Saddle Chairs Market 2026 Strategic Outlook — PW Consulting Executive Brief

As organizations recalibrate workplace ergonomics, clinical environments, and industrial workstations coming out of the pandemic-era transition to hybrid operations, saddle chairs are re-emerging as a category with tangible strategic and procurement implications. PW Consulting’s latest Saddle Chairs Market study — grounded in five years of historical data and a seven-year forecast horizon — quantifies that momentum and translates it into decision-grade findings for 2026 planning cycles.

Saddle Chairs Market

Why this brief matters for 2026 decisions

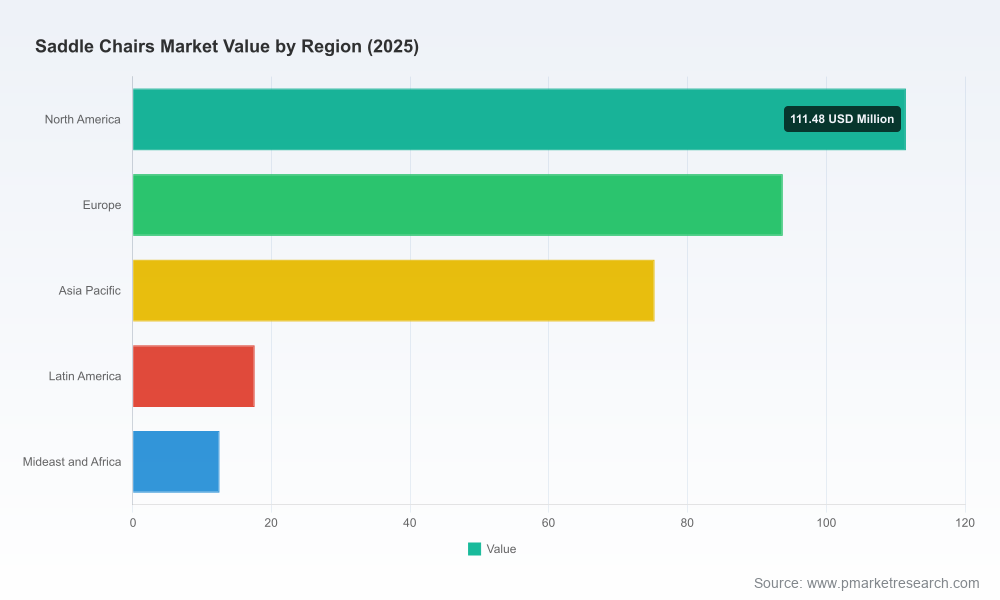

Our market model values the global saddle chairs market at USD 310.5 Million in the 2025 base year and projects steady expansion through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 5.85%. That trajectory reflects a confluence of factors relevant to executive teams and category managers: the normalization of active-sitting products alongside standing desks, healthcare-driven demand for posture-support solutions, and new product introductions from both specialist and mainstream office-furniture manufacturers.

Saddle Chairs Market

For 2026 planning, the implications are practical: procurement teams must balance the upside of growing adoption against episodic supply-chain constraints; product and R&D leaders can prioritize modular, certification-led designs; and M&A and corporate development functions should use the industry’s current fragmentation profile to identify bolt-on opportunities that accelerate access to clinical and industrial end-markets.

Saddle Chairs Market

What PW Consulting’s full report delivers

- Actionable market sizing and scenarios. Beyond a base-case forecast, the report constructs upside and downside scenarios that stress-test demand assumptions against raw-material shocks and accelerated hybrid-work adoption. Each scenario is associated with recommended inventory, sourcing, and pricing levers for 12–24 month execution.

- Practical go-to-market playbooks. For incumbent manufacturers and newcomers, we provide segment-specific GTM strategies (healthcare, commercial office, industrial/technical), channel maps, buyer-persona playbooks, and sample commercial scorecards for vendor selection.

- Product and innovation roadmaps. The report synthesizes ergonomic research, patent filings, and clinical endorsements to outline a prioritized product roadmap—spanning saddle variants, backrest integration, split-seat ergonomics, and sustainable material substitutions—that maximizes adoption while containing warranty and liability exposure.

- Supply chain and procurement playbook. We map critical inputs (cushion foams, gas lifts, metal frames, upholstery), identify single-source risk exposures, and offer mitigation strategies—including dual-sourcing templates, inventory buffers, and nearshoring analyses—tailored for 2026 realities.

- Competition and M&A intelligence. The study profiles key players, their business models, manufacturing footprints, and strategic differentiators, and identifies criteria for attractive acquisition targets and partnership opportunities.

- Regulatory and risk matrix. The report consolidates applicable furniture safety standards, certification pathways relevant to medical and dental settings, and a compliance checklist to reduce time-to-market and procurement friction for institutional buyers.

Competitive landscape: strategic takeaways

The saddle chairs market exhibits a moderate level of concentration. Our concentration analysis indicates that the top three suppliers together account for roughly 28.5% of observable market activity, and the top five approach the high‑thirties in percentage share. This profile creates space for niche specialists to defend premium positions while larger furniture groups leverage brand and distribution scale to accelerate adoption.

- Salli Systems (Finland) — A product-led specialist famed for split-seat solutions. Their technical differentiation around two-part seats positions them well in health-sensitive segments where posture and circulation claims carry purchase-weight. Strategic implication: incumbents should monitor Salli for feature-led innovations that can be licensed or challenged through competing ergonomics science.

- Score BV (Netherlands) — A vertically integrated designer-manufacturer that emphasizes workplace and clinical deployments from its own factory. Score’s ability to control production enables faster customization for institutional buyers; their recent content efforts also show how thought leadership supports consultation-led sales.

- HÅG / Flokk (Norway) — With the Capisco lineage and design heritage, they occupy an innovation-and-brand-led tier that targets dynamic sitting and sit-stand integration. Their strategic advantage is design credibility within forward-looking corporate procurement.

- Humanscale (USA) — A prominent ergonomic furniture brand that brings established enterprise channels and trust to saddle variants. Their model suggests that once saddle chairs reach mainstream office-furniture buying lists, major ergonomic brands will be natural amplifiers.

- Bambach Saddle Seat (Australia) — The originator archetype with strong recognition in dental and clinical markets; their backrest options and clinical pedigree make them a strong partner for professional-training and certification programs.

- Treston (Finland) — Focused on industrial use-cases and ESD-protected environments, Treston demonstrates how industrial specifications (durability, anti-static properties) create differentiated, higher-margin product lines.

- Branch Furniture (USA), ProNorth Medical (Canada), RGP Dental (USA) — These brands illustrate three strategic paths: sustainable design and scaling via partnerships (Branch), focused healthcare product innovation and targeted launches (ProNorth), and clinical specialization in dental ergonomics (RGP). Their activity underscores the fragmented, opportunity-rich nature of the market.

Recent industry signals to watch in 2026

- Product momentum. Targeted product launches and content updates from specialist manufacturers continue to validate category use-cases in clinical and hybrid workplaces. These moves accelerate buyer education and short-term demand.

- Raw-material pressure. Polyurethane foam supply constraints identified in early 2026 are elevating costs and lead times for cushion-intensive seating products. Manufacturers that secure alternative foam sources, re-engineer cushion constructions, or qualify validated substitutes will preserve margin and fill rates.

- Regulatory and standards stability. While ergonomic seating falls under general furniture safety frameworks, we see no category-specific recall trends in 2025–2026. This creates an opportunity for proactive certification and clinical validation as a differentiator rather than as a compliance burden.

- End-user behavior. The sustained interest in active-sitting solutions—driven by hybrid work practices and sit-stand desk pairings—means that commercial procurement cycles will increasingly include saddle chairs as an option rather than a niche add-on.

Strategic recommendations for 2026

- Procurement and supply-chain: Implement near-term dual-sourcing for critical cushioning components, prioritize suppliers with verified capacity, and establish conditional inventory buffers tied to lead-time triggers. Negotiate fixed-price collars where possible to protect against foam price volatility.

- Product and R&D: Prioritize modularity (interchangeable seats, backrest add-ons), validate ergonomic claims through independent clinical trials, and accelerate low-VOC and recyclable-material options to meet corporate ESG requirements.

- Commercial and marketing: Build educational content and point-of-decision tools aimed at procurement committees and occupational-health buyers. Position saddle chairs not only as comfort items but as productivity and injury-prevention levers, supported by quantified case studies.

- M&A and partnerships: Target bolt-on acquisitions that provide clinical-channel access or proprietary seating technologies. Consider partnership models (co-branded products, OEM agreements) to rapidly enter adjacent geographies while minimizing capex.

- Risk management: Model downside scenarios tied to prolonged material shortages and include contractual flex for service-level adjustments. For larger suppliers, diversify manufacturing footprints to reduce concentration risk.

Scenarios that should inform your FY26 budget

Use the report’s scenario work to align capital allocation with supply-and-demand uncertainty. Our base case aligns with the market’s projected mid-single-digit CAGR. The upside case assumes accelerated hybrid adoption and substitution away from conventional stools, while the downside incorporates prolonged polyurethane constraints and slower corporate capex. For each scenario, we provide recommended inventory days, pricing adjustments, and commercial cadence to protect revenue and margin integrity.

How to use this intelligence

PW Consulting’s Saddle Chairs Market report is designed for functional leaders who need to convert market signals into operational actions: procurement directors looking to secure supply through 2026; product teams evaluating feature roadmaps; BD and corporate development teams sizing acquisition targets; and sales leaders constructing evidence-based value propositions for institutional buyers.

The executive brief you are reading intentionally surfaces strategic insights and actionable guidance while preserving the full granularity of segment splits, regional allocations, and vendor-level figures for clients who require them. Those detailed datasets — including supplier share matrices, end-market segmentation, and validated price benchmarks — are available in the full report and accompanying data workbook.

Next steps

- For procurement or product inquiries, commission the full PW Consulting Saddle Chairs Market report to access the segmented data, supplier scorecards, and scenario-specific playbooks that will directly inform your 2026 operating plan.

- If you are evaluating acquisition or partnership opportunities, request the confidential target shortlist and valuation framework derived from our competitive and consolidation analyses.

- To fast-track risk mitigation, ask for the supply-chain remediation annex that maps alternative foam suppliers and validated material substitutions with onboarding templates.

PW Consulting stands ready to brief executive teams and steering committees on these findings and to translate them into prioritized 90/180/360 day action plans. For access to the complete dataset, detailed segmentation, and proprietary supplier metrics referenced in this brief, visit PW Consulting’s market intelligence portal or contact our industry practice leads to arrange a tailored executive session.

For detailed analysis of this topic, please visit the official page:Saddle Chairs Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com