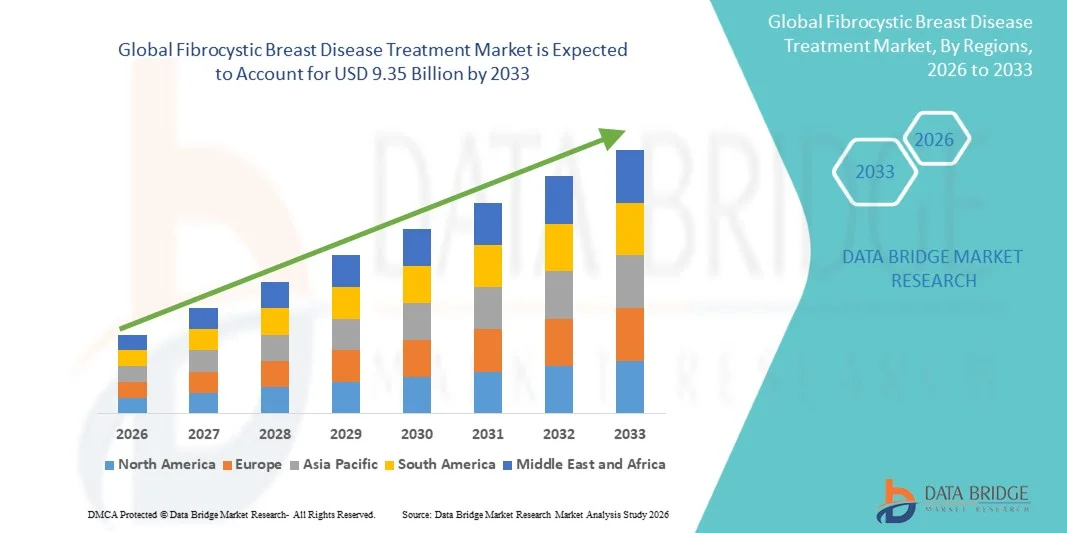

Fibrocystic Breast Disease Treatment Market Size, Share, Trends, and Industry Forecast by 2033

Other |

2026-06-04 09:05:01

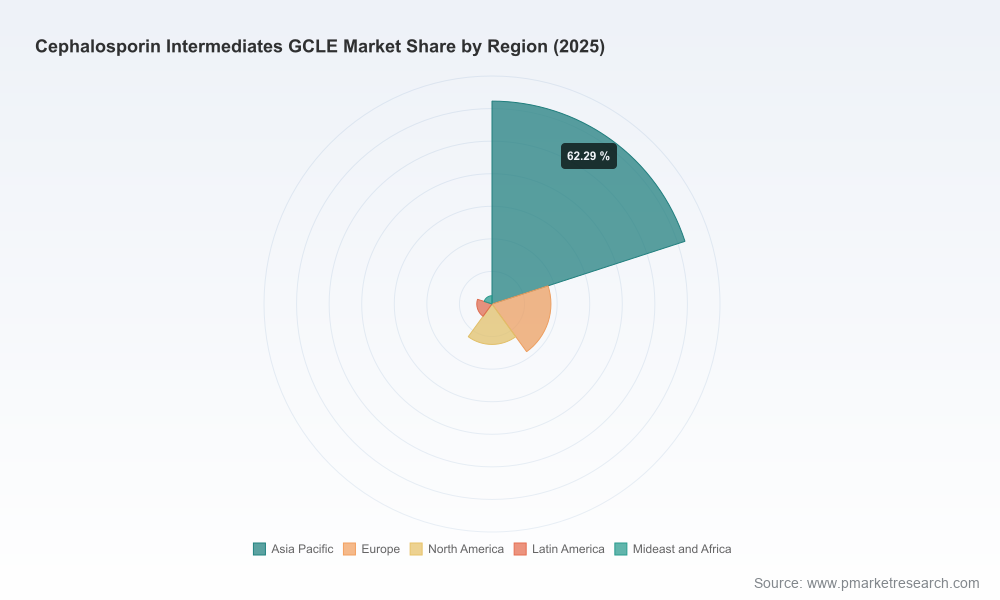

PW Consulting’s new market research brief on the Cephalosporin Intermediates GCLE market (base year: 2025; historical review: 2020–2025; forecast: 2026–2032) equips senior executives, corporate strategy teams and investors with targeted, decision-ready insight for 2026. Our top-line modelling shows the GCLE market reached approximately USD 392.4 Million in 2025 and is forecast to expand at a compound annual growth rate (CAGR) of 5.4% through 2032, culminating in a materially larger market by the end of the forecast window. The market exhibits a meaningful degree of concentration (three-firm concentration ≈ 58%, five-firm concentration ≈ 72%), implying scalable returns for incumbent scale players and attractive consolidation optionality for well-capitalized entrants.

Cephalosporin Intermediates GCLE Market

Timing of capacity investments: With steady mid-single-digit CAGR dynamics, near-term capacity allocation is a decisive lever — especially for firms balancing capital intensity, regulatory compliance, and quality uplift initiatives.

Cephalosporin Intermediates GCLE Market

Supply-chain and sourcing risk: The GCLE value chain is tightly coupled to penicillin feedstock flows. The lack of diversified penicillin suppliers beyond China creates a single-country dependency that cannot be viewed as short-term noise; it is a structural input risk that should influence procurement, hedging and near-shoring strategies.

Cephalosporin Intermediates GCLE Market

Regulatory arbitrage and export pathways: Recent regulatory developments in major manufacturing hubs have created selective windows for advantaged exporters. For example, advanced authorization mechanisms allow certain GCLE import pathways without minimum import price restrictions when tied to export-oriented antibiotic manufacture — a potential near-term margin uplift for export-centric producers.

Logistics and cost variability: Elevated international shipping costs and periodic container shortages remain part of the operating reality for intermediate exporters. These dynamics introduce episodic cost pressure that can materially affect landed costs and contract negotiation power.

Our full study is built for executives who need concise operational guidance without getting lost in raw tables. The report contains:

Robust market sizing and trend analytics (historical 2020–2025 and base-year 2025 benchmarking) and scenario-based projections for 2026–2032 that reflect supply-side constraints and likely regulatory evolutions.

Profitability and cost-stack breakouts that map raw material exposure, synthesis route differentials, energy & utilities sensitivity, and logistics pass-through effects.

Granular supply-chain heat maps highlighting penicillin sourcing, conversion nodes, and critical single points of failure across Asia–Europe–India corridors.

An actionable competitive playbook: capability matrices, capacity-to-demand overlays, and prioritized M&A targets aligned to strategic archetypes (scale-accretive buyouts, technology-driven niche plays, and downstream integration opportunities).

Regulatory and trade-impact modelling that quantifies the near-term opportunity created by export-facilitating authorizations and the longer-term implications of country-level raw-material concentration.

Investment and operational checklists for 2026: capital allocation guardrails, sample contractual clauses for long-term feedstock security, and best-practice templates for quality-control upgrades to support high-purity product lines.

Downstream demand anchors and product quality segmentation: Demand for GCLE is end-market driven by cephalosporin APIs used across a set of core molecules. Buyers increasingly differentiate by purity and process reliability. Producers positioned to supply high-purity grades with reliable lot-to-lot performance command premium pricing and lower commercial churn; this creates a two-track strategy for incumbents — defend scale in standard-grade volumes while investing selectively to move up the purity ladder.

Input concentration: Penicillin-G remains the primary feedstock for GCLE synthesis and, according to industry sources, is sourced predominantly from China. That concentration elevates sovereign and logistic risk and suggests firms should be considering multi-layered mitigation: strategic inventory buffers, long-term offtakes with Chinese suppliers, and targeted investments in alternative chemistry routes where technically and economically feasible.

Regulatory nuance as a commercial lever: Recent advanced-authorization schemes in certain manufacturing jurisdictions enable preferential import terms for GCLE when tied to export-oriented antibiotic production. Savvy producers that architect supply agreements and trade compliance around these schemes can reduce landed feedstock costs and improve competitive positioning on export programs.

Logistics as competitive friction: Elevated freight and container cost volatility materially changes landed-cost economics for exporters. Firms that optimize freight procurement, rationalize packaging and build regional distribution hubs will preserve margins and customer responsiveness.

Consolidation economics: With a high CR5 concentration and structural barriers to rapid greenfield scale-up (raw material access, capex needs, process know-how), the sector is primed for consolidation. Players considering M&A should prioritize targets that deliver immediate feedstock synergies, regulatory footprints in favorable jurisdictions, or hard-to-replicate quality credentials.

PW Consulting’s companion competitive profiles section canvasses active and listed manufacturers across Asia and India. These profiles evaluate production footprints, product breadth, licensing and trade capabilities, and strategic intent. Key players examined in the report include established multinational and regional manufacturers, with differentiated strategic postures:

Otsuka Chemical Co., Ltd. (Osaka, Japan) — the developer and a primary industrial-scale manufacturer of GCLE. Otsuka’s integrated approach and dedicated facilities (including an India plant) position it as a benchmark for quality and consistent global supply.

CSPC Cenway Tianjin Pharmaceuticals Co., Ltd. and Tianjin-based manufacturers — active suppliers with cost-competitive manufacturing bases focused on meeting large-volume API programs.

Listed Chinese manufacturers (selected players in Tianjin, Ningbo, Shandong and Jiangsu) — these firms bring scale and domestic supply-chain integration, often supporting both local API customers and export programs.

India-based suppliers (including Virchow Group and Otsuka Chemical India operations) — strategically positioned to serve global generics makers, with regulatory strategies calibrated to leverage export-favoring trade mechanisms.

Our profiles do more than list capabilities; they map each company’s strategic trade-offs (e.g., cost competitiveness vs. quality premium, domestic focus vs. export orientation), recent investments, and near-term capacity levers. For confidentiality and competitive sensitivity we provide directional positioning and qualitative strengths in this briefing; the full report contains deeper tabular benchmarking and capacity maps.

Secure feedstock: Prioritize long-term penicillin supply agreements and develop a layered sourcing approach combining contractual hedges, spot-market fallback, and, where feasible, small-scale domestic synthesis alternatives to reduce single-country exposure.

Upgrade selectively to high-purity production: Where market access and customer relationships permit, invest in targeted process upgrades and quality systems to capture premium demand and reduce customer switching risk.

Leverage trade policy: Structure export-oriented supply chains to exploit advanced-authorization and similar regulatory pathways that reduce landed feedstock cost and enhance margin capture.

Optimize logistics: Implement freight procurement strategies and explore regional warehousing to blunt shipping cost spikes and improve delivery reliability.

Pursue consolidation selectively: Use the current concentration structure to screen M&A targets that deliver feedstock integration, regulatory benefits, or quality differentiation rather than just near-term volume growth.

This briefing is an extract of a broader, evidence-based study that blends proprietary primary interviews, process-mapping, extensive trade-data analysis and scenario-based financial modeling. We balance strategic vision with implementation detail — from contractual clauses used in long-term penicillin offtakes to capex phasing calendars that reduce commissioning risk. The output is tailored to board-level strategy debates and CFO-level capital allocation decisions for the 2026 planning cycle.

We have designed the public briefing as a strategic trailer: it surfaces the signals and recommended moves but intentionally withholds the full segmentation tables, granular regional/application breakdowns and the complete company benchmarking matrix to preserve the commercial value of the underlying work. Senior leaders and strategy teams seeking the complete dataset, model files and the full set of practical templates (procurement contracts, quality upgrade checklists, M&A screening scorecards) are invited to access the full report via PW Consulting’s market research portal.

Contact PW Consulting for the full Cephalosporin Intermediates GCLE Market report to convert these insights into a 2026 action plan aligned with your risk appetite and growth objectives.

For detailed analysis of this topic, please visit the official page:Cephalosporin Intermediates GCLE Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com