PW Consulting: Moissanite Market Set to Grow at a 6.98% CAGR — Strong Outlook Through 2032

Other |

2026-06-30 16:38:03

PW Consulting’s Worldwide Smartphone Panel Market report (base year 2025; historical series 2020–2025; forecast 2026–2032) delivers a pragmatic, decision-ready view for executives setting technology, supply-chain and investment agendas in 2026. The market is on a steady growth trajectory — our top-line model shows the global smartphone panel market at approximately USD 45.5 billion in 2025 and growing at a compound annual growth rate (CAGR) of 5.19% through the 2026–2032 forecast window, reaching roughly USD 65 billion by 2032. Behind that headline growth lie concentrated supplier dynamics, accelerating technology transitions, and a set of geopolitical and raw-material risks that together will shape winners and losers next year and beyond.

Worldwide Smartphone Panel Market

Actionability under time pressure: 2026 is a hinge year for many OEMs, ODMs, and panel suppliers as multi-year capacity plans and technology investments converge. Companies that align procurement, R&D and go-to-market choices to realistic demand and supplier-risk scenarios in the first half of 2026 will secure outsized advantage.

Worldwide Smartphone Panel Market

Clarity on industry structure: The smartphone panel market remains highly concentrated — a small cohort of large suppliers controls the lion’s share of premium and high-volume programs. That concentration creates both negotiating leverage for OEMs and single-point-of-failure risk when paired with raw-material bottlenecks and trade frictions.

Worldwide Smartphone Panel Market

Technology and form-factor inflection points: Flexible/foldable architectures and AMOLED migration in mid-range devices are changing BOM structure, supplier selection, and lifetime service models. Our report provides the roadmap executives need to sequence capability investments and partner selections.

Moderate, durable top-line growth. With market value expanding at a ~5.2% CAGR across our forecast, firms should plan for steady demand growth rather than explosive adoption. That favors disciplined capacity additions and staged capital deployment over indiscriminate capex pours.

AMOLED transition accelerates. Unit-mix shifts toward emissive technologies are reducing the relative share of legacy LCD platforms in mid-range devices. For component buyers, this means negotiating increasingly sophisticated quality and yield guarantees with AMOLED-capable suppliers, and preparing for new inspection and failure-mode profiles in production and after-sales service.

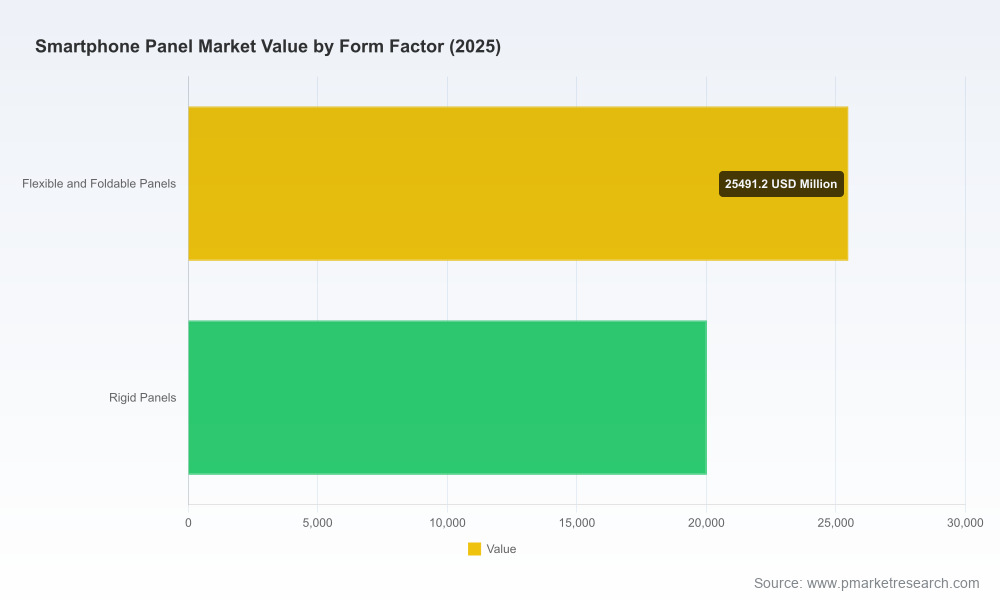

Flexible and foldable panels are strategic growth vectors. Demand for panels that enable new industrial designs is rising, but these products carry distinct material and process dependencies (e.g., polyimide substrates, ultra-thin glass) that raise cost and supply risk. Early alignment with qualified suppliers and co-development agreements will compress time-to-market for first movers.

Supply-chain and materials concentration. Critical inputs used across display manufacture — including indium-containing compounds, specialty substrates and advanced chemical precursors — remain concentrated geographically. Policymakers and market participants are actively considering import restrictions and incentives, which can rapidly shift sourcing economics and lead times.

Regulatory and trade uncertainty. Investigations and policy actions aimed at processed critical minerals have the potential to introduce tariffs, quotas or preferential procurement rules. Firms should model scenarios that incorporate supply frictions and response options such as forward-buying, qualifying alternate chemistries, or vertical integration of strategic upstream processes.

The competitive picture is defined by a handful of companies that combine scale, advanced process know-how, and close OEM relationships. PW Consulting’s analysis of market behavior, recent investments and public disclosures highlights several actionable takeaways:

Samsung Display: Continues to lead in premium flexible AMOLED and LTPO-enabled panels. Recent capacity reviews and technology demonstrations signal readiness to expand foldable OLED output and to push advanced features (privacy, slidable designs) into mainstream flagships. Strategy implication: Samsung is a preferred partner for high-margin flagship programs; secure multi-year supply agreements if your product roadmap requires the latest foldable or LTPO capabilities.

BOE and Chinese suppliers: Volume leadership is now a structural reality. Investment in larger Gen lines and the activation of additional OLED capacity have sharpened their competitiveness for mid-to-high-end programs. Strategy implication: Chinese suppliers are strong alternatives for scale and cost, but evaluation must include geopolitically driven contingency planning and rigorous IP and quality assessments.

LG Display, CSOT (TCL), Tianma, Visionox, AUO, Innolux and legacy Japanese/Taiwanese players: Each brings differentiated strengths — from premium OLED process expertise to competitive LTPS/LCD offerings and niche specialty panels. Strategy implication: Consider multi-sourcing strategies that pair suppliers by capability (e.g., premium OLED from one partner, cost-optimized LTPS from another) to balance risk and performance.

Smaller entrants and regional players: Offer targeted value in emerging form factors and are often more willing to engage in co-development arrangements for novel applications. Strategy implication: Use selective pilot programs and design-for-manufacturability (DFM) engagements to capture innovation at lower cost.

Capacity moves and technology showcases: Public disclosures and trade-show demonstrations (e.g., foldable OLED capacity reviews, new product launches featuring advanced subpixel architectures, and tech showcases emphasizing privacy and slidable displays) highlight where suppliers are prioritizing R&D and capex.

Industry shipment forecasts and unit-mix shifts: Independent shipment projections show continued large-scale smartphone unit volumes with meaningful uplift in emissive panel share. For buyers, this amplifies the need for readiness on AMOLED manufacturing parameters and supplier yield support.

Material and policy developments: Concentration in processing of indium and other minerals, plus active trade investigations in late 2025/early 2026, should be modeled as credible risks in any procurement or investment plan.

Our report is designed for executives who must convert market intelligence into executable plans. It includes:

A validated historical baseline (2020–2025) and a transparent forecasting methodology for 2026–2032, enabling scenario-based planning across near-, mid- and long-term horizons.

Supplier risk matrices that score manufacturing scale, technology competency, quality/performance, geopolitical exposure, and cost competitiveness. These matrices are built to be operationalized in procurement RFPs and strategic sourcing playbooks.

Technology roadmaps and capex cadence guidance for AMOLED, LTPS and flexible/foldable panels, including implications for yield ramp timing, BOM cost evolution, and serviceability constraints.

Practical procurement templates: negotiation checklists, warranty/yield clause samples, and contingency sourcing frameworks designed for OEMs and large ODMs.

Scenario playbooks for raw-material shocks, trade-policy changes and supplier outage events — each with recommended trigger points, hedging instruments, and execution steps.

Strategic M&A and partnership maps to help corporate development teams identify value-accretive targets and co-investment opportunities without disclosing program-level economics in this summary.

Immediate (0–90 days): Conduct a supplier exposure audit focused on critical inputs and single-source dependencies; negotiate conditional capacity options with preferred OLED partners; and initiate material alternative assessments for indium-containing layers.

Medium-term (90–180 days): Run pilot co-development projects with at least one flexible-panel supplier and one cost-optimized supplier to validate BOM and yield assumptions; finalize multi-sourcing contracts with tiered supply commitments and performance SLAs.

Strategic (180–365 days): Align R&D roadmaps with chosen suppliers for foldable/flexible designs; update product roadmaps reflecting realistic ramp timelines; and position procurement to take advantage of potential policy-driven supplier re-shoring incentives or financing programs.

High-performing teams will not only consume our forecast numbers, they will operationalize the report’s playbooks into procurement scorecards, R&D milestone-linked contracts, and scenario drills. The report is designed as the single source of truth for cross-functional planning — enabling product, procurement, manufacturing and corporate development teams to coordinate around a common set of assumptions and trigger points.

This brief synthesizes the macro view and strategic implications from PW Consulting’s Worldwide Smartphone Panel Market report while deliberately withholding program-level and subsegment granularities that are core to supplier negotiations and competitive differentiation. For executives who must act in 2026 — and who require the detailed segmentation, supplier scorecards, and customizable scenario models — the full report and supporting data tables are available through PW Consulting’s report portal.

Contact PW Consulting to schedule a briefing and receive the bespoke annexes needed to transform these insights into executable contracts, investment approvals and product roadmaps for 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Smartphone Panel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com