Global Depression Glass Market Growing at 5.8% CAGR Through 2031

Other |

2026-07-10 12:37:36

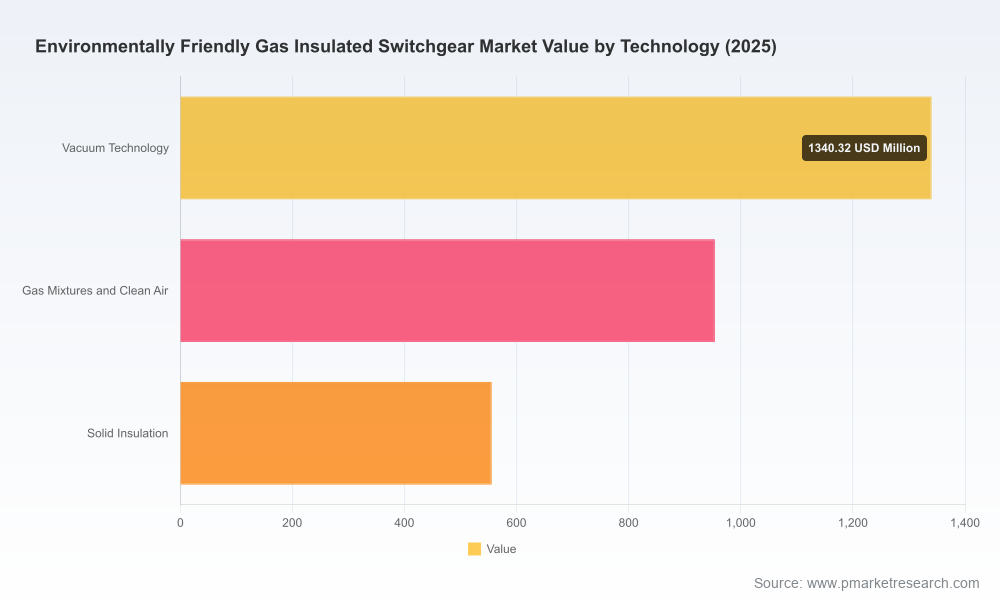

PW Consulting’s latest market study on Worldwide Environmentally Friendly Gas Insulated Switchgear (GIS) presents a forward-looking intelligence package designed to influence capital allocation, procurement strategy, and technology roadmaps in 2026 and beyond. The study consolidates a multi-year historical view (2020–2025), a rigorously modeled base year of 2025, and a seven-year forecast window (2026–2032). Headline metrics: the global market is sized at approximately USD 2,850 Million in 2025 and is projected to approach USD 4,932 Million by 2032, reflecting a compound annual growth rate (CAGR) of about 8.15% across the forecast horizon.

Worldwide Environmentally Friendly Gas Insulated Switchgear Market

Policy-driven acceleration: Regulatory milestones implemented in major markets have converted what was previously projected as incremental uptake into near-term procurement mandates for many transmission and distribution system operators. These changes compress decision timelines for utilities, original equipment manufacturers (OEMs), and large industrial end-users.

Worldwide Environmentally Friendly Gas Insulated Switchgear Market

Technology portfolio risk: Transitioning from legacy SF6-based solutions to SF6-free options is no longer optional — it is a strategic sourcing and product engineering priority. This transition carries multi-dimensional impacts on TCO (total cost of ownership), warranty and service models, and long-term maintenance strategies.

Worldwide Environmentally Friendly Gas Insulated Switchgear Market

Market structure and supplier strategy: The market is moderately concentrated, with the top three vendors commanding a near-majority share and the top five consolidating a clear leadership band. This concentration amplifies the commercial leverage of the leading incumbents while creating pockets of opportunity for highly focused challengers and regional specialists.

Our modeling shows a clear inflection during the 2023–2026 window where regulatory action, pilot deployments, and supply-chain maturation jointly increased addressable demand for environmentally friendly GIS. The next phase (2026–2032) is characterized by broad commercial scale-up: utilities move from pilots to programmatic replacement and new-build specifications increasingly mandate SF6-free or low-GWP alternatives.

Key macro drivers captured in the study include tighter F-gas regulation in regional jurisdictions, phasedown schedules for related refrigerants and gases, capital support programs for SF6-free grid pilots, and technology advances in vacuum interruption, clean-air insulation, fluoroketone and fluoronitrile mixtures, and solid insulation modules. We quantify the sensitivity of market growth to three policy scenarios and two technology-adoption pathways — enabling executives to stress-test their 2026 investment decisions against plausible regulatory and price outcomes.

Multiple SF6-free approaches are commercially viable today: g3-type fluoronitrile blends, fluoroketone-based mixtures, clean-air synthetic gas, vacuum interruption with solid insulation, and CO2-origin alternatives. Each solution presents a different mix of engineering tradeoffs (dielectric performance, leakage management, sealing technology, service lifecycle) and procurement implications.

Cost differential and procurement strategy: Eco-friendly GIS typically carries a material premium relative to incumbent SF6 designs. Buyers must incorporate lifecycle savings (regulatory compliance, carbon-cost avoidance, reduced leakage risk) into procurement models rather than relying solely on purchase price.

Critical inputs and sourcing risks: Certain niche gases and specialized sealing technologies remain subject to concentrated supply chains. Our report maps key supplier nodes and identifies single points of failure, providing procurement contingencies and supplier diversification approaches for 2026 contract cycles.

The competitive section of the report synthesizes vendor strategy, product roadmaps, deployment references, and commercial positioning. It profiles incumbent global players that are already shaping mainstream adoption through differentiated technology stacks and field-proven projects. Notable strategic moves we analyze include:

GE Vernova — advancing high-voltage g3 solutions for transmission-grade applications and recently delivering large-scale g3 installations that replace SF6 equipment in critical network nodes.

Siemens Energy — scaling its Clean Air “Blue GIS” portfolio with major grid connection wins and targeted offers for substation deployments up to MV/HV ranges commonly used in modern TSO projects.

Hitachi Energy — expanding commercial EconiQ offerings with fluoroketone-based AirPlus variants that have entered service in national grids, demonstrating compatibility with existing network architectures.

ABB — iterating its eco-efficient product line with certified AirPlus modules and strengthening commercial catalogs for higher-voltage installations.

Schneider Electric, Mitsubishi Electric, and Toshiba — each pursuing differentiated MV and HV strategies, combining vacuum, solid insulation and natural-gas-origin concepts for region-specific market entry.

Recent project wins and grid connections by these vendors are signaling a tipping point from demonstration projects toward mainstream procurement. Our competitive heatmaps and negotiation playbooks illuminate how to benchmark supplier bids, capture value in performance guarantees, and negotiate service and spares contracts that reflect the new technology mix.

Regulatory change remains the single most important non-technical risk and opportunity for market participants. Recent measures in several jurisdictions tighten allowable greenhouse gas footprints of switchgear and, in some cases, ban select SF6 applications outright from specific dates. These policy moves accelerate replacement cycles for assets approaching end-of-life and reshape specification language in RFPs. Our scenario analysis quantifies how different regulatory timelines affect capital spending needs and replacement backlogs, enabling CFOs and planning teams to prioritize budgets and timelines for 2026 procurement rounds.

This study is explicitly designed to be actionable for business leaders and includes:

Robust market sizing and forecast model (historical 2020–2025, base year 2025, forecast 2026–2032) with downloadable worksheets that allow users to run alternate assumptions and sensitivity cases.

Vendor benchmarking and reference-case analysis, including field deployment case studies and an evaluation framework for technical tradeoffs and commercial terms.

Procurement playbooks for utilities and large industrials: specification templates, scoring matrices, risk allocation frameworks, and recommended warranty/service structures tuned for SF6-free adoption.

Supply-chain risk maps and mitigation strategies covering critical gas suppliers, sealing component manufacturers, and certified testing houses.

CapEx vs OpEx modeling guidance and a TCO calculator that factors in regulatory compliance costs, leakage risk, service intervals, and residual value under alternative regulatory timelines.

Investment implications and M&A screening criteria for private equity and strategic investors seeking exposure to the clean GIS value chain (components, retrofit services, gas-supply, and aftermarket).

Short-term procurement decisions — adopt clause-based RFP language that requires SF6-free options where technically feasible and use our scoring framework to compare total lifecycle cost rather than sticker price.

Mid-term technology strategy — commit to a portfolio approach that pilots multiple SF6-free technologies in different network contexts (e.g., urban distribution vs. long-span transmission) to preserve optionality.

Supply-chain resilience — secure strategic supply agreements for critical gases and components, establish second-source qualifications, and include price-adjustment and continuity clauses in 36–60 month contracts.

Regulatory engagement — prepare utility regulatory filings and stakeholder impact assessments that justify accelerated replacement programs using the report’s scenario outputs.

To preserve the commercial value of the full study and ensure our clients gain differentiated competitive advantage, this preview intentionally omits granular regional and application splits, detailed price matrices, and certain vendor-level market-share tables. The full report contains those elements, together with interactive data tables and model access that allow corporate strategists and procurement teams to extract bespoke scenarios for board-level decision-making in 2026.

For executives preparing 2026 CapEx cycles, procurement teams rewriting RFPs, or investors sizing opportunities across the clean switchgear ecosystem, the full PW Consulting report provides the executable detail required to move from strategy to contract. The complete deliverable includes the editable forecast model, vendor scorecards, procurement templates, and a prioritized checklist for operational readiness.

Access to the full Worldwide Environmentally Friendly Gas Insulated Switchgear Market report and the downloadable forecasting model is available on PW Consulting’s research portal. Our advisory team is also offering customized briefings and scenario workshops throughout Q3–Q4 2026 to help clients convert these insights into immediate procurement and investment actions.

For detailed analysis of this topic, please visit the official page:Worldwide Environmentally Friendly Gas Insulated Switchgear Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com