Breaking: US Car Charger Market Set to Surge as Electric Vehicles Gain Popularity

Other |

2026-07-03 10:36:20

PW Consulting’s latest market intelligence delivers a rigorous, decision-ready perspective on the Worldwide Fabric Flame Retardancy Testers market as buyers, regulators, and manufacturers enter a pivotal phase in 2026. Our new study quantifies the market’s recent trajectory and clarifies the practical implications firms must act on now to preserve compliance, competitiveness, and margin. At a macro level, PW Consulting projects the market to grow from USD 115.8 Million in 2025 to USD 167.89 Million by 2032, representing a compound annual growth rate (CAGR) of 5.45% across the 2026–2032 forecast horizon.

Worldwide Fabric Flame Retardancy Testers Market

Regulatory complexity is increasing. National standards bodies and product safety agencies continue to refine flammability testing requirements for textiles, apparel, automotive interiors, and protective clothing. Buyers and test-lab operators must align equipment investments to evolving methodologies so certification timelines and market access are not compromised.

Worldwide Fabric Flame Retardancy Testers Market

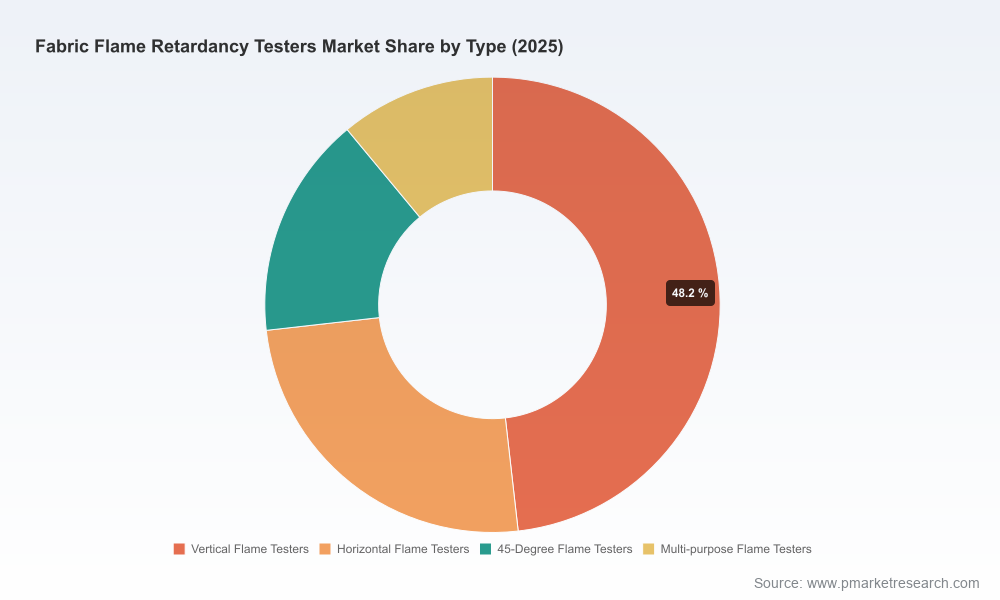

Product and channel diversification among end-users raises demand for a broader set of tester capabilities—from prescribed vertical- and horizontal-burn protocols to curtain, upholstery, and specialized protective-clothing procedures—creating opportunities for modular, multi-protocol platforms.

Worldwide Fabric Flame Retardancy Testers Market

Service and data monetization are rising. Manufacturers of testing equipment increasingly compete not just on hardware but on software, connectivity, calibration services, and training—shifting the value proposition to lifecycle services and recurring revenue.

Actionable market sizing and a seven-year forecast model with scenario sensitivity for technology adoption, regulatory shifts, and supply-chain volatility—designed for capital planning and vendor selection in 2026.

Practical buyer’s checklists for laboratories and OEMs: equipment selection matrices that map test standards to device capabilities, required peripherals, and lab accreditation pathways.

Cost-to-serve and total cost of ownership calculators customized for in-house testing setups versus outsourcing to third-party test houses—useful for procurement and make-versus-buy decisions.

Competitive benchmarking and vendor scorecards that evaluate product breadth, standards support, automation, after-sales footprint, and software/data interoperability—structured to support RFP shortlists and supplier negotiations.

M&A and partnership playbooks highlighting capability gaps in the incumbent landscape, target profiles for bolt-on acquisitions, and integration checklists for combining hardware, software, and service teams.

The market exhibits moderate concentration with leading vendors accounting for a meaningful share of global revenues while leaving strategic space for specialized entrants. Our concentration analysis indicates that the three largest suppliers command a material portion of the market, and the top five firms broaden that footprint further—an industry profile that favors scale in manufacturing, distribution, and service networks, but also rewards technical specialization and local compliance expertise.

Major equipment suppliers include well-established manufacturers and specialized instrument providers. Among notable competitors, several Chinese manufacturers offer comprehensive lines spanning vertical, horizontal and 45-degree configurations and models targeted at garments, furnishings, automotive interiors, and other end-use segments. International vendors provide complementary strengths in certain automotive and protective-clothing test chambers and in-depth solutions for laboratory automation and traceable calibration chains. Each vendor pursues a different blend of hardware breadth, regulatory coverage, and aftermarket services—creating a multifaceted competitive landscape.

Standards compliance remains the primary demand driver for tester procurement. Recent updates from major authorities reinforce the need for equipment that supports both traditional and newly specified procedures. For example, national amendments and international standards continue to refine permissible test equipment and procedural detail for clothing and textile flammability, while enduring standards for protective clothing and flame spread continue to define baseline test requirements. For equipment buyers, the practical implication is clear: select devices that are certified to run the current suite of mandatory and anticipated test methods, with firmware and software architectures that can be updated without costly hardware replacement.

Equipment manufacturers and test houses are operating in an environment of elevated and fluctuating input costs. Metals and other raw material markets have shown upward pressure and intermittent firmness into early 2026, creating margin sensitivity for lower-volume, high-precision instrument lines. Procurement strategies that reduce exposure—longer supplier contracts, localized sourcing for key components, and design choices that limit high-cost inputs—will materially affect price-competitiveness and delivery reliability.

Automation and repeatability: Buyers prefer fixtures and automation that reduce operator variance, improve throughput, and support traceable data. PLC-controlled rigs, automated igniters, and integrated optical scanning are now table stakes for labs that serve high-volume customers.

Data integration and cloud-enabled reporting: Interoperability with lab information management systems (LIMS) and secure cloud-based result repositories are becoming differentiators—particularly for manufacturers needing audit-ready compliance records across multiple manufacturing sites.

Modularity and multi-protocol platforms: Equipment that can be reconfigured to perform multiple test methods extends asset life and supports rapid response to new standards or customer requests.

Services as competitive edge: Calibration, accreditation assistance, training, and remote diagnostics convert a hardware sale into a longer-term commercial relationship and reduce churn.

For manufacturers of testing equipment: prioritize product architectures that are upgradable and service-friendly. Design modular platforms that can be field-upgraded to support amended standards. Invest in digital service infrastructure (remote diagnostics, software updates, data hosting) to create recurring revenue streams and higher switching costs for customers.

For OEMs and large lab operators: perform a targeted portfolio review of in-house testing capabilities vs. third-party outsourcing. Use PW Consulting’s TCO frameworks to quantify the break-even horizon for equipment acquisition, factoring service, calibration cadence, and throughput assumptions.

For third-party test houses: expand capabilities around rapid certification bundles that combine multiple flammability protocols, supported by traceable electronic reporting. Differentiate on turnaround, accreditation, and data security to capture outsourcing flows from upstream apparel and automotive suppliers.

For procurement and supply-chain teams: de-risk through dual-sourcing of critical components and prioritize suppliers that demonstrate responsive spare-parts logistics and calibration capabilities in key customer geographies.

For investors and M&A strategists: look for targets that fill capability gaps—either through software/data assets that extend product lifecycles or regional service providers that can accelerate market entry and customer intimacy.

Winning vendors in 2026 will combine three capabilities: standards breadth, service depth, and software-enabled differentiation. Scale allows for competitive pricing and inventory resilience; specialization enables premium positioning in niche applications (e.g., protective clothing, automotive interior standards); and digital services create stickiness. Vendors that can demonstrate consistent, auditable test outputs and offer lifecycle support (training, calibration, parts, and cloud reporting) will capture the highest-value contracts with OEMs, testing labs, and regulators.

Our report blends quantitative rigor with executable guidance. We provide the numeric runway—market sizing, CAGR, and revenue scenarios—alongside pragmatic tools (RFP templates, TCO models, vendor scorecards, and an M&A integration checklist). Crucially, we preserve the confidentiality of proprietary segmentation data to protect client competitive positioning while enabling commercial decisions: the publicly shared narrative demonstrates the analytic framework and directional findings; the complete dataset and granular splits are available through the full report and are recommended for teams making capex, product development, or M&A commitments in 2026.

Validate internal test-equipment inventories against the standards your products will need to meet in 2026–2027 and table a prioritized replacement or upgrade plan tied to revenue impact.

Run a procurement stress test: use our TCO model to quantify the financial impact of different sourcing and service models across your production footprint.

Engage with potential hardware and software partners to pilot modular systems or data-integration projects; use short pilot cycles to derisk broader rollouts.

Request PW Consulting’s vendor scorecards and RFP templates to accelerate supplier selection and shorten procurement timelines while preserving negotiation leverage.

PW Consulting’s Worldwide Fabric Flame Retardancy Testers Market report provides the strategic lens and practical tools required to make high-confidence decisions in 2026. For the full set of market splits, supplier-level detail, methodology, and downloadable decision-support templates, please access the full report on our website. Our analysts stand ready to support tailored briefings and bespoke scenario runs aligned to your capital-planning and go-to-market timelines.

For detailed analysis of this topic, please visit the official page:Worldwide Fabric Flame Retardancy Testers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com