عملية رفع الثدي في الرياض مع خطط علاج مخصصة

Health |

2026-07-01 04:43:16

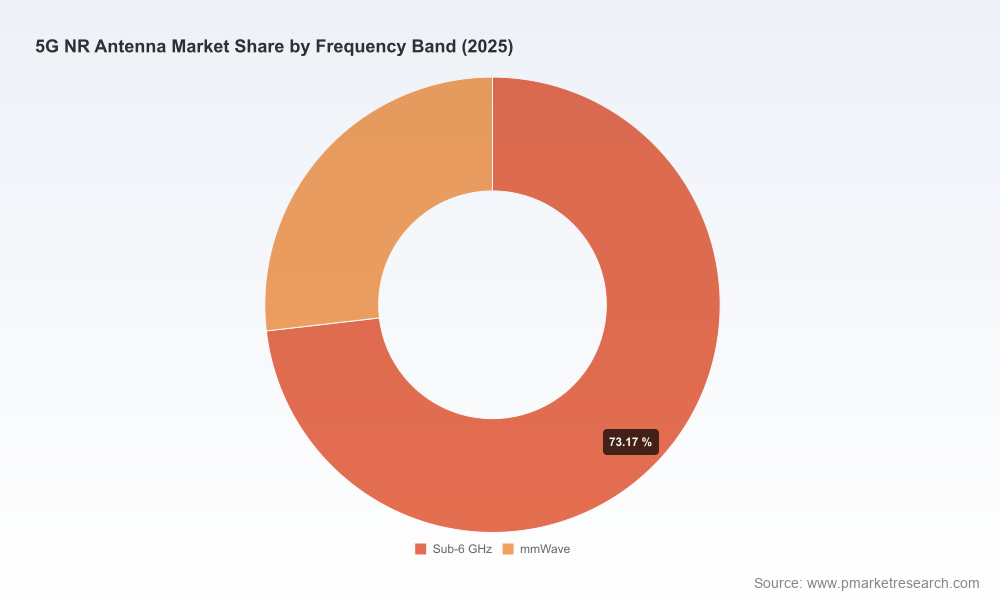

PW Consulting’s new market study on the Worldwide 5G NR Antenna Market offers a strategic compass for operators, vendors, investors and infrastructure planners as they set priorities for 2026. The market is at an inflection point: after accelerating from a modest base in 2020, total revenues reached USD 28,900 Million in 2025 and are forecast to grow to roughly USD 33,110 Million in 2026, continuing at a compound annual growth rate (CAGR) of 15.68% through our 2026–2032 projection horizon. By 2032 the market is expected to exceed USD 80 billion. These headline figures frame a high-growth opportunity, but the most valuable insights for executives are tactical — where to place bets, how to structure supply chains, and how to de-risk rollout pathways when spectrum, regulation and component costs are in flux.

Worldwide 5G NR Antenna Market

Timing capital allocation: With mid-cycle capex cycles returning in many markets, our modeling shows that incremental investment in antenna systems (both active and passive) can materially affect total cost of ownership (TCO) for macro and densification strategies. The market growth trajectory underscores that delaying strategic procurement can create competitive disadvantages in coverage, capacity and energy efficiency.

Worldwide 5G NR Antenna Market

Vendor selection and competitive positioning: The antenna market displays moderate concentration — the largest manufacturers control a meaningful portion of supply. Market consolidation trends and CR metrics signal that vendor partnership choices will determine access to design roadmaps, turnkey integration and economies of scale.

Worldwide 5G NR Antenna Market

Regulatory and spectrum risk: 3GPP’s Release 19 OTA spatial emission limits in the upper 6 GHz band, combined with national spectrum actions, are reshaping product requirements and test regimes. Decisions made in 2026 must reflect new compliance baselines to avoid retrofit costs and deployment delays.

Market sizing and scenario forecasts — Our base-year 2025 calibration and forecast scenarios to 2032 use bottom-up deployment drivers and vendor shipment models. We present a central scenario (15.68% CAGR) and alternative downside/upside pathways to stress-test procurement timing and inventory plans.

Vendor benchmarking — Proprietary scorecards evaluate commercial antenna offerings on throughput, spectral flexibility, energy efficiency, form factor compatibility and OTA emission compliance. The analysis highlights where product roadmaps align with evolving regulatory and operator requirements.

TCO and deployment playbooks — We provide build-versus-buy decision tools for macro cell upgrades and small cell rollouts, incorporating capital spend, installation labor, backhaul/fronthaul economics and lifecycle maintenance. These playbooks quantify trade-offs for hybrid AAU versus passive configurations under realistic deployment scenarios.

Risk matrices — Supply chain fragility (notably fiber and high-density components), regulatory timelines and component price volatility are quantified and paired with mitigation strategies, from dual-sourcing to inventory hedging and modular upgrade paths.

Test and compliance pathways — Given recent standards updates, the report includes practical test plans and acceptance criteria for OTA spatial emission limits and NTN conformance cases, helping engineering teams reduce verification cycles and certification costs.

Executive playbook — A concise, prioritized action list for CxOs and procurement leads, aligning vendor engagements, spectrum advocacy, capex phasing and field trials for 2026.

The competitive map blends global RAN equipment giants with specialized antenna manufacturers and systems integrators. While the market is competitive, the top tier of suppliers captures a disproportionate share of revenue and technology leadership. Our analysis profiles firms across capability vectors — massive MIMO and hybrid active-passive systems, distributed antenna systems (DAS), and passive panel solutions — and evaluates strategic fit for different deployment archetypes.

Ericsson (Stockholm, Sweden) — Strong in integrated massive MIMO and hybrid active-passive base station antennas. Ericsson’s portfolio emphasizes beamforming and high-capacity macro sites, and the company’s integration expertise (including strategic technology acquisitions) positions it well for large-scale operator projects that demand turnkey performance.

Nokia (Espoo, Finland) — Focused on scalable adaptive mMIMO (AirScale) and hybrid solutions that balance passive and active elements. Nokia’s strengths lie in modular radio access designs that suit phased upgrades and mixed macro/small-cell rollouts.

Huawei (Shenzhen, China) — Offers ultra-wideband active antenna units and multi-band massive MIMO optimized for dense urban and suburban coverage with an emphasis on energy efficiency. Its product breadth supports aggressive capacity-dense builds where power and spectrum efficiency are priority metrics.

Samsung (Suwon, South Korea) — Concentrates on high-throughput massive MIMO radios and has active programs in non-terrestrial network (NTN) testing. Samsung is attractive to operators looking to push peak-user throughput and explore satellite-assisted coverage.

ZTE (Shenzhen, China) — Delivers AAU configurations optimized for macro coverage-capacity balance, including hybrid designs that reduce integration friction for operators moving from legacy architectures.

CommScope (Claremont, NC, USA) — A leading supplier of passive and hybrid panel antennas with multi-port configurations for macro sites; strong channel relationships and RF integration expertise make CommScope a common partner for tower and site vendors.

Amphenol Antenna Solutions (Wallingford, CT, USA) — Specializes in passive cellular antennas, with growing emphasis on sustainability and manufacturability — factors that matter for large-scale replacement programs and operator ESG targets.

Comba Telecom (Hong Kong) — Focused on practical base station antennas and distributed systems; competitive on cost and regional support for dense urban builds.

Corning (Corning, NY, USA) — Known for distributed antenna systems and optical/RF integration for in-building 5G NR coverage; its optical expertise is increasingly relevant as operators balance fiber backhaul economics.

JMA Wireless (Liverpool, NY, USA) — Offers DAS and antenna solutions with domestic US manufacturing — a differentiator in markets where supply-chain provenance and local content matter.

SOLiD (Seongnam, South Korea) — Specializes in venue and transport DAS deployments, addressing complex underground and indoor high-density use cases.

Tongyu Communication (Zhongshan, China) and PROSE Technologies (Germany) — Provide passive antenna solutions with a focus on multi-band capability and sustainability, respectively, and are often selected for targeted cost-sensitive or ESG-aligned projects.

Collectively, the market shows meaningful concentration: the top three and top five suppliers control a substantial share of revenue and influence on standards and roadmaps. This dynamic affects partner negotiation leverage, component lead-times and availability of integrated solutions for complex deployments.

Standards-driven product change: 3GPP’s Release 19 OTA spatial emission limits for upper-6 GHz operations (adopted in 2025) change antenna test benches and certification requirements. Operators must align RF front-end selections and site acceptance plans to these new baselines to prevent re-work.

Spectrum auctions and pipeline: National-level spectrum actions (including mandated auctions and identification of new mid/high band ranges) will materially affect where and how operators prioritize antenna investments — particularly for sub-6 GHz densification and midband capacity builds.

Backhaul economics: Fiber deployment costs remain a major component of 5G site economics. With fiber pricing volatility and surges in demand for specialized bend-insensitive and high-density cables, operators need to optimize fiber strategies, including mixed fiber-wireless fronthaul, to control rollout budgets.

Testing and NTN readiness: Recent certifications and testing milestones for NTN and OTA conformance indicate growing maturity of non-terrestrial use cases. Early adopters of NTN-capable antenna systems may capture new service opportunities but must budget for bespoke conformance testing.

Prioritize flexibility: Adopt antenna designs and procurement contracts that enable phased upgrades between active, hybrid and passive deployments to match spectrum availability and traffic build-out.

Lock in compliance early: Integrate Release 19 OTA emission criteria into procurement acceptance tests and field verification procedures to avoid expensive retrofits.

Hedge supply risk: Establish dual sourcing for critical components (e.g., AAU modules, fiber cables) and consider pre-certified integration kits to shorten site acceptance timelines.

Use the report’s TCO playbooks: Run our build-versus-buy calculators on representative deployment clusters to quantify trade-offs between vendor-integrated AAUs and disaggregated passive-active architectures.

Plan procurement cadence against auction timelines: Synchronize capex phases with known national spectrum auctions and release schedules to maximize ROI on densification spends.

This press preview is designed to give C-suite and deployment leaders the strategic context needed for 2026 planning. PW Consulting’s full Worldwide 5G NR Antenna Market report contains the granular scenario models, TCO worksheets, vendor scorecards and compliance checklists that translate these strategic insights into procurement-ready decisions. To access detailed segmentation, regional rollout maps and vendor product-level assessments, please consult the full report.

For teams preparing 2026 budgets and RFPs, the report functions as an operational playbook: not only where the money will be spent, but how to sequence investments, which vendor capabilities matter most, and how to mitigate the principal regulatory and supply-side risks now shaping the 5G antenna landscape.

For detailed analysis of this topic, please visit the official page:Worldwide 5G NR Antenna Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com