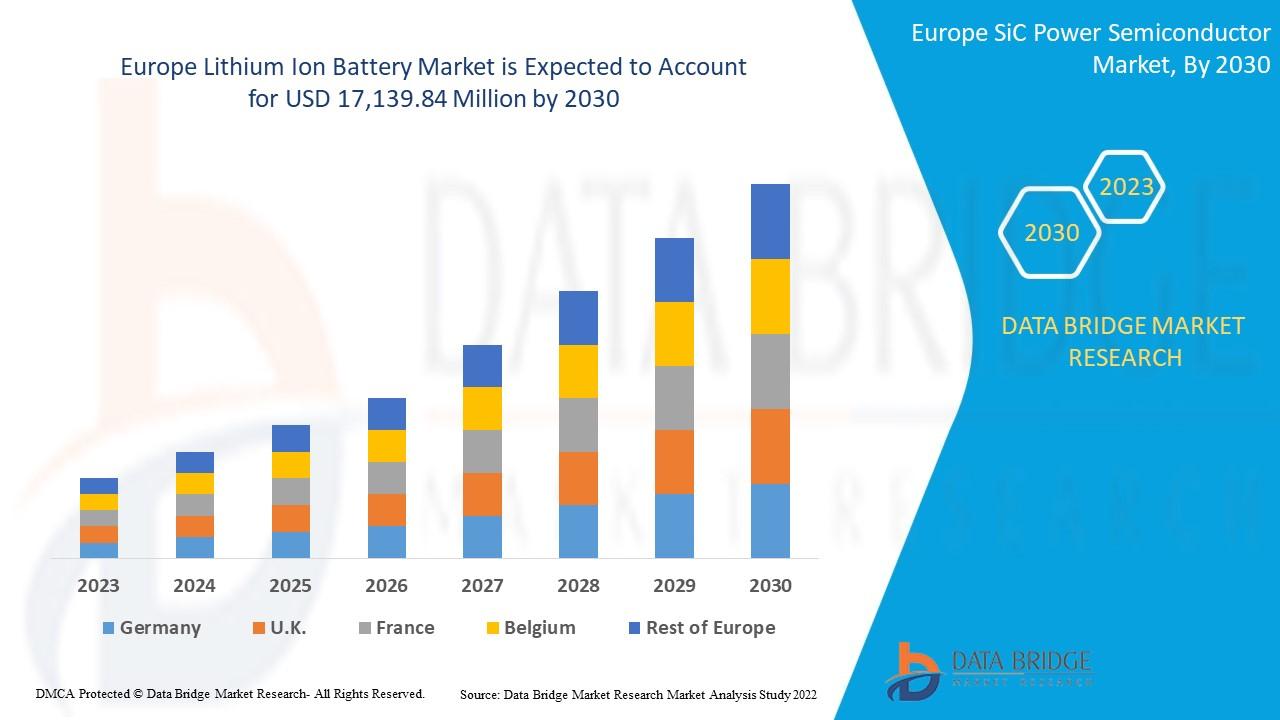

Europe Lithium Ion Battery Market Size, Share, Trends, Industry Analysis and Forecast by 2030

Other |

2026-05-27 10:37:00

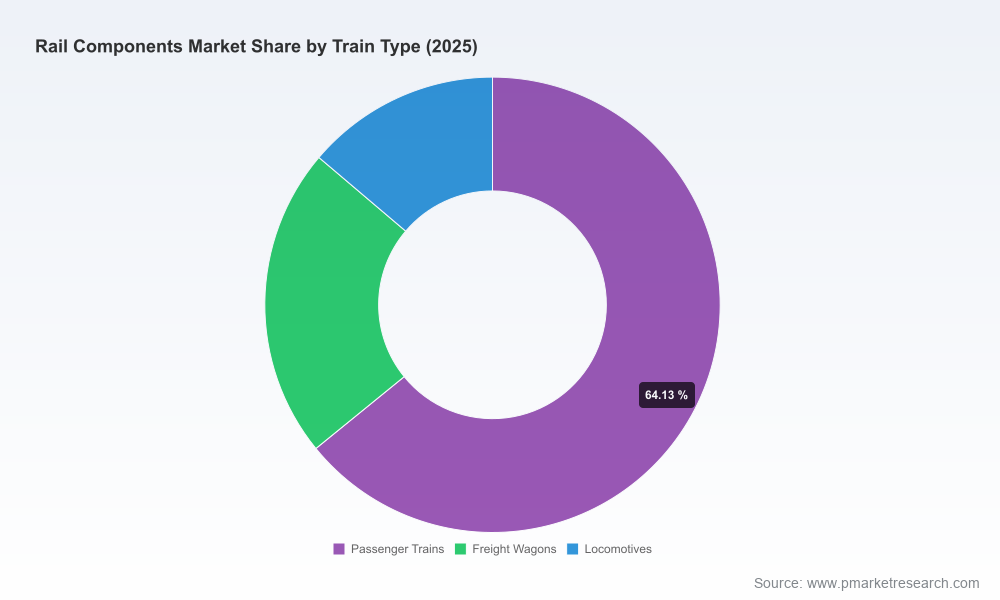

As global rail systems enter a decisive decade for electrification, automation and sustainability, PW Consulting’s latest Worldwide Rail Components Market report (base year 2025) provides the strategic intelligence executives need to set course for 2026. The market returned to growth after mid‑cycle volatility, reaching an overall market size of approximately USD 72.5 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of about 4.65% through our 2026–2032 forecast. By 2032 the market approaches the USD 100 billion threshold—an important psychological and strategic milestone for suppliers, OEMs and asset owners planning investment, sourcing and M&A decisions in the coming 12–18 months.

Worldwide Rail Components Market

Timing: 2026 is the first full planning year after several sweeping regulatory and technical inflection points came into force or became binding. Capital programs that started in 2024–2025 now enter procurement slots where component selections, certification and localization choices will lock in supplier relationships for years.

Worldwide Rail Components Market

Risk calibration: Raw‑material cost trends and carbon‑border measures are materially changing the economics of component manufacturing. Our modelling integrates price shocks, certification lead times and tariff exposure so buyers and suppliers can quantify 2026 procurement risk and margin pressure on product families and manufacturing footprints.

Worldwide Rail Components Market

Value capture: The market shifts from pure hardware to software‑enabled systems and lifecycle services. Players that convert one‑off sales into recurring digital and maintenance revenues stand to outperform the market average embedded in our CAGR projection.

Regulatory acceleration. Mandates for interoperable digital signaling and advanced train control architectures are compressing product development and certification timelines. Key markets have introduced baseline interoperability requirements that mean suppliers must prioritise compliant platforms now to be procurement‑eligible in 2026 tenders.

Raw material and carbon economics. Rail steel grade demand and price volatility have a direct bearing on both OEM margins and asset lifecycle costs. Simultaneously, cross‑border carbon adjustments are changing sourcing calculus—favoring localized or low‑carbon certified steel sources for projects tendered from 2026 onward.

Technology convergence. Automation (including driverless operations in selected corridors), electrified traction advancements and integrated fleet management are accelerating the bundling of mechanical and digital components. Procurement strategies must now contemplate system‑level compatibility, cybersecurity and software life‑cycle management alongside traditional BOM considerations.

Aftermarket importance. With lifecycle service revenues proving more resilient than new build sales in recent cycles, component makers and rolling stock suppliers should increase focus on predictive maintenance offerings, spare‑parts distribution networks and extended warranties as strategic levers to stabilize revenue through 2026 and beyond.

The market exhibits moderate concentration: the three largest suppliers control a meaningful share of the market, and the top five extend that position further. This structure creates a two‑tier dynamic where global integrators and large component manufacturers lead platform standardisation and certification, while a broad base of specialists and regional players compete on cost, customisation and local content. For 2026 planning, buyers and investors should map suppliers across three dimensions: product breadth (hardware + software), certification footprint, and supply‑chain resilience.

Tier‑one integrators (examples): Companies with wide portfolios in traction, signalling, bogies and system integration continue to set interoperability standards and capture platform business in new metro and high‑speed programmes. Recent product launches in driverless operation platforms and expanded automation suites point to continued investment in turnkey offerings.

Braking, HVAC and critical mechanical specialists: Firms focused on braking systems, thermal management and entrance systems are pursuing bolt‑on acquisitions and R&D to expand into compact, lightweight and electronically integrated subsystems—moves that increase their relevance to both new‑build and retrofit markets in 2026 tenders.

Steel and track specialists: Companies supplying rails, switches and wheelsets are responding to demand for premium steels and certifications that meet heavy‑haul and high‑speed standards. Certification wins and regional qualifications will be decisive for supply appointments in 2026 procurement cycles.

New automation platform components unveiled by a major mobility player signal quicker adoption of driverless operations in target urban corridors—suppliers not on certified lists risk being excluded from the next wave of metro procurement.

Strategic acquisitions in compact braking components reinforce the push to consolidate subsystem suppliers and shorten time‑to‑market for integrated metro solutions.

Contract awards for digital fleet optimisers with large freight operators demonstrate how software optimisation can shift operating economics, a dynamic that incumbent component suppliers must address either through partnership or internal capability build.

Regional certification milestones in premium rail steel open new heavy‑haul opportunities but also highlight how technical compliance and regional standards can drive supplier selection away from purely price‑based decisions.

We designed the report as a toolkit for executives executing 2026 strategies. Key practical deliverables include:

A consolidated market model capturing historical dynamics (2020–2025) and a granular, scenario‑driven forecast for 2026–2032 that reconciles demand drivers, regulatory timelines and raw‑material scenarios.

Supplier benchmarking that evaluates product breadth, certification status, geographic manufacturing footprint and digital capability—enabling procurement teams to shortlist partners against 2026 RFP requirements.

Regulatory impact matrices that translate key mandates into compliance roadmaps, certification timelines and cost implications across product lines—designed for programme managers and compliance leads.

Supply‑chain heatmaps identifying single‑sourcing risks, critical raw‑material dependencies and localized exposure to carbon‑border tariffs, with mitigation playbooks for 12–24 month horizons.

M&A and alliance playbooks for mid‑sized suppliers and private‑equity investors, outlining value creation blueprints, integration risks and priority targets aligned with electrification and digitalisation trends.

For OEMs and system integrators: accelerate certification programmes for digital rail control and signalling suites now. Inclusion in 2026 tenders will depend on demonstrable compliance and integration testing with established ERTMS/PTC frameworks.

For component manufacturers: prioritise modular, software‑enabled variants of legacy products that facilitate remote diagnostics and predictive maintenance. Repackage offerings as lifecycle contracts to shift revenue mix toward higher‑margin service streams.

For procurement and asset owners: include carbon‑content and origin clauses in 2026 RFPs and run parallel qualification tracks for low‑carbon suppliers to avoid late‑cycle exposure to border adjustment measures.

For investors: target businesses that combine hardware scale with software monetisation pathways and demonstrable certification pipelines—these characteristics are likely to outperform the broader market trend embedded in our CAGR forecast.

Across the board: execute scenario planning that models at least two downside raw‑material shocks and one accelerated digital adoption case. Contracts and capex plans signed in 2026 will otherwise be vulnerable to mid‑term margin erosion.

PW Consulting’s scenario modelling shows that suppliers that balance global R&D scale with regional manufacturing and qualified certification are better positioned to win large, multi‑year frame agreements announced in 2026. For many tendering authorities, the combination of technical compliance, local content and low‑carbon supply chains will be as critical as unit economics in final supplier selection.

Integrate the report’s supply‑chain heatmaps into your supplier due‑diligence process to identify immediate single‑source vulnerabilities before issuing RFPs.

Use the regulatory impact matrices to align your product road map and certification investments with the timelines your procurement teams will face in 2026 tenders.

Apply our competitive benchmarks to structure strategic partnerships and to inform M&A target screening that accelerates your entry into digital and electrified system components.

The rail components market is entering a phase of structurally supported growth, driven by technology convergence, regulatory momentum and renewed capital programmes. Our headline numbers—a mid‑2020s market base and an approximate 4.65% CAGR through the 2026–2032 horizon—outline the scale and tempo of opportunity. But the real competitive edge in 2026 will come from tactical execution: faster certification, locally resilient supply chains, and converting hardware sales into software and service‑driven revenue streams.

PW Consulting’s Worldwide Rail Components Market report equips decision makers with the forecasts, risk models and operational playbooks required to make those choices with confidence. For organisations preparing 2026 procurement, product or investment plans, the report functions as both a compass and a toolkit—pointing to where growth will be captured and providing the steps to get there. To access the full dataset, country and sub‑segment forecasts, and supplier scorecards that underpin our strategic recommendations, please visit our report page.

For detailed analysis of this topic, please visit the official page:Worldwide Rail Components Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com