https://www.facebook.com/GlucolynforBloodSugar

Art |

2026-05-25 15:12:45

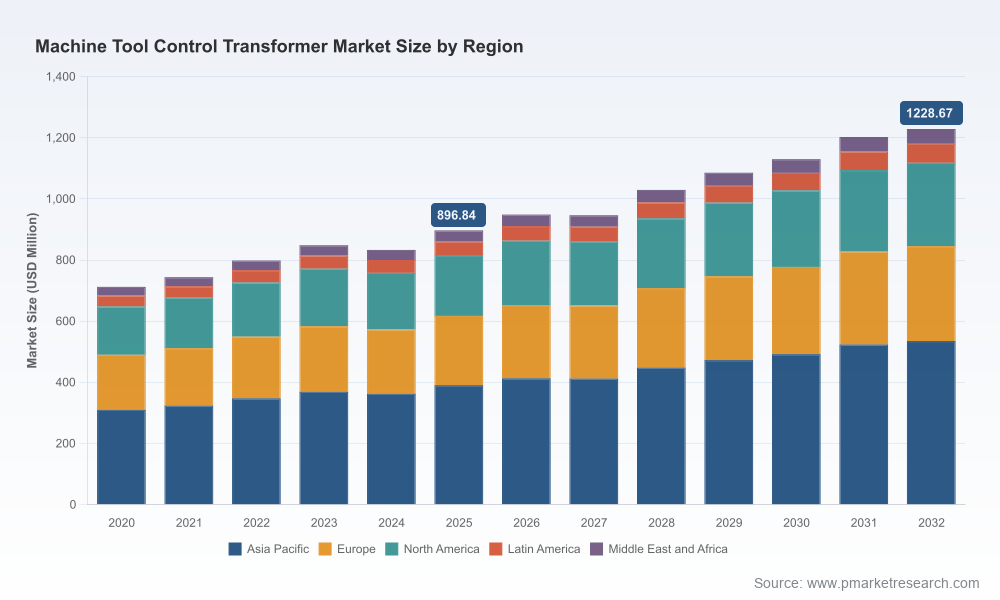

PW Consulting’s latest market study on Worldwide Machine Tool Control Transformers (base year 2025, historical period 2020–2025, forecast 2026–2032) provides an action‑oriented, board‑level briefing that translates industrial electrical component dynamics into executable strategies for 2026. The study synthesizes primary interviews, bottom‑up costing models and scenario stress‑tests to produce a rigorous market view: the global control transformer market expanded from roughly USD 712 million in 2020 to about USD 897 million in 2025, and is forecast to grow at a compound annual growth rate (CAGR) of approximately 4.6% through 2032, reaching just over USD 1.22 billion by 2032.

Worldwide Machine Tool Control Transformer Market

For executives charged with procurement, engineering roadmaps, product strategy or inorganic growth, the PW Consulting report surfaces four strategic imperatives:

Worldwide Machine Tool Control Transformer Market

Raw material volatility is the most immediate business risk. Copper—central to winding costs—spiked intraday to above USD 14,500 per tonne in January 2026 and consensus forecasts put average 2026 prices materially higher than historical norms. Electrical steel prices have almost doubled since 2020. These inputs account for a large share of production cost in dry‑type control transformers and have re‑set supplier cost structures and make‑vs‑buy calculus across the value chain (sources: IEA Analysis, JPMorgan Global Research, Taishan Transformer Insights).

Worldwide Machine Tool Control Transformer Market

Regulatory realities create a duality. The U.S. Department of Energy’s 2024 final rule on distribution transformer energy conservation explicitly excludes machine‑tool control transformers from the covered definition; similarly, California’s 2025 Energy Code exempts these units from certain low‑voltage dry‑type distribution transformer certification rules. Practically, this reduces forced product redesigns tied to federal or state distribution transformer efficiency standards in the immediate term, granting suppliers time to prioritize reliability and form‑factor innovations. However, OEMs and end users that commit to aggressive corporate energy targets may still demand higher‑efficiency components, generating a voluntary market segment where premium pricing and differentiation are possible (sources: U.S. DOE Federal Register; California Energy Commission).

On demand, factory modernization, higher automation penetration and retrofit cycles in developed manufacturing bases are the consistent tailwinds. Simultaneously, electrification trends in adjacent sectors increase competition for copper and electrical steel and accelerate supplier consolidation in upstream components.

The control transformer supplier set is a mix of specialized regional manufacturers and global players that leverage broader transformer portfolios or power‑electronics capabilities. PW Consulting’s competitive analysis—drawn from product audits, technology roadmaps and commercial interviews—highlights several strategic archetypes:

Representative firms illustrate these archetypes. North American manufacturers with broad dry‑type portfolios lead in engineered product robustness and certifications for demanding industrial environments. Several U.S. and European specialists emphasize catalog and custom control transformer lines optimized for inrush handling, isolation and factory‑automation integration. China‑based OEMs have been active in transferring technology and scaling JBK/DBK series offerings suited for CNC and automation panels, while Germany‑based component suppliers bridge global engineering standards with local production footprints.

Competitive implications for 2026:

The report purposefully blends strategic foresight with operational tools. Highlights include:

To preserve the report’s role as a strategic decisioning tool, PW Consulting discloses high‑level trends and corporate footprints publicly while reserving detailed segment tables, region‑and‑application breakdowns and company‑level revenue splits for the full report and subscription access. This “trailer” approach ensures executives can evaluate the strategic logic here and then use the detailed data‑set to execute procurement negotiations, engineering redesigns or M&A diligence.

We recommend three immediate actions for CxOs and procurement leads:

The Worldwide Machine Tool Control Transformer market in 2026 is characterized by steady headline growth underwritten by modernization cycles, but under pressure from input cost inflation and evolving buyer expectations. Suppliers that combine technical depth in inrush handling and isolation with disciplined procurement, modular product design and proactive regulatory positioning will capture disproportionate value. For buyers and investors, the window to re‑negotiate supplier relationships, de‑risk supply exposure and build differentiated product stacks is now—before commodity cycles and consolidation crystallize new competitive borders.

PW Consulting’s full report provides the granular tables, segmented forecasts and supplier scorecards necessary to operationalize these recommendations. Access to the complete dataset and downloadable decision tools is available through PW Consulting’s market research portal.

For detailed analysis of this topic, please visit the official page:Worldwide Machine Tool Control Transformer Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com