What Is Driving Growth in Digital Infrared Thermometer Market Post-Pandemic?

Networking |

2026-05-04 10:12:37

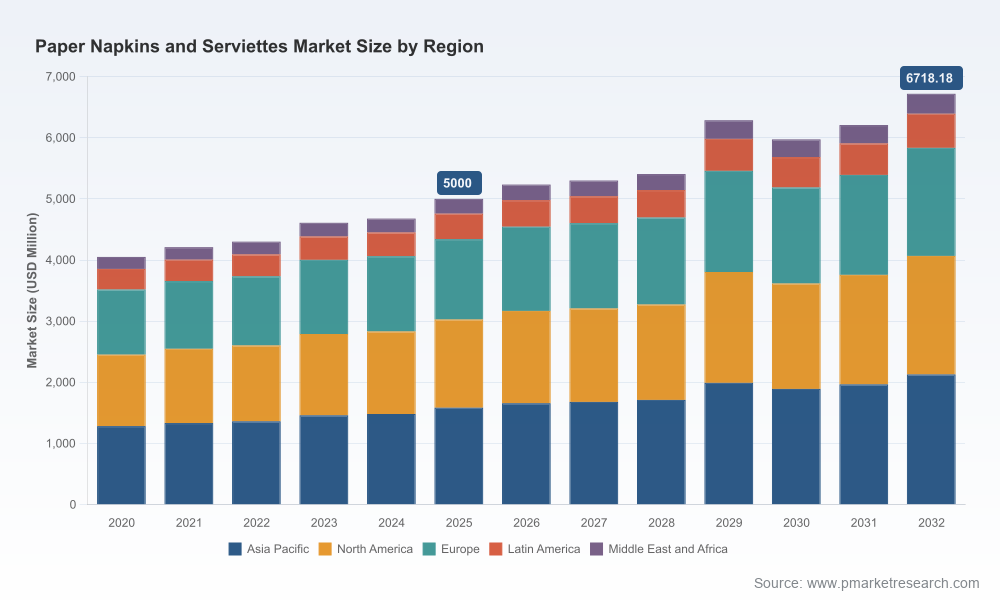

PW Consulting’s latest market briefing on the Worldwide Paper Napkins and Serviettes Market synthesizes macro trajectory, cost dynamics, regulatory pressure, and competitive maneuvering to help executives make high-conviction decisions in 2026. The global market reached an estimated USD 5,000.0 Million in 2025 and is projected to grow at a compound annual growth rate (CAGR) of approximately 4.31% across our 2026–2032 forecast window. This briefing highlights the strategic takeaways our clients will use to prioritize capital allocation, sourcing strategies, and product development — while the full report contains the granular models, segment-level forecasts, and supplier-level analytics that drive these conclusions.

Worldwide Paper Napkins and Serviettes Market

Post-pandemic consumption patterns are settling into new equilibria between out-of-home dining and at-home consumption; 2026 will see firms either lock in advantaged supply chains or surrender margin to input-cost volatility.

Worldwide Paper Napkins and Serviettes Market

Regulatory and commercial demand for higher recycled content and certified compostable options is no longer niche: procurement teams and brand owners must translate sustainability commitments into supply-side specifications or risk losing institutional contracts.

Worldwide Paper Napkins and Serviettes Market

Input-cost dynamics and concentrated supplier footprints mean capacity investments announced today (or the choice not to invest) will materially affect availability and margin across the next six years.

Our top-down model shows a stable, mid-single-digit growth market, with the USD 5,000.0 Million base in 2025 expanding under a 4.31% CAGR to a materially larger market by 2032. Growth is driven by three interacting vectors: a resilient foodservice recovery, premiumization of retail household formats (absorbency and multi-ply claims), and an accelerating institutional shift to certified compostable or high-recycled content products.

For leaders, this profile implies predictable aggregate demand but meaningful heterogeneity beneath the headline. That heterogeneity creates pockets of outsized opportunity — e.g., value-engineered away-from-home systems, compostable product lines for healthcare and hospitality, and private-label programs tuned to local recycling infrastructures.

Raw material pressure has re-emerged as a core risk to operating margins. European jumbo roll prices and pulp indices have moved higher in early 2026, and sanitary tissue producer price measures are signaling persistent cost pressure in North America.

These input moves are increasing the importance of efficient inventory and pass‑through mechanisms. Successful operators are adopting tiered pricing, formula-based cost clauses in long-term contracts, and route-to-market changes (e.g., dispensers that reduce consumption).

There is a parallel capex response: new capacity in North America and targeted retrofits to produce higher recycled-content or compostable grades. Firms that time expansion to anticipated pulp-price cycles and regulatory shifts will unlock margin advantages.

Across the EU and North America, procurement standards and municipal composting programs are reshaping specification sheets. Buyers increasingly require BPI certification, higher recycled fiber content, and clear end-of-life claims. These requirements are not simply marketing fodder — they change raw material sourcing, production processes, and third‑party testing needs. For C-suite teams, the strategic question is whether to retrofit existing platforms or invest in differentiated, certified SKUs that command a premium in institutional tenders.

The market exhibits moderate concentration: the combined share of the three largest firms sits at a level that favors scale advantages, while the top five increase the barrier to entry for large institutional supply. This structure creates room for midsize, specialized players to win with product differentiation and local agility.

Kimberly‑Clark Corporation continues to leverage its global brands and away‑from‑home channels, pushing higher recycled content and sustainable packaging through large-scale reformulations. Expect continued emphasis on brand-led differentiation and sustainability certification as a commercial gatekeeper for major retail and institutional buyers.

Procter & Gamble plays to strengths in absorbency and multi‑use functionality, maintaining a dominant retail positioning in select markets. Their playbook centers on premium retail SKUs and operational discipline in North America.

Georgia‑Pacific focuses on commercial and institutional channels with an eye to compostable options; this makes them a natural partner for foodservice operators seeking circularity commitments.

Essity pushes system-level solutions (dispenser + serviette) that reduce consumption, which is both a sustainability and cost story for buyers. Their rollouts of next‑generation dispensers materially alter demand profiles at the point of use.

Sofidel is capitalizing on recent capacity additions in North America to shorten supply chains and serve customers with regional preferences, while Cascades, WEPA, Metsa, APP, Hengan, La Pajarita, and family-owned specialists like Mank cover a spectrum from certified compostable offerings to bespoke printed serviettes.

Recent corporate developments underscore these strategies: Essity’s broad dispenser launch in early 2026, Sofidel’s new Ohio facility, Kimberly‑Clark’s recycled-content reformulation, and Cascades’ BPI-certified lines all point to a market where product and system innovations are replacing purely price-based competition.

Sourcing and Cost Management: Establish multi-tiered supplier portfolios combining global majors for scale and regional specialists for flexibility. Negotiate formula-based escalation clauses tied to pulp indices where possible.

Portfolio and NPD: Prioritize development of certified compostable and high‑recycled content SKUs for institutional channels, and modularize product families to reduce SKU proliferation while addressing buyer-specific requirements.

Commercial Models: For foodservice, consider bundled offers (dispenser + consumables) that lock in volume and enable predictable consumption reductions — a value proposition increasingly favored by sustainability-driven buyers.

M&A and Capacity Decisions: Use scenario-based valuation models that incorporate pulp-price volatility and policy trajectories. Small regional acquisitions can be an efficient way to secure certified capacity and local customer relationships without the long lead times of greenfield projects.

Innovation and Footprint: Invest selectively in tissue lines that support recycled fiber and compostable polymer coatings. Retrofit programs that deliver certification at lower incremental capex offer compelling returns in markets with stringent procurement standards.

Continued pulp-price spikes or supply disruptions could compress margins and catalyze consolidation; firms without hedging or flexible sourcing will be most exposed.

Regulatory divergence across jurisdictions (e.g., differing composting infrastructures) could fragment demand and complicate global SKU rationalization.

Technology adoption (dispenser systems that reduce consumption) may shrink unit volumes even as revenue rises for integrated suppliers; players must revise unit-economics models accordingly.

Proprietary bottom‑up demand model (2020–2032) with scenario runs for alternative recovery and input-cost paths.

Segmentation deep dives by product type, channel, and region, and a supplier matrix scoring capacity, sustainability credentials, and commercial reach.

Price‑pass‑through and sensitivity analyses linking pulp indices and sanitary tissue PPI to gross margin outcomes under multiple contracting strategies.

Commercial playbooks for foodservice and retail, including dispenser economics, private label strategies, and tender playbooks for institutional buyers.

M&A screening with prioritized targets and accretion/dilution scenarios, and an integration checklist for certified/compostable assets.

Primary interviews with five leading procurement officers and sixty on-the-ground retailer and foodservice buyers, plus a patent and technology brief on coatings and compostable binders.

Executives that treat 2026 as a tactical year for building durable sourcing advantage, certifying product lines, and embedding system-level offers (e.g., consumable + dispenser) will emerge with improved margins and stronger client retention. The market’s overall growth is steady and predictable at the headline level, but the profit pool is reshaping: sustainability, capacity timing, and consumption-reduction technologies are redefining where value accrues. PW Consulting’s full report provides the granular models and supplier-level intelligence required to convert these strategic windows into executable roadmaps.

For access to the complete dataset, detailed segment outputs, and bespoke advisory support, please visit the PW Consulting report page or contact our industry practice lead. The executive summary above is designed to guide your initial 2026 planning; the full analysis converts that guidance into specific actions and quantified scenarios.

For detailed analysis of this topic, please visit the official page:Worldwide Paper Napkins and Serviettes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com