Couples Massage Toronto: Benefits, Costs & Expert Guide

Other |

2026-07-01 06:16:15

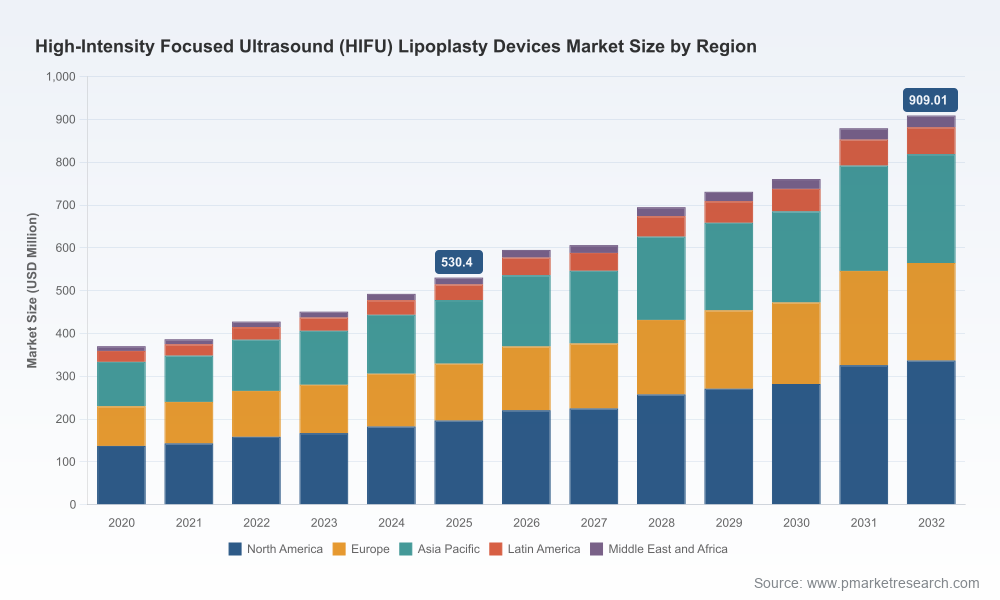

As HIFU-based lipoplasty moves from a niche clinical technique toward broader commercial adoption, executive teams must translate accelerating market signals into concrete strategic moves. Our latest PW Consulting report shows the global HIFU lipoplasty devices market reached approximately USD 530.4 million in 2025 and is growing at a compound annual growth rate (CAGR) of 8.01% through the 2026–2032 forecast horizon. This trajectory creates a multi-year window in which product, regulatory and commercial choices made in 2026 will disproportionately determine competitive advantage across the decade.

Worldwide High-Intensity Focused Ultrasound (HIFU) Lipoplasty Devices Market

Timing the investment: With steady mid-single-digit CAGR and a marked acceleration in the later forecast years, companies must choose whether to accelerate capital deployment now (R&D, manufacturing scale-up, clinical trials) or pursue a disciplined wait-and-see market-entry. The report quantifies the tradeoffs and break-even timelines for both options.

Worldwide High-Intensity Focused Ultrasound (HIFU) Lipoplasty Devices Market

Regulatory positioning as strategy: HIFU devices are regulated across multiple jurisdictions with rigorous safety and evidence requirements. Our analysis maps the fastest practical pathways to regulatory acceptance and shows how regulatory strategy intersects with clinical evidence generation and reimbursement engagement.

Worldwide High-Intensity Focused Ultrasound (HIFU) Lipoplasty Devices Market

Commercial go-to-market playbooks: Adoption is driven not only by technology but by training, channel configuration and payer acceptance. The report provides tested go-to-market blueprints tailored to device archetypes (stationary consoles vs. portable models) and to different end-user profiles.

M&A and partnership imperatives: Market concentration metrics indicate a moderately consolidated competitive landscape. For buyers and investors, we identify the archetypal targets that deliver the most leverage against product, IP and distribution gaps.

Proprietary market model (2020–2032): An editable financial model with base-year calibration, scenario toggles, sensitivity tables and a Monte Carlo module that allows executives to stress-test volume, pricing and reimbursement assumptions.

Commercialization playbooks: Step-by-step launch plans for different device formats (console vs. portable), including channel economics, training curricula, clinical trial sizing and ideal pilot geographies.

Regulatory and reimbursement roadmap: A jurisdiction-by-jurisdiction decision tree that reconciles device classification, premarket evidence expectations, and payer engagement milestones. Actionable checklists reduce time-to-market risk.

Technology and IP benchmarking: Side-by-side technical assessment of transducer architectures, cartridge strategies, energy-delivery trade-offs, and clinical endpoints — with implications for lifecycle management and modular upgrade paths.

Competitive playbook and heatmaps: Market-positioning matrices, capability gaps, and prioritized whitespace opportunities that inform where to invest in clinical studies, marketing, or M&A.

M&A and valuation toolkit: Comparable transaction analysis, target scorecards, synergies playbooks and a negotiation-ready valuation framework tailored to medtech investors and strategic acquirers.

Primary research library: Summaries of interviews with clinicians, opinion leaders, payers and channel partners, plus anonymized survey data that reveal adoption barriers and willingness-to-pay across provider types.

The HIFU lipoplasty competitive field is characterized by a mix of legacy players, specialty medtech firms and regionally strong OEMs. Three-to-five firm concentration metrics indicate a moderate level of market consolidation (CR3: 38.5%; CR5: 52.1%), which creates meaningful opportunities for challengers with differentiated clinical evidence or disruptive product form factors.

Liposonix (Hologic) — Historically important as an early entrant, its Liposonix system helped define the clinical pathway for non-invasive fat reduction. Note that Liposonix as a commercial product was phased out in prior years; its legacy continues to inform clinical expectations and competitive benchmarks.

Ulthera (Merz Aesthetics) — Ultherapy has evolved from skin-tightening into body-contouring indications through iterative evidence generation and regulatory engagement. Merz’s recent regulatory wins demonstrate how expanded indications can materially broaden addressable use cases.

InMode — Actively expanding its product stack with enhanced transducer technology and newer form factors. A late‑2024 product launch introduced upgraded transducers aimed at improving depth and treatment efficiency, illustrating the type of incremental innovation that can shift provider preference.

Hironic — A regional stronghold with ongoing product updates and CE mark renewals, highlighting the importance of sustained post-market surveillance and cartridge/consumable lifecycle management for market acceptance.

Strategic implication: incumbents compete on technology differentiation (transducer and cartridge design), clinical evidence, and distribution breadth. New entrants should prioritize one or two of these vectors rather than attempt full-spectrum competition from day one.

Device makers must navigate a tripartite dynamics set: regulatory clearance, reimbursement policy, and clinician adoption. Regulatory frameworks in major markets demand robust safety and efficacy evidence; European regulations emphasize post-market surveillance, while North American pathways require clear demonstration of safety and intended performance. Reimbursement coverage exists in relevant procedural codes, which materially supports adoption when combined with strong clinical outcomes and repeatability.

Clinical training and outcomes consistency are additional adoption gates. HIFU operators require procedural training to achieve reproducible results; devices that reduce operator dependence through automation and standardized cartridges consistently face a lower barrier to adoption.

Prioritize regulatory-first development — Align R&D and clinical plans with the most efficient regulatory pathways for your target markets. Early engagement with regulatory bodies and well-designed 510(k) or equivalent submissions shorten commercialization cycles.

Build reimbursement enablement into clinical programs — Design pivotal studies to generate the outputs that payers and coding committees require; incorporate economic endpoints into trial protocols to accelerate coverage conversations.

Choose focused commercialization anchors — Pilot in provider segments where training investment yields rapid repeatability (e.g., high-volume aesthetic clinics or specialized surgical centers), then scale via bundled services and consumable models.

Invest in modular product architecture — A cartridge/transducer ecosystem that supports incremental upgrades and cross-compatibility with future energy-delivery improvements reduces long‑term customer acquisition costs and creates recurring revenue through consumables.

Use M&A strategically — Given the moderate concentration, consider tuck-in acquisitions to access niche clinical evidence, complementary IP or field service capabilities rather than broad horizontal roll-ups.

Prepare for channel-enabled scale — Train trainers, certify centers of excellence, and design service level agreements that reduce downtime. Field service and consumable supply reliability materially influence purchase decisions.

PW Consulting’s Worldwide HIFU Lipoplasty Devices Market report is built as an operational toolkit for executives who must make binding choices in 2026. Beyond headline market projections, the deliverables include an executable launch plan, regulatory checklists, clinical trial design templates, a payer engagement roadmap, an M&A playbook and a calibrated market model you can adapt to internal assumptions.

We intentionally reserve granular regional and end-user splits in the subscriber-only dataset to maintain the “trailer” approach: this brief demonstrates the depth and actionable nature of our analysis while directing stakeholders to the full report for the segment-level intelligence that underpins prioritization and transaction-level decisions.

Stakeholders that align product development, regulatory strategy and commercialization execution in 2026 will capture asymmetric returns as the HIFU lipoplasty market scales. Whether you are a device OEM, investor, or strategic partner, the choices you make this year — on clinical evidence, regulatory timing, and channel configuration — will determine whether you lead, follow, or exit. PW Consulting’s full report equips teams with the data, frameworks and playbooks needed to make those choices with confidence.

To access the full dataset, regional/end-user breakdowns, and the editable market model, request the complete Worldwide HIFU Lipoplasty Devices Market report from PW Consulting.

For detailed analysis of this topic, please visit the official page:Worldwide High-Intensity Focused Ultrasound (HIFU) Lipoplasty Devices Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com