Transcranial Doppler Devices Market Opportunities in Stroke Diagnosis and Monitoring

Health |

2026-05-06 12:25:38

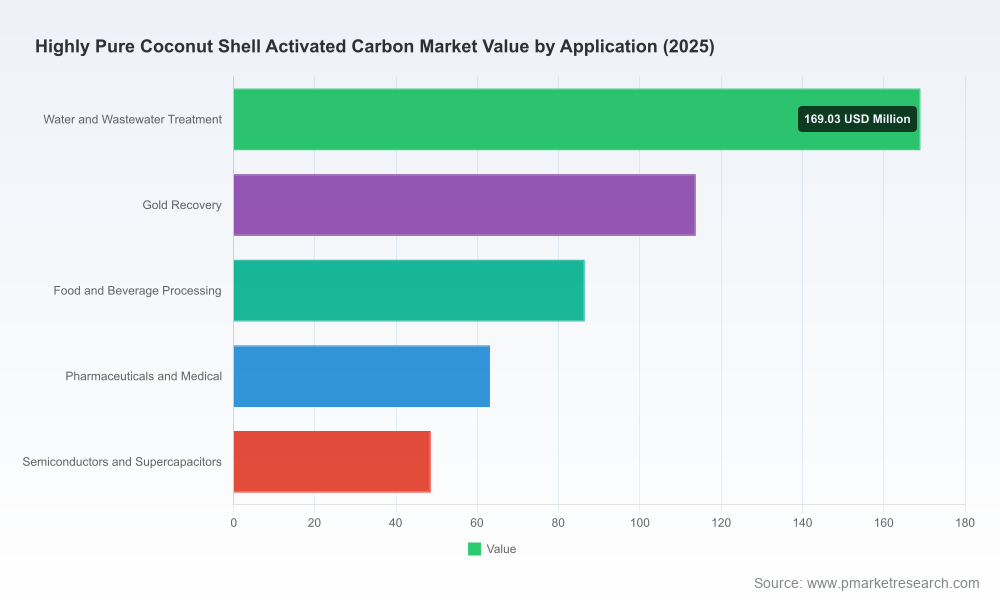

PW Consulting’s new market study on the Worldwide Highly Pure Coconut Shell Activated Carbon market provides a data-driven strategic foundation for leadership teams preparing decisions in 2026. The market has expanded steadily from 2020 through 2025 and reached an estimated USD 480.9 Million in 2025. Under our base forecast, the market resumes robust growth over the 2026–2032 horizon at a compound annual growth rate (CAGR) of 9.15%, arriving at an estimated market size approaching USD 888 Million by 2032. These headline macro trends underscore why 2026 will be a pivotal year for procurement, capacity, and M&A choices across the value chain.

Worldwide Highly Pure Coconut Shell Activated Carbon Market

Two broad forces are converging in 2026 to reshape competitive dynamics and margins in coconut shell activated carbon (CSAC): demand-side tightening driven by regulatory and industrial end-use growth, and supply-side constraints stemming from feedstock availability and logistics.

Worldwide Highly Pure Coconut Shell Activated Carbon Market

Consistent end-market expansion. Regulatory tightening in water and air quality, continued demand from specialist industrial uses (including precious metals recovery and select high-purity process streams), and rising adoption in advanced filtration and energy storage applications are broadening high-purity product demand.

Worldwide Highly Pure Coconut Shell Activated Carbon Market

Supply pressure and pricing volatility. Raw coconut shell charcoal availability tightened in 2024–2025, putting upward pressure on feedstock and finished-product prices. Several leading manufacturers responded in 2025 with list-price increases for coconut-shell grades—an industry reaction with direct implications for contracting and margin planning going into 2026.

Regional sourcing and trade policy. Rising trade frictions and tariffs on imported inputs are prompting buyers and producers to reconsider sourcing strategies and build regional resiliency—changes that will determine where new capacity and processing investments are prioritized.

Our study is designed as a decision-useful tool for C-suite and procurement leaders. Rather than a descriptive summary, the report contains actionable modules that translate market intelligence into executable options:

Market sizing and trend analysis: longitudinal topline series from 2020 through 2032 with sensitivity scenarios and upside/downside breakpoints calibrated to feedstock and regulatory shocks.

Supply-chain heatmaps: origin-to-consumer flow mapping, chokepoint diagnosis, and port/transit vulnerability assessments to support risk-mitigation and near-shoring decisions.

Price-modeling toolkit: transparent cost-build models for standard and premium-high-purity grades, enabling buyers to stress-test contracts and producers to optimize pricing bands.

Supplier scorecards and capability matrices: comparative assessments across production scale, grade spectrum, vertical integration, quality certifications, and sustainability traceability.

Commercial playbooks: practical contracting templates (spot/long-term/allocation clauses), hedging approaches for feedstock, and inventory strategies tailored to eight buyer archetypes.

Strategic options and investment cases: capex sizing, payback profiles for new activation capacity or regeneration facilities, and M&A scorecards for opportunistic consolidation play.

Regulatory and standards navigator: analysis of regulatory drivers in major markets and an impact matrix for product qualification timelines and testing requirements.

To maintain the “trailer” function of this release, detailed segment tables and origin/application splits are intentionally reserved for the full report. Those subscribers will receive the granular time-series, pricing curves, and supplier-by-grade matrices necessary for transactional decisions.

The market shows moderate concentration: the top three global players control a meaningful portion of supply, and the top five increase that share materially. That concentration pattern creates asymmetric power in times of tight feedstock supply yet leaves opportunity for agile regional producers and specialty players to capture premium niches.

Large integrated leaders: Established producers with large-scale activation capacity and vertically integrated sourcing are using their footprint advantage to secure feedstock contracts and defend margin. Strategic capacity additions by leading manufacturers in recent years signal a focus on automated, low-cost production to serve regulated water and industrial markets.

Regional specialists: Companies with proximate access to coconut shell feedstock have remained competitive on cost and logistics for local markets; they are also adapting product lines to meet certification requirements for drinking water and food-grade applications.

Specialty and value-added providers: Suppliers differentiating on high-purity grades, tailored pore structures, and integrated filtration solutions are capturing premium segments where performance and traceability outweigh raw price.

Noteworthy near-term moves that validate the above dynamics include strategic capacity expansions by producers in origin countries and industry-wide price adjustments implemented during 2025. These commercial responses highlight how quickly the cost curve can shift when feedstock tightness meets robust end-market demand.

Based on our analysis, companies that treat 2026 as a strategic horizon — not only an operational one — will be better positioned. The following imperatives are prioritized by expected impact and timing:

Secure diversified feedstock pathways: move beyond single-country dependencies; execute multi-origin sourcing and long-term supply agreements with built-in quality and sustainability clauses.

Negotiate flexible contracts: combine fixed-volume anchor deals with indexed spot tranches tied to transparent cost drivers to balance certainty and market responsiveness.

Invest selectively in vertical capabilities: consider upstream investments in charcoal processing or downstream in regeneration and reactivation to capture margin and continuity of supply, evaluated through the report’s investment case modules.

Differentiate on grade and value: prioritize product development for high-purity and specialty pore structures where buyers tolerate higher prices for performance and compliance simplicity.

Operationalize scenario planning: include feedstock shock, tariff escalation, and accelerated electrification scenarios in capital and procurement planning to ensure decisions remain robust under stress.

Pursue opportunistic consolidation: mid-scale regional players and specialty producers are potential acquisition targets for market share lift, vertical integration, and capability stacking—transaction readiness analysis is provided in the full study.

Embed sustainability and traceability: certification, chain-of-custody, and community sourcing narratives materially affect buyer choice in regulated markets; traceability investments can support price premia and long-term contracts.

The PW Consulting study is structured to be directly usable in boardroom cycles and procurement negotiations. Typical applications include:

Quarterly strategy updates: refresh topline risk matrices and supplier scorecards to inform sourcing committees and CAPEX approvals.

M&A diligence: use our supplier market maps, valuation multipliers and synergy calculators as an independent benchmark in transaction processes.

Procurement playbook execution: adopt our contract templates and pricing model to compress negotiation cycles and create defensible cost forecasts.

Investor communications: integrate the report’s independent market sizing and scenario outcomes into capital market disclosures and investor Q&A to reduce perception risk.

The 2026 planning window will reward organizations that couple tactical procurement moves with strategic structural choices. PW Consulting’s market forecast — anchored by a clear topline trajectory and a 9.15% CAGR for 2026–2032 — provides the necessary context to evaluate trade-offs between short-term cost exposure and long-term competitive positioning. The full report contains the segment-level demand analyses, origin-grade matrices, supplier scorecards, and contract playbooks required to convert insight into action.

For procurement leaders, operations executives, and corporate strategists ready to convert market intelligence into defensible decisions in 2026, access to the complete dataset and the accompanying executable modules is essential. Subscriber access to the full PW Consulting report will provide the granular tables, price curves, and supplier-by-grade detail intentionally withheld from this preview.

To obtain the full report and the boardroom-ready toolkits, visit PW Consulting’s Worldwide Highly Pure Coconut Shell Activated Carbon Market page or contact your firm representative for an executive briefing and licensing options.

For detailed analysis of this topic, please visit the official page:Worldwide Highly Pure Coconut Shell Activated Carbon Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com