Budesonide Inhaler Market Insights and Growth Trends

Networking |

2026-06-16 06:29:12

PW Consulting today publishes a focused industry briefing derived from its comprehensive market research report on the Worldwide Automatic Cosmetic Powder Pressing Machine market. As brands and contract manufacturers accelerate automation and precision across compact cosmetics production, our analysis distills the macro trajectory, competitive dynamics, and immediate strategic moves that matter for 2026 capital allocation and product roadmap decisions.

Worldwide Automatic Cosmetic Powder Pressing Machine Market

The market for automatic cosmetic powder pressing machines has demonstrated steady expansion through the 2020–2025 historical window and enters 2026 with clear momentum. Our base-year evaluation (2025) places the global market well into the mid‑three‑figure million USD range, and the outlook to 2032 reflects a compound annual growth rate (CAGR) of approximately 6.78% over the 2026–2032 forecast horizon.

Worldwide Automatic Cosmetic Powder Pressing Machine Market

Put simply, demand is shifting from one-off, labor‑intensive presses to integrated automatic and servo-driven systems that prioritize repeatability, throughput, and regulatory compliance. This growth is not uniform — it is concentrated where brands and contract manufacturers prioritize automation, quality control, and faster time-to-market for color cosmetics — and that unevenness creates strategic windows for targeted investment.

Worldwide Automatic Cosmetic Powder Pressing Machine Market

Regulatory-driven demand for consistency: Recent regulatory frameworks — notably enhanced GMP expectations in primary export markets — are increasing procurement of automated presses that deliver verifiable process control and traceability. Equipment that integrates data capture and adverse-event traceability is moving from "nice-to-have" to procurement precondition.

Labor and cost pressures accelerating automation: Rising input costs and persistent labor shortages are prompting manufacturers to shift CapEx toward machines that reduce manual touchpoints. Across our client engagements, anticipated input-cost inflation has been a decisive trigger for earlier replacement cycles and retrofits.

Input materials and supply continuity: Structural components, notably steel for press frames, saw price normalization through mid-2025 with modest upward pressure into early 2026. Manufacturers should factor medium-term material cost volatility into procurement timing and total cost of ownership (TCO) models.

Technology convergence: Machine builders increasingly bundle servo actuation, PLC controls, precision filling, and Industry 4.0-capable telemetry. Buyers will benefit from evaluating vendor roadmaps for software openness and upgrade pathways rather than focusing solely on upfront machine throughput.

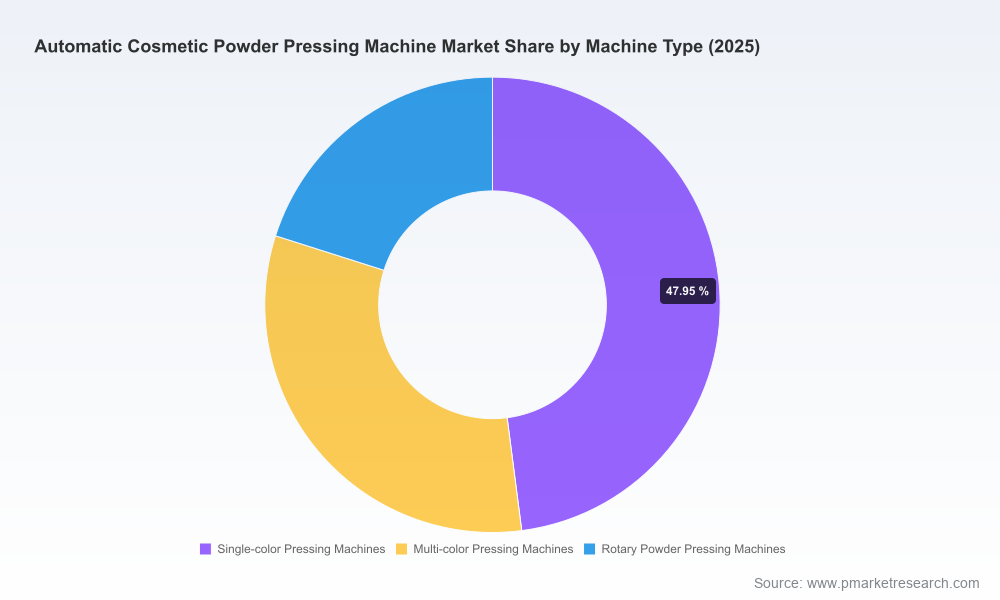

The report dissects the market across machine architecture, end-user profiles, and regional demand. While we intentionally withhold the granular regional and application breakdowns in this preview, the key takeaway for executives is clear: selectivity in product and geographic focus yields outsized returns. Opportunities cluster around automated, multi-mode pressing solutions for contract manufacturers and brand partners delivering SKU-rich color portfolios.

Our full dataset maps growth corridors by machine type and end-user across 2020–2032, supporting prioritization of R&D, production-expansion, and aftermarket service investments.

The sector combines century-old European engineering houses with highly agile Asian OEMs. Consolidation is moderate: top suppliers collectively capture just over half of market value, leaving meaningful room for regional specialists and technologically differentiated entrants.

GIENI (Shanghai GLENI Industry Co., Ltd.): Positioning itself with bottom-up compact solutions and servo-driven models, GIENI’s recent product feature updates emphasize operator ergonomics, auto discharging, and powder management systems. For buyers, GIENI represents a vendor oriented toward full-line automation and modular upgrades — suitable where rapid scale and consistent compaction are priorities.

Eugeng International Trade Co., Ltd.: With a presence at major trade shows and a product portfolio spanning full-automatic and lab-scale hydraulic options, Eugeng is a strong competitor for customers seeking breadth of configurations and demonstration support. Their trade show visibility underscores a go-to-market strategy that balances volume sales with partnership-driven installations.

Guangzhou Jutao & other Chinese OEMs: Several Guangzhou-based suppliers present customizable, cost‑competitive automatic powder pressing platforms. These vendors are attractive to contract manufacturers and growing regional brands prioritizing CAPEX efficiency and rapid lead times.

Lorenzato S.r.l. & Bonals Technologies (Europe): European suppliers stress precision, long-term durability, and compliance support — attributes that appeal to global brands and suppliers seeking Industry 4.0 compatibility and high service expectations.

Lab and semi-automatic suppliers (Henwi, Yeto): For R&D, small-batch innovation, and pilot lines, semi-automatic and lab-scale presses remain central. These platforms enable formula experimentation and small-series launches without the lead time and footprint of full‑scale automatic lines.

Recent vendor activity — product upgrades showcased at major expos and targeted feature releases in early 2026 — signals that incumbents are prioritizing software, modularity, and operator safety. Procurement teams should assess vendor roadmaps alongside immediate delivery capability.

Recalibrate CapEx timing to lock favorable TCO: With material costs and lead times still variable, buyers should model TCO scenarios that include short-term procurement to hedge against steel-price escalation versus delayed purchases that benefit from component availability and newer control features.

Prioritize modular automation and retrofit pathways: Choose platforms that support phased upgrades (servo modules, telemetry, precision filling) to extend asset life and spread investment across product launch cycles.

Embed compliance into procurement criteria: When MoCRA-like GMP requirements or equivalent standards are relevant to your market footprint, make process traceability, audit-friendly QC records, and supplier validation mandatory in RFPs.

Design for service and spare-parts economics: Evaluate vendors on spare‑parts availability, remote service capability, and mean time to repair — these factors can dominate uptime economics in multi-SKU compact operations.

Explore partnerships over outright buys for innovation speed: Co-development agreements with vendors that supply lab-scale and pilot machines can accelerate formula-to-shelf timelines and reduce commercial risk for new finishes and formats.

Our full report is designed as an executable tool for procurement, operations, and product strategy leaders. It combines:

Normalized historical market sizing (2020–2025) and a detailed forecast (2026–2032) with scenario sensitivities.

Vendor benchmarking that evaluates technical capabilities, upgradeability, and aftermarket economics.

Purchaser-focused checklists for RFPs, GMP/compliance alignment, and TCO modeling templates.

Actionable insights on where to prioritize automation investments by business model (brand owner vs. contract manufacturer) and launch cadence.

To preserve the strategic advantage of our clients — and in accordance with our "trailer" approach — this briefing highlights the implications of our findings; the full report contains the granular segmentation tables, regional demand matrices, and the proprietary dataset that underpins our recommendations.

Procurement leaders should use the briefing to set evaluation criteria and shortlist vendors based on upgradeability, compliance readiness, and service economics. R&D and manufacturing heads can align pilot capacity investments with a roadmap that anticipates multi‑SKU automation. Finance teams should run stress tests on TCO under the 6.78% CAGR scenario to determine optimal amortization and funding schedules.

PW Consulting is available for advisory engagements to convert the report’s strategic intent into detailed implementation plans: RFP design, vendor due diligence, and retrofitting roadmaps tailored to specific production footprints and regulatory exposures.

Executives seeking the full dataset, vendor scorecards, and the step-by-step procurement playbook can access the complete Worldwide Automatic Cosmetic Powder Pressing Machine Market report on the PW Consulting website. For organizations that require immediate, bespoke support, our senior consultants are scheduling strategy workshops and supplier evaluation clinics throughout Q3 2026.

For detailed analysis of this topic, please visit the official page:Worldwide Automatic Cosmetic Powder Pressing Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com