Worldwide Memory Packaging Market — Strategic Outlook for 2026 Decisions

Executive summary

PW Consulting’s new market intelligence on the Worldwide Memory Packaging Market provides the evidence-based, decision-grade perspective executives need to act in 2026. The market’s overall scale reached USD 36,898.6 Million in our base year (2025) and is projected to expand materially in 2026 and beyond — our forecast sees the market trending toward roughly USD 74,380 Million by 2032 under the central scenario, reflecting a compound annual growth rate (CAGR) of 10.53% across the 2026–2032 forecast window. These headline metrics conceal an important nuance: growth is uneven along technology, geography and customer segments, and is being driven by a small number of structural inflections in supply, policy and product architecture.

Worldwide Memory Packaging Market

Why this report matters for 2026 decision-makers

- Make procurement and capacity decisions with confidence: 2026 will be a pivotal year to renegotiate supplier commitments, re-allocate CAPEX and lock-in materials contracts as memory makers shift outsourcing patterns and service providers re-price capacity.

- Prioritize capital against risk: our model translates market growth into probabilistic cash-flow impacts for OSATs, IDM packaging groups, and private equity—helping boards and CFOs choose between organic capacity expansion, brownfield upgrades, or M&A to secure market share.

- Design defensible roadmaps for advanced packaging: the rise of heterogeneous integration and high-bandwidth memory increases technical and supply-chain complexity; product, operations and R&D leaders must align roadmaps to capture value without over-investing ahead of adoption curves.

- Anticipate regulatory and geostrategic shock: export controls and tariff regimes are already shaping investment flows and will materially affect where and how advanced memory packaging capabilities are staged.

Market dynamics shaping near-term strategy

Three macro forces are converging to re-write the memory-packaging playbook in 2026:

Worldwide Memory Packaging Market

- Supply tightness and price repricing. Several OSATs and testing service providers announced price adjustments in early 2026 in response to sustained capacity tightness on DRAM and NAND packaging. This is compressing gross margins for cost-sensitive OEMs and shifting value capture toward providers who can combine scale with advanced technical capability.

- Customer outsourcing ramps and design cycles. Major memory OEMs are increasing their reliance on external packaging partners for next-generation DDR and HBM products. Outsourcing ramps create windows of demand that favor OSATs with scalable, qualifiable capacity — and create exposure for OEMs that under-allocate partner capacity.

- Policy and materials friction. New trade measures and export controls (including targeted restrictions on advanced memory and packaging-relevant technologies) plus national controls on critical minerals are tightening the set of reliable suppliers for some advanced processes. These changes raise the bar for supply-chain due diligence and may accelerate onshore or friend-shoring strategies.

Collectively, these dynamics mean that 2026 will be a year of tactical adjustments and strategic repositioning. Businesses that treat the year as merely another planning cycle risk being surprised by abrupt price regimes, capacity constraints, or regulatory compliance costs that impact both unit economics and time-to-market.

Worldwide Memory Packaging Market

Competitive landscape: implications for OEMs, OSATs and investors

The market remains concentrated: the three largest participants account for a majority share of industry revenue, and the top five cover more than two-thirds of the market — a concentration profile that accelerates both competitive escalation and consolidation opportunities. That structure creates distinct implications:

- For tier-1 OEMs: supplier leverage is evolving. Firms with strong internal packaging capabilities can choose to insource selectively, while those dependent on OSATs must secure multi-year commitments or premium service-level agreements to guarantee throughput.

- For OSATs and service providers: scale plus technical breadth is the primary defense against margin compression. Service providers that combine legacy wire-bonding and flip-chip throughput with fast qualification paths for TSV/3D and fan-out processes will capture disproportionate value.

- For strategic investors: a concentrated market lowers the number of attractive buy targets but increases the value of well-timed bolt-on acquisitions and capacity partnerships that close capability gaps.

Key players profiled (selection)

- Advanced Semiconductor Engineering Inc. (ASE Inc.) — Kaohsiung, Taiwan. Leading OSAT with comprehensive memory packaging offerings across DRAM, NAND and advanced formats including high-bandwidth memory and system-in-package approaches. (https://www.aseglobal.com/)

- Amkor Technology Inc. — Tempe, Arizona, United States. Major global provider of packaging and test services, experienced across memory and storage packaging, including advanced fan-out and specialized memory formats. (https://amkor.com/)

- Powertech Technology Inc. (PTI) — Hsinchu, Taiwan. Specializes in memory packaging and testing with sizeable capacity serving primary memory manufacturers. (https://www.pti.com.tw/)

- ChipMOS Technologies Inc. — Hsinchu, Taiwan. Focused on integrated packaging and test services for DRAM and NAND flash applications. (https://www.chipmos.com/)

- Hana Micron Inc. — Gumi, South Korea. Provides advanced memory packaging techniques for semiconductor memory devices. (https://www.hanamicron.co.kr/)

- JCET — Jiangyin, China. Large OSAT operator offering a range of packaging solutions for memory devices. (https://www.jcetglobal.com/)

- Additional regional players and specialists — prominent suppliers in Taiwan, China, South Korea and Southeast Asia round out the competitive set, each presenting different trade-offs in cost, lead-time and regulatory exposure.

Recent developments that change the playbook

- Applied Materials announced a long-term R&D partnership with SK hynix focused on advanced materials and packaging innovations for next-gen DRAM and HBM — a vivid signal that equipment and materials upgrades will be central to the next performance leap.

- Several OSATs announced price increases in early 2026 to offset tight capacity and upstream cost pressures; such moves change short‑term negotiation levers and increase the value of secured capacity commitments.

- Major memory OEMs are accelerating outsourcing of DDR5 and adjacent product lines to external packagers, creating a multi-year demand pulse that will test qualification throughput and supply resilience.

- Policy interventions including tariffs and export controls are narrowing the set of viable locations and technologies for advanced packaging in certain jurisdictions — a crystallizing risk that must be managed inside strategic planning and procurement.

What our report delivers — practical, actionable content

PW Consulting’s Worldwide Memory Packaging Market report is deliberately designed as a playbook for executives making 2026 allocations. The report combines rigorous market modeling with pragmatic implementation tools, including:

- Top-down and bottom-up market-sizing and demand scenarios (2020–2025 historicals; 2026–2032 forecasts).

- Concentration and competitive mapping with capability matrices for the leading OSATs and regional specialists.

- Supply-side capacity maps, qualification timelines and bottleneck stress-tests to expose single points of failure.

- Price and cost-model templates that show margin sensitivity across packaging technologies and materials cost shocks.

- Regulatory risk matrix and geostrategic playbook to support friend-shoring, dual-sourcing and licensing strategies.

- Procurement and contract negotiation checklists, plus an M&A & partnership scoreboard that scores targets by strategic fit.

- Implementation roadmaps for adopting advanced packaging technologies (e.g., 3D stacking, TSV, fan-out, WLCSP) aligned to realistic qualification and ROI timeframes.

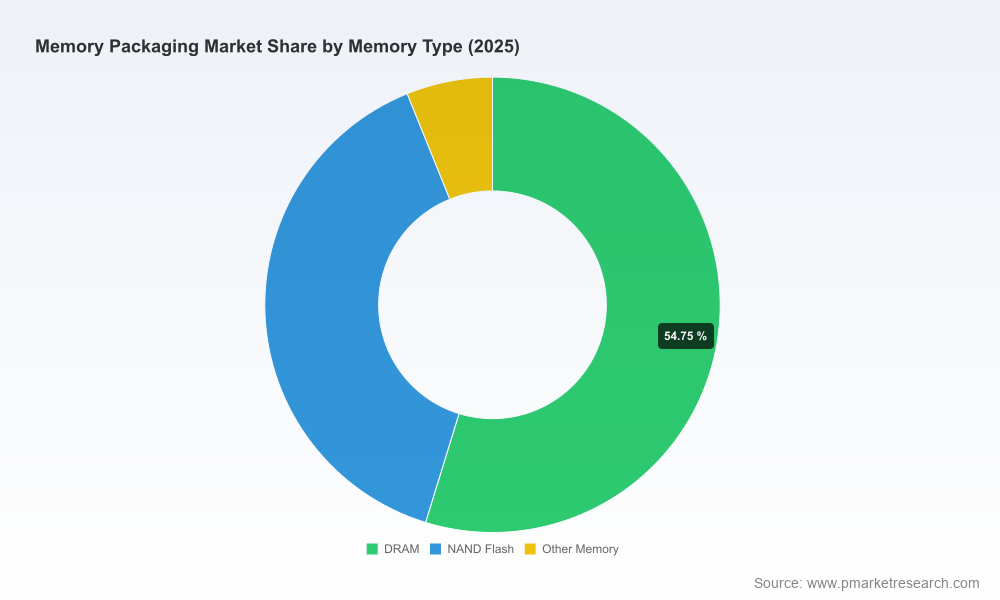

Note: this press summary intentionally omits the granular split tables and drill-down datasets (region-by-technology-by-memory type), which are available exclusively in the full report and online data portal.

Recommended 2026 actions — six pragmatic moves

- Revisit supplier contracts now. Convert discretionary single-year relationships into multi-year, capacity-secured partnerships with indexed pricing to hedge volatility.

- Lock critical materials and logistics pathways. Negotiate conditional supply agreements for constrained inputs and layer contingency logistics into manufacturing plans.

- Scoped CAPEX: prefer optionality. Where possible, favor modular capacity expansions and partner-funded brownfield upgrades over large greenfield commitments.

- Accelerate qualification pipelines for advanced packaging with prioritized customer/product lanes to capture early-adopter premiums while limiting broad exposure.

- Embed regulatory scenario workstreams into corporate planning. Model the P&L and time-to-market implications of tariff or export-control escalations on target products and facilities.

- Use strategic partnerships to access capability. Consider joint R&D or co-investments with equipment and materials suppliers to de‑risk process transitions and share qualification costs.

How PW Consulting supports 2026 decision cycles

Our consulting teams combine the detailed market model with implementation support: from supplier diligence and integration planning to price-model customization and deal negotiation support. The market is large and growing, but value capture will be won by organizations that translate top-line opportunity into defensible and executable operational plans.

To access the full datasets, scenario outputs, and operational toolkits that underpin these findings, consult the complete Worldwide Memory Packaging Market report and the PW Consulting research portal. The full report contains the granular regional, technology and memory-type splits that inform the tactical playbooks summarized here — critical inputs for any organization committing capital or re-shaping supply chains in 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Memory Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com