarios for 2026 planning cycles.

Seven-year market model (2026–2032) and sensitivity analyses to test price, adoption and automation scenarios.

Vendor evaluation framework and comparative vendor scorecards that synthesize capability, deployment models, vertical strengths, implementation complexity and partnership ecosystems.

Implementation playbooks and phased migration blueprints (including “lift-and-shift,” hybrid and greenfield cloud paths) to minimize disruption and manage TCO.

ROI and TCO templates tailored to different buyer archetypes — retail/e‑commerce, manufacturing, regulated industries and 3PLs — plus sample KPIs, contract guardrails and migration checkpoints.

Automation-integration blueprints and vendor–robotics partner mapping to accelerate pilot-to-scale cycles.

Compliance and data-security checklist tailored to traceability-sensitive verticals, including audit-readiness workflows for batch and serial tracking.

Case studies showing measured throughput gains, labor productivity improvements and orchestration wins, with anonymized ROI data and lessons learned.

Tier‑one cloud-native suites: Vendors with cloud-first roadmaps and deep omni‑channel fulfillment capabilities continue to lead with broad functional footprints and strong integration into ERP and transportation ecosystems. Their strengths are predictable scalability, extensive partner networks and feature breadth — appropriate for complex, enterprise-scale transformation programs.

Orchestration and AI winners: Providers that embed AI-driven orchestration and robust WES capabilities are translating real-time decisioning into tangible throughput and uptime improvements. These capabilities are increasingly decisive in environments with mixed automation and high SKU churn.

Modular and mid-market specialists: A cohort of vendors focuses on fit-for-purpose deployments for 3PLs, regional distributors and regulated healthcare segments. Their advantage is lower implementation complexity, strong vertical templates and faster time-to-value in targeted use cases.

Platform consolidation trend: Expect tighter bundling across execution layers — WMS, WCS, WES and TMS — as vendors pursue end-to-end visibility and single-pane orchestration. Strategic acquisitions and partnerships are converging toward broader execution suites, which changes integration risk profiles for buyers.

Recent market moves underscore the pace: notable provider rebranding and portfolio consolidation, new execution software launches, and expansion plays into North American markets reflect an active vendor market balancing organic product development with inorganic capability-building. These developments influence vendor roadmaps, partner availability and negotiation levers for buyers.

Translate outcomes into requirements: Begin RFPs from measurable business outcomes (throughput, on-time fulfillment, labor productivity, compliance readiness), not feature checklists. Outcome-driven procurement shortens evaluation cycles and exposes true vendor fit.

Reassess TCO with multi-scenario models: Use scenario modeling to compare on‑premise, private cloud and cloud‑native approaches across a 5–7 year horizon. Factor in continuous improvement cadence, security and compliance uplift, and the potential benefit of subscription-based operational flexibility.

Prioritize integration-first pilots: Execute pilots that validate WMS integration with WES, TMS and automation hardware. The sequence and scope of pilots — zone-by-zone, site-by-site — materially reduce scale-up risk.

Insist on traceability and auditability: For regulated sectors, make automated traceability, batch/serial management and audit trails mandatory evaluation criteria. Ensure vendors can demonstrate rapid compliance updates.

Design for people plus automation: Technology alone won’t deliver throughput without workforce enablement. Require vendors to demonstrate labor management capabilities and change-management support as part of implementation contracts.

Monitor market consolidation and partnerships: As vendors expand into adjacent layers and pursue acquisitions, update sourcing strategies to protect flexibility. Negotiate cloud exit and data portability clauses to avoid vendor lock-in.

Elevate cybersecurity and data governance: For cloud/SaaS deployments, demand continuous risk-management evidence, role-based access, encryption standards and vendor SOC/ISO attestations as contract prerequisites.

Advisory engagements that convert the report’s market model into bespoke investment roadmaps and procurement packages.

Vendor shortlists and RFP templates calibrated to your vertical, scale and automation aspirations — including negotiation playbooks and implementation governance plans.

Workshops and executive briefings that translate market dynamics into board-ready investment briefs and risk-mitigation strategies.

The full Worldwide Omni-channel and Warehouse Management Systems Market report contains the comprehensive datasets, vendor scorecards, scenario models and implementation tools referenced in this release. In keeping with our “preview” approach, we have intentionally withheld certain granular segmentation tables and the complete vendor ranking matrix from this summary to encourage direct engagement with the full report and advisory services. For procurement teams and executive sponsors preparing 2026 budgets, that body of work provides the empirical foundation and practical templates to convert market intelligence into executable programs.

To obtain the complete report, datasets and consulting engagement options, please visit PW Consulting’s website or contact our advisory desk. The decisions you make this year about architecture, vendor selection and partner strategy will define your ability to transform omni‑channel complexity into sustained competitive advantage over the next decade.

For detailed analysis of this topic, please visit the official page:Worldwide Omni-channel and Warehouse Management Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com