Web Content Management Market Opens New Opportunities for Enterprises

Other |

2026-06-01 08:33:23

PW Consulting’s new market brief provides a forward-looking, pragmatic lens on the worldwide SentryGlas (SGP) and ionoplast interlayer films market as industry stakeholders prepare for strategic choices in 2026. Built from a verified historical series (2020–2025) and a detailed forecast horizon (2026–2032), the analysis synthesizes demand drivers, supply‑chain risk, regulatory inflection points and supplier positioning into immediately actionable guidance for manufacturers, glass processors, developers, and investors.

Worldwide SGP Interlayer Films Market

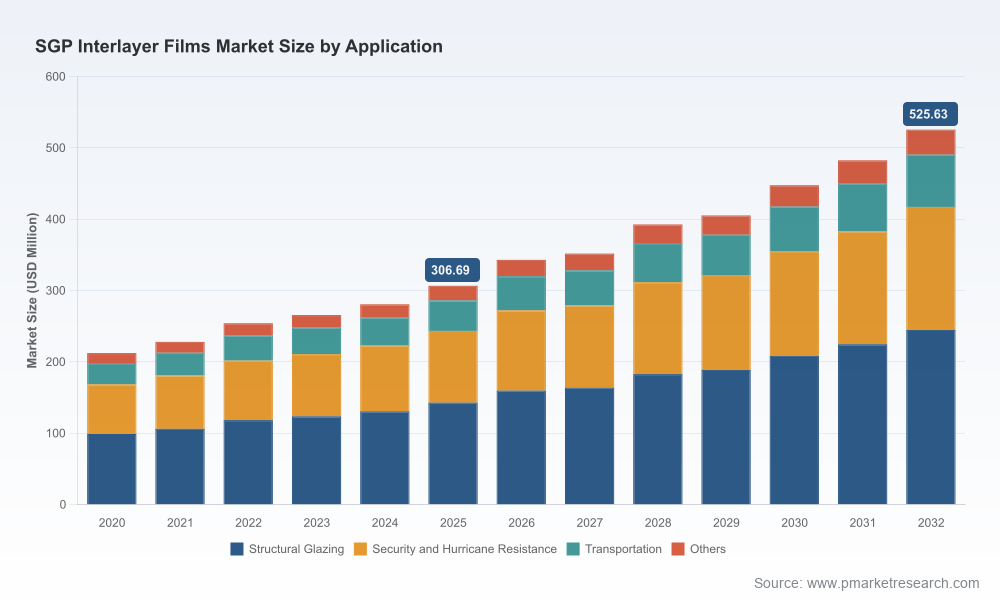

Key macro view: the SGP interlayer films market has expanded materially from an assessed USD 212.45 Million in 2020 to USD 306.69 Million in 2025, and our baseline projection places the market at approximately USD 343.05 Million in 2026. Over the forecast window (2026–2032) the market is expected to grow at a compound annual growth rate of about 8.0%, reaching an estimated USD 525.63 Million by 2032 under the base scenario. These topline dynamics set the context for capital allocation, capacity planning and contract negotiations in the coming 12–18 months.

Worldwide SGP Interlayer Films Market

Demand composition is shifting. Growth is being underpinned by structural glazing adoption in high‑value architecture, increased safety and hurricane‑resistance specifications, and expanding uptake in specialized transportation and marine segments. These applications raise requirements for thicker, higher‑performance ionoplast offerings and push premiumization across the value chain.

Worldwide SGP Interlayer Films Market

Supply tightness and cost pressure are real. Feedstock volatility — notably a documented rise in spot prices for PVB and ionomer feedstocks as a result of monomer shortages — is compressing margins for converters and shifting the balance of power toward vertically integrated suppliers or players with secured feedstock contracts.

Regulatory and trade signals are converging. New testing and certification requirements for load‑bearing and overhead glazing, together with regionally asymmetric trade measures and environmental restrictions on certain additives, increase the operating complexity for cross‑border supply and for processors serving multinational projects.

Robust market sizing and forward curves: annualized historical reconciliations and scenario‑based forecasts (base, downside, upside) across the 2026–2032 window to inform CapEx and procurement timing.

Commercial playbooks: price pass‑through strategies, contract templates to secure multi‑year volumes, and margin protection mechanisms tailored for both suppliers and large fabricators.

Supply‑chain stress testing: raw‑material cost‑shock scenarios, lead‑time sensitivity matrices, and recommended inventory policies calibrated to project pipelines and regional regulatory requirements.

Regulatory compliance roadmaps: an operational checklist for CE marking, overhead glazing approvals and post‑breakage vision testing, plus an impact assessment of chemical restrictions under regional environmental regimes.

Competitive intelligence and M&A scouting: supplier scorecards, capacity maps and a prioritized list of potential acquisition or JV targets for rapid scale and capability infill.

Commercial benchmarking: product tiering, realized pricing bands and premium feature assessments (e.g., ultra‑thick SGP, colored interlayers, pre‑laminated panel offerings).

Trosifol (Wiesbaden, Germany): A visible technology leader with a strong brand in high‑strength ionoplast films. Recent product introductions signal a move to broaden addressable aesthetic and decorative use cases without diluting structural credentials. For buyers, Trosifol’s position suggests limited short‑term negotiating leverage due to product differentiation; for competitors, the path is clear — compete on either cost through scale or on value through specialized services (pre‑lamination, design partnerships).

Kuraray (Tokyo, Japan): Developer of ultra‑thick SGP options and active in certifying products for higher‑risk applications. Certification progress for overhead and seismic applications reduces project approval friction for glazed structures — an advantage for fast movers on specification and a call‑to‑action for fabricators to update compliance dossiers to capture these higher‑margin projects.

Everlam (Halen, Belgium): Focused on flexible production and custom thicknesses for European structural projects; recent capacity increases demonstrate demand concentration in engineered structural glazing. Companies evaluating supplier relationships should map lead times and custom lamination capacity against backlog to avoid project delays.

Glastrotech (Dallas, TX, USA): An example of a high‑value regional distributor/processor model that converts global SGP offerings into application‑ready panels. Regional processors with pre‑lamination capabilities can capture downstream value and de‑risk large project delivery for architects and façade contractors.

Raw materials: Spot PVB/ionomer pricing experienced a notable uptick in late 2024 driven by ethylene monomer shortages. This dynamic constrains converters that lack forward purchase agreements and elevates the importance of sourcing flexibility and alternative resin qualification programs.

Regulation: European construction product standards — including requirements for CE marking and post‑breakage vision testing for load‑bearing glass — are changing procurement and design checklists. Projects that fail to anticipate these requirements face schedule and cost friction when entering European markets.

Trade measures: Current trade duties on certain imports alter the calculus for global sourcing and nearshoring. Where duty differentials exist, localized lamination or distribution hubs become economically attractive despite higher fixed costs.

Environmental constraints: Restrictions on some plasticizers under regional chemical regulations favor SGP ionoplast chemistries as non‑PVC, lower‑additive alternatives — a compliance tailwind that also supports premium pricing in sustainability‑focused projects.

Lock and layer feedstock contracts: combine short‑term spot exposure with staggered forward contracts to smooth cost volatility and retain flexibility for upside demand.

Prioritize certification readiness: secure required testing and documentation (e.g., overhead glazing approvals) now to be preferred suppliers on large public and institutional bids that will be tendered in 2026–2028.

Evaluate near‑market capacity: conduct a quick win analysis (3–9 months) for establishing regional pre‑lamination hubs to avoid duty and lead‑time penalties on high‑value projects.

Pursue product premiumization and differentiation: invest in colored and specialty SGP variants and integrated façade services to capture a higher share of project value and insulate margins from raw‑material swings.

Use consolidation selectively: for strategic acquirers, targeted M&A to secure custom lamination capacity, downstream distribution or proprietary chemistry opens defensible routes to scale and margin protection.

Our Worldwide SGP Interlayer Films Market report functions as an executive playbook. It combines market economics with operational tools — heat maps, supplier scorecards, capex decision templates and contract language examples — to convert insight into executable steps suitable for procurement, product, and corporate development teams.

Note: this release is a strategic preview designed to showcase the report’s analytical depth and operational utility. To preserve the commercial value of our primary intelligence and to support bespoke client engagements, we intentionally limit disclosure of core segmentation tables, regional/application splits and supplier share data in this notice. The full report includes downloadable datasets, detailed regional and application breakdowns, pricing curves, and customizable scenario models essential for transaction due diligence, plant planning and bid strategy.

For C‑suite teams planning capital investments or major sourcing changes in 2026, the benefits of the full intelligence package are immediate: accelerate time‑to‑decision, reduce execution risk and capture first‑mover economic advantage in a market expanding at roughly an 8.0% CAGR.

Contact PW Consulting to access the complete Worldwide SGP Interlayer Films Market report and the associated decision‑support toolkit. Our advisory teams can also deliver rapid, project‑specific briefings and model customizations to align the report’s outputs with your 2026 operating plan.

For detailed analysis of this topic, please visit the official page:Worldwide SGP Interlayer Films Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com