The Overlooked Dangers Shaping Oil and Gas Safety Today

Other |

2026-04-24 13:19:10

PW Consulting’s new market study on Worldwide 3D Automated Optical Inspection Equipment in the PCB market (base year 2025) delivers a forward-looking, actionable roadmap for executives planning capital allocation, supplier strategies, and technology roadmaps in 2026. Built on a rigorous historical series (2020–2025) and a seven-year forecast horizon (2026–2032), the report quantifies a robust market expansion—anchored by a compound annual growth rate (CAGR) of 11.2%—and translates that growth into pragmatic choices for OEMs, EMS providers, test-equipment vendors, and strategic investors.

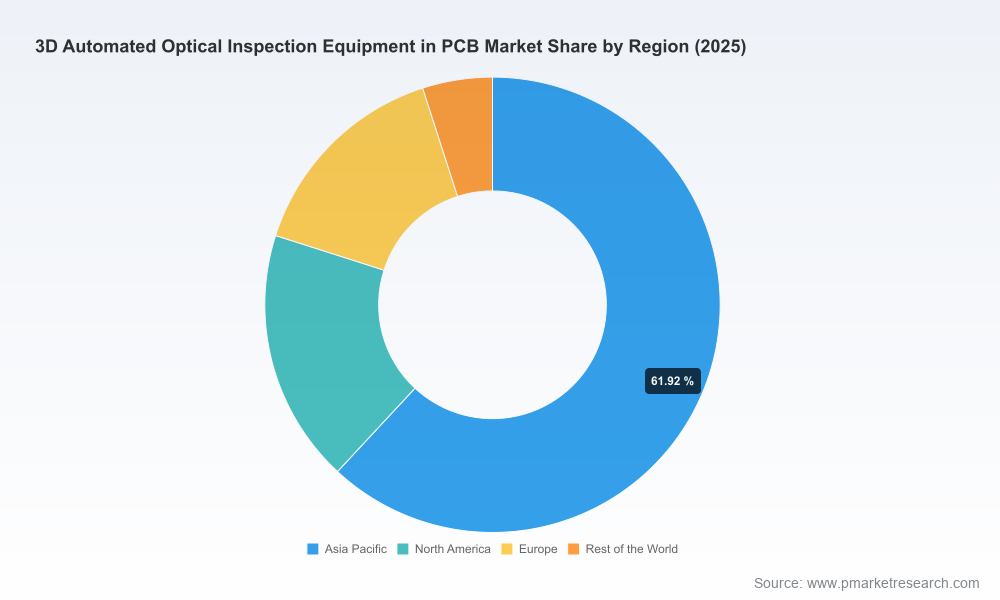

Worldwide 3D Automated Optical Inspection Equipment in PCB Market

The evolution of PCB complexity (HDI routing, micro-BGAs, and ultra-fine pitch components), coupled with the mobility of high-value electronics into automotive, telecommunications, and medical systems, has elevated the strategic importance of 3D AOI. In an environment where component densities and reliability expectations rise in tandem, a single percent improvement in first-pass yield can translate into meaningful margin recovery across production lines. PW Consulting’s study quantifies the market at a multi-hundred-million-dollar scale in 2025 and projects it to more than double by the end of the forecast period—evidence that 3D AOI is becoming a linchpin capital investment for competitive manufacturers.

Worldwide 3D Automated Optical Inspection Equipment in PCB Market

Demand drivers: Escalating inspection requirements for advanced packages (e.g., micro-BGA, 01005 passive components), higher automation to offset labor constraints, and expanded use in safety-critical sectors are primary demand pushes.

Worldwide 3D Automated Optical Inspection Equipment in PCB Market

Supply-side friction: Lead times for high-resolution 3D camera modules averaged 16–20 weeks in Q4 2025 due to lingering semiconductor shortages, compelling procurement teams to plan equipment cycles with longer horizons and to consider modular upgrade paths.

Regulatory and standards pressure: The 2025 update to IPC standards (e.g., tightened 3D height-measurement accuracy requirements) raises the bar for qualification and acceptance criteria in high-reliability production lines, affecting both equipment selection and process validation timelines.

Trade and policy risks: Export controls on advanced imaging sensors and new tariff structures in key markets are already influencing sourcing strategies and regional supply footprints—risks that must be integrated into CapEx and supplier diversification plans.

Pricing dynamics: Optics inflation and component scarcity pushed average unit prices up in 2025, altering total cost of ownership (TCO) calculations and payback modeling for new 3D AOI investments.

The sector is concentrated: the top three suppliers command a majority share of market revenue, with the top five capturing roughly two-thirds of industry revenues. This concentration yields both stability and strategic negotiating leverage for large buyers, while creating opportunities for niche innovators focused on software, AI, and specialized sensors.

Koh Young Technology (Seoul): A perennial leader in true 3D imaging for high-speed SMT inspection. Recent product introductions underscore a continued emphasis on AI-enhanced defect detection and throughput gains—features that make Koh Young a primary contender for high-mix, high-volume lines requiring minimal false calls.

CyberOptics Corporation (Minneapolis): Known for multi-reflection suppression and fine-pitch capability, CyberOptics has refreshed its platform to address the smallest passive components, a move that strengthens its position in advanced consumer and telecom segments.

Viscom AG (Hannover): Focused on high-resolution imaging for HDI boards and large-scale throughput, Viscom’s recent demonstrations reflect a strategy that balances optical resolution with line-speed compatibility for high-volume manufacturers.

TRI (Taipei): Leveraging AI-driven analysis, TRI’s product suite targets solder-paste and component placement verification—areas where algorithmic improvements can reduce false positives and drive yield improvement without massive hardware swaps.

SAKI Corporation (Tokyo): Gimbal-less camera designs and precision height measurement are SAKI’s differentiators, particularly relevant to firms adopting stricter IPC measurement tolerances.

Mirtec Corporation (Oxford, CT): High-resolution imaging and laser profiling for post-reflow inspection position Mirtec well in mixed-model lines seeking versatile inspection stacks.

Nordson Test & Inspection (Carlsbad): By combining AOI and AXI capabilities into hybrid platforms, Nordson targets customers with complex, high-mix product portfolios that value consolidated inspection workflows.

Recent vendor moves—product launches, platform upgrades, and certifications—signal an industry focus on AI, finer inspection tolerances, and support for the smallest components. Buyers should evaluate roadmap maturity (software intelligence, sensor modularity, platform upgradability) as heavily as headline performance metrics.

Our report is designed as an execution tool for decision-makers. Beyond headline market sizing, it provides the operational templates and analytic frameworks that turn insight into procurement and operational choices:

Capital planning models: Interactive TCO and ROI templates that incorporate purchase price inflation, extended lead times, service and spare parts availability, and productivity uplifts to calculate realistic payback windows under multiple supply scenarios.

Supplier risk matrix: A granular diagnostic that maps vendors against strategic criteria—technology readiness, regional exposure to trade controls, service network density, spare-part lead times, and software update cadence—to prioritize strategic partnerships and dual-sourcing options.

Compliance and qualification playbook: Stepwise validation protocols aligned to the latest IPC standard updates and sector-specific acceptance thresholds, reducing qualification cycles and shortening time-to-revenue following equipment deployment.

Operational integration guidelines: Best-practice recipes for integrating 3D AOI into SMT and post-reflow workflows, including metrics for sampling vs. full-line inspection, data harmonization with MES, and closed-loop process improvements between inspection, placement, and rework.

M&A and partnership scouting: Criteria-based target screening for corporate development teams seeking tuck-ins or technology acquisitions—especially relevant for suppliers aiming to bolster software/AI capabilities or sensing modules.

PW Consulting’s analysis yields a concise set of actions for senior executives and plant managers preparing for the 2026 planning cycle:

Adopt a staged CapEx cadence: Prioritize modular, upgradeable systems that allow incremental investment in sensors and software. Given extended camera-module lead times, early procurement windows and staged roll-outs minimize line disruption and protect margins.

Embed supply-chain contingencies into vendor contracts: Negotiate clauses covering sensor delivery SLAs, substitute sourcing, and joint risk-sharing for critical optics components to mitigate the impact of continued supply-chain tightness and export-control exposure.

Elevate inspection spec governance: Update inspection acceptance criteria and qualification plans to reflect tightened IPC requirements and to prevent downstream escapes—this reduces long-term warranty and field-failure costs.

Prioritize software and analytics: Vendors with strong AI and false-call reduction capabilities can deliver quicker yield uplift than raw sensor upgrades. Evaluate software licensing models, continuous-learning frameworks, and data-privacy practices.

Consider geographic sourcing shifts: Tariffs and export controls materially affect landed cost and delivery risk. For regionally exposed operations, evaluate localized equipment sourcing or regional service hubs to preserve uptime and predictability.

The comprehensive study couples quantitative forecasting with executable tools—without disclosing sensitive customer-level data in this briefing. The full deliverable includes:

Market-size forecasts and scenario analyses through 2032, with sensitivity runs on pricing, supply disruption, and regulatory tightening.

Vendor benchmarking across technology, service, and financial vectors, along with detailed SWOTs and go-to-market implications.

Procurement playbooks, TCO calculators, and inspection qualification templates you can adapt directly to your operations.

Case studies documenting line-level yield improvements, rework avoidance, and post-deployment ROI from representative deployments across automotive, telecom, and consumer electronics settings.

This briefing frames the strategic choices that will matter most in 2026: timing of capital deployment, the balance between hardware and software investment, supplier risk management, and compliance-ready qualification. For procurement directors, operations leads, and corporate strategists, the PW Consulting report transforms market growth projections and competitive signals into a prioritized action plan—one that reconciles rapid technological change with pragmatic constraints in supply and trade policy.

To access the complete dataset, vendor scorecards, and the plug-and-play tools referenced here, please consult the full report on PW Consulting’s website. The full report contains the detailed regional and segment splits, vendor revenue breakdowns, and downloadable Excel models that underpin the scenarios summarized in this release.

For detailed analysis of this topic, please visit the official page:Worldwide 3D Automated Optical Inspection Equipment in PCB Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com