Worldwide Pt Paste for Gas Sensor Market — Strategic Outlook for 2026

Executive summary

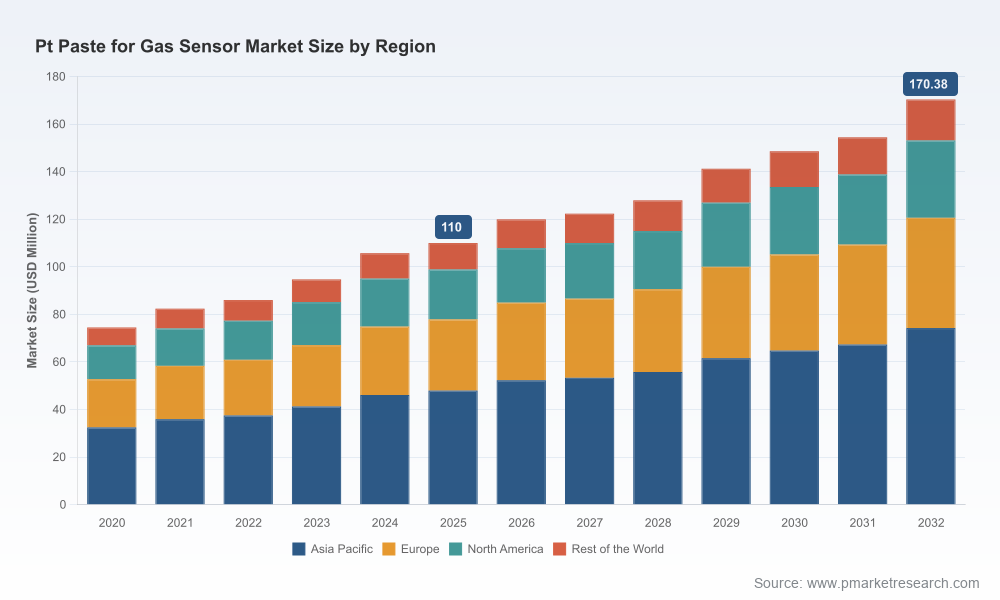

PW Consulting’s new market study on Worldwide Pt Paste for Gas Sensors delivers a focused strategic playbook for 2026 decision-makers. The global market has expanded steadily from approximately USD 74.5 million in 2020 to roughly USD 110.0 million in 2025, and our modelling anticipates growth to the neighborhood of USD 119.95 million in 2026 and onward to about USD 170.38 million by 2032. The report’s central forecast is underpinned by a compound annual growth rate of 6.45% across the 2026–2032 period, reflecting durable demand drivers in automotive emissions control, industrial monitoring and safety-sensitive applications.

Worldwide Pt Paste for Gas Sensor Market

Why this study matters for 2026 corporate strategy

- Timing: With Pt feedstock markets experiencing acute volatility, 2026 will be a year when procurement, product design and M&A choices lock in multi-year cost structures and supply footprints.

- Scale and concentration: The market exhibits material supplier concentration, with the top-three and top-five suppliers controlling a substantial share—metrics captured in our report that explain how bargaining power and supply risk translate into margin pressures and pricing power.

- Operational levers: The interplay of material composition, firing processes and sensor architectures means manufacturers who move early on formulation and process optimization will capture disproportionate quality and cost advantages.

Market dynamics shaping strategic choices

Three structural forces are defining the near-term competitive map:

Worldwide Pt Paste for Gas Sensor Market

- Feedstock scarcity and price shocks. The platinum market recorded a multi-year supply shortfall that continued into 2025—primary supply fell materially as output constraints emerged in key producing regions. Price behaviour was extreme: platinum prices rose sharply through 2025, increasing over 100% in the year as market deficits, geopolitical risks and tightening above-ground inventories fed through to traded prices. For Pt paste producers and their OEM customers, this converts an upstream commodity risk into an operational and product-cost reality.

- Regulatory and product compliance. Pt pastes for sensor electrodes and heaters are manufactured to meet RoHS2 (and related) restrictions, driving formulation changes and certifiable lead‑free production practices. Compliance choices—and the testing and documentation that support them—are non-negotiable procurement filters for OEMs supplying mobility and consumer end-markets.

- Technology and manufacturing divergence. Pt paste variants are tailored to firing temperature, substrate and print-fidelity needs. High-temperature co-fired ceramic processes hold distinct performance advantages for some sensor platforms; lower-temperature and thick-film approaches offer alternative cost and integration profiles. These technology forks influence capex, throughput and qualification timelines.

Supply chain and procurement playbook for 2026

Mitigating Pt volatility and securing continuity requires a layered strategy. Our report offers an actionable playbook that includes:

Worldwide Pt Paste for Gas Sensor Market

- Strategic sourcing: Prioritise diversified long-term offtake and recycled-PGM arrangements over spot exposure. Contract mechanisms should incorporate indexed pricing collars, defined delivery profiles and recycling credits.

- Recycling and circularity: Invest in end-of-life and in-line scrap recovery capabilities. Even modest improvements in internal reclamation lift gross margins and reduce sensitivity to market spikes.

- Supplier qualification and dual-sourcing: Use a supplier-scoring matrix to balance technical capability, geographic risk and financial resilience. For critical heater and electrode pastes, parallel qualification paths shorten the time to switch in stress scenarios.

- Financial hedging and inventory strategy: Calibrated inventory buffers coupled with tailored hedging—not blanket speculative positions—are preferable for mid-sized manufacturers; capital-light OEMs should focus on contractual protections.

Product, manufacturing and R&D imperatives

Decisions made in 2026 about process architecture and material science will shape product competitiveness through the decade. Key R&D and manufacturing priorities are:

- Formulation optimisation: Prioritise formulations that deliver the required electrical and catalytic performance with lower PGM loading or improved dispersion—this can materially reduce per-sensor PGM exposure without compromising life or stability.

- Process rationalisation: Where possible, align paste selection to firing-temperature roadmaps and substrate strategies to increase yield and reduce cycle time. High-temperature co-fired solutions and low-temperature thick-film approaches each have distinct qualification and capital implications.

- Qualification acceleration: Build accelerated ageing and cross-validation test benches to shrink sensor qualification timelines. Faster validation reduces time-to-market and the financial drag from rising material costs.

- Modular product roadmaps: Adopt modular sensor designs that allow substitution of electrode/heater paste variants with minimal redesign—this reduces the commercial impact when suppliers adjust pricing or availability.

Competitive landscape — what to monitor

The market is populated by a mix of specialty formulators, PGM houses and materials groups. Leading providers combine deep PGM expertise, tailored thick-film technologies and vertical integration capabilities. Our report includes comparative profiles and strategic assessments of major players—covering their product portfolios, firing and process know-how, geographical footprints and recent R&D or documentation updates.

- Specialist formulators bring screen-printable, fritted and high-precision pastes optimised for specific sensor architectures.

- Large PGM and materials groups offer upstream sourcing advantages, recycling capabilities and regulatory compliance infrastructure.

- Regional manufacturers can offer competitive cost structures and proximity advantages but may differ on qualification timelines and technical depth.

Notable recent moves we track: a documentation update from a leading European supplier in early 2026 refining solderable conductor paste specifications for fuel sensors, and a 2025 PGM market report from a major PGM house highlighting persistent supply deficits. These developments underscore the link between raw-material market dynamics and product-level engineering choices.

Risk, consolidation and M&A implications

Market concentration metrics indicate meaningful share held by a small set of suppliers—an important consideration for mid-sized and large OEMs. Consolidation and vertical integration are probable outcomes if raw-material stress persists and margins compress. Strategic options in 2026 include:

- Targeted acquisitions to secure feedstock, recycling or formulation capability.

- Joint ventures with specialty formulators to co-develop lower-Pt-load pastes and share qualification costs.

- Strategic partnerships with PGM recyclers or refineries to build upstream insulation from market swings.

Scenario planning: three plausible 2026–2028 pathways

Our report models multiple scenarios that quantify margin, price and supply outcomes under alternative assumptions (baseline growth at ~6.45% CAGR across the forecast horizon; stress cases reflecting deeper PGM shortages; and dampened-demand cases tied to OEM cycle downturns). Each scenario includes trigger points and suggested tactical responses—ranging from operational cost cuts to accelerated partnerships—allowing procurement, product and corporate strategy teams to stress-test plans before committing capital.

What the PW Consulting report contains (practical deliverables)

The study is designed as a hands-on toolkit for 2026. It contains:

- Historical market reconciliations (2020–2025) and a 2026–2032 forecast model with downloadable datasets in machine-readable format.

- Supply‑chain risk maps and supplier scorecards that quantify technical capability, commercial terms, and continuity risk.

- Raw‑material sensitivity modelling that links platinum price scenarios to unit cost outcomes and margin sensitivity across sensor platforms.

- Operational playbooks: procurement clauses, recycling economics, qualification timelines and capex implications for alternative paste/process choices.

- Competitive intelligence dossiers on key suppliers, including product ranges, firing-temperature capabilities, and recent public developments—enabling rapid shortlists for bid invitations and partnerships.

- Scenario-based strategic recommendations and an M&A heatmap highlighting attractive vertical and horizontal targets.

Actionable recommendations for 2026 planning cycles

- Embed material-price sensitivity into product roadmaps. Treat platinum-informed cost thresholds as gating criteria for new product launches.

- Prioritise supplier qualification workstreams now to establish alternative sources before 2027 procurement cycles peak.

- Invest in in-house recycling pilots and partnership negotiations with reclamation specialists to lower PGM exposure.

- Accelerate R&D programs that reduce PGM usage per sensor through dispersion, alloying or process improvements—these are the highest-return investments in the current cost environment.

- Evaluate selective vertical integration where scale and financial capacity permit, particularly around feedstock access and reclamation.

Next steps and how to access the full intelligence

PW Consulting’s Worldwide Pt Paste for Gas Sensor Market study is structured to support executive decision-making in 2026 and beyond. The full report contains the granular segmentation, supplier-level data, downloadable models and step-by-step implementation guidance that strategic, procurement and R&D teams need to act confidently. We intentionally present synthesis and strategic direction here while reserving the detailed segment-level tables and supplier scorecards for the full publication.

For organisations planning capex, sourcing or M&A activity in 2026, obtaining the complete dataset and scenario workbooks is a practical first step to converting market insight into defensible financial and operational plans.

For detailed analysis of this topic, please visit the official page:Worldwide Pt Paste for Gas Sensor Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com