High Performance Computing Market Overview: Key Drivers and Challenges

Other |

2026-02-18 06:45:21

PW Consulting’s latest Worldwide Taxi and Limousine Services Market report delivers a high-fidelity view of an industry in the middle of a structural reset. Between ongoing electrification mandates, shifting consumer preferences toward on-demand and premium mobility, and a competitive landscape shaped by both global platforms and entrenched local operators, the market entering 2026 demands decisive, data-driven actions. This briefing highlights the report’s strategic value for 2026 corporate planning while preserving the proprietary, segment-level intelligence contained in the full study.

Worldwide Taxi and Limousine Services Market

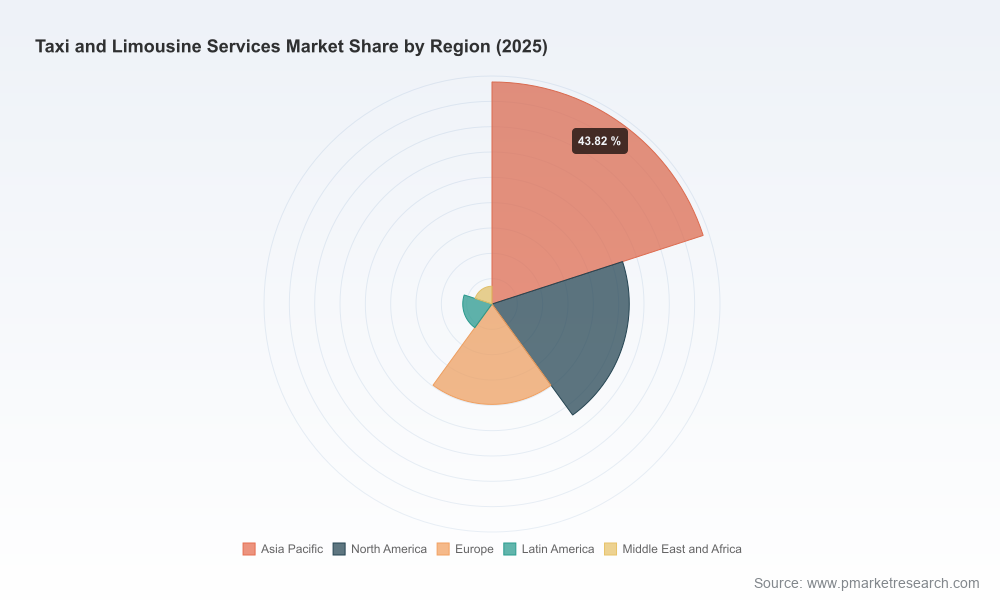

The taxi and limousine market has expanded rapidly over the last half decade and enters 2026 from a position of scale and momentum. Our topline model shows the market roughly doubling from the early-2020 base and progressing toward a multi-hundred-billion-dollar industry by the late 2020s. The forecast period (2026–2032) is modeled at a compound annual growth rate of 9.04%, reflecting the combined uplift from technology-enabled booking, premium service demand, and fleet modernization initiatives. This growth, and the underlying year-by-year sizing in our model, is the quantitative spine supporting the operational and financial playbooks we supply to clients.

Worldwide Taxi and Limousine Services Market

Regulatory inflection points will shape fleet economics. Binding regional and national targets for zero-emission miles and other clean-fleet standards mean capital planning, vehicle procurement, and charging infrastructure investment must be synchronized with compliance timelines.

Worldwide Taxi and Limousine Services Market

Platform economics and concentration trends create differentiated strategic options. The market exhibits moderate national and regional concentration—enough that platform partnerships and API integrations materially affect distribution strategy, yet fragmented enough that local operators retain negotiating leverage in many corridors.

Premium and accessibility-driven segments are redefining margin pools. Corporate travel, secure-chauffeured services, and wheelchair-accessible offerings are producing higher margin opportunities but require tailored operational capabilities and training investments that many legacy fleets have yet to deploy at scale.

Electrification and regulatory acceleration: Standards similar to the California Clean Miles Standard require transportation network companies to manage the transition toward predominantly electric vehicle miles. These rules, together with a growing set of zero-emission mandates in major cities, compress the timeline for fleet decarbonization and create first-mover advantages for operators that secure financing, charging partnerships, and vehicle supply early.

Accessibility and inclusivity as competitive differentiators: Public funding programs and grants are accelerating the procurement of wheelchair-accessible vehicles (WAV). Operators who develop WAV-capable service lines and the accompanying driver training and dispatch logic will capture underserved demand and strengthen municipal partnerships.

Premiumization and corporate demand: Corporate clients increasingly demand chauffeur-grade vehicles, vetted drivers, and security features. This is boosting demand for limousine-style and executive transport services that bundle safety, privacy, and reliability—areas where specialized providers can command premium pricing.

The market is being contested by global platform leaders, regional super-apps, and established local operators. Our report profiles the strategic positioning, operating models, and commercial levers of the primary competitors in the ecosystem, including global giants and specialist providers.

Global platforms: Market leaders with broad international footprints have scale in demand aggregation, technology, and capital markets access. Their strategic playbooks focus on platform monetization, multi-service bundling, and strategic partnerships to secure market access while navigating regulatory scrutiny.

Regional champions and super-apps: Companies rooted in regional markets leverage localized product design, payments integration, and multi-service ecosystems (e.g., food, deliveries, financial services) to deepen consumer engagement and capture share.

Specialists and premium operators: Chauffeured and limousine specialists continue to hold a competitive moat in corporate and security-conscious segments, where bespoke service quality and operational rigor are decisive.

Public and government-backed operators: In several major hubs, government-affiliated providers and regulated taxi systems remain essential partners for mobility orchestration at airports and public facilities—requiring private operators to craft cooperative strategies rather than purely competitive ones.

Our vendor-level analysis in the full report evaluates these players across capability, regulatory readiness, fleet strategy, and route economics—yielding an actionable set of scenarios and partnership recommendations tailored to buyers, investors, and operators. We intentionally withhold the full scoring and proprietary subsegment data here to preserve competitive integrity and to encourage direct engagement with the source materials.

Fleet and capital planning: Recalibrate CAPEX schedules to align EV procurement with available charging capacity and regulatory compliance milestones. Short-term leases and fleet-as-a-service arrangements can bridge gaps while preserving flexibility.

Charging and depot strategy: Secure multi-provider charging agreements and prioritize depot upgrades in corridors with the highest utilization density. Consider public–private charging partnerships to de-risk infrastructure timelines.

Service differentiation: Launch modular premium offerings—airport transfer bundles, corporate accounts with safety and privacy features, and WAV-enabled booking flows—to capture higher-margin segments and diversify revenue.

Data monetization and partnerships: Monetize route and demand data through API access, enterprise booking integrations, and targeted corporate travel solutions. Partnerships with airports, hotels, and event organizers can convert one-off demand into recurring commercial accounts.

Workforce and safety: Invest in driver upskilling programs focused on passenger safety, disability assistance, and advanced vehicle systems—areas that strengthen brand trust and meet evolving regulatory expectations.

Given the growth profile and the market’s mixed concentration, 2026 is a window for selective consolidation and strategic alliances. Buyers should prioritize targets that deliver:

Operational control in high-yield micro-markets

Proven capability in premium and WAV services

Scalable electrification pathways (fleet conversion plans, charging partnerships)

Strong municipal and airport relationships

Our M&A playbook in the full report includes valuation frameworks that account for regulatory transition costs, stranded-asset risk for fossil-fuel vehicles, and revenue upside from premiumized service lines—inputs that materially alter deal structuring and earn-out design.

Proprietary top-down and bottom-up market-sizing models with year-by-year forecasts across the 2020–2032 horizon.

Scenario analysis that quantifies regulatory and technology shocks, including sensitivity to electrification costs and charging rollout timelines.

Operator benchmarking and vendor scorecards covering service capability, regulatory readiness, and fleet economics (note: detailed scores and segment breakdowns are in the full report).

Practical toolkits: go-to-market playbooks for incumbents and new entrants, an M&A diligence checklist, and a route-to-revenue roadmap for premium and WAV services.

Regulatory heatmaps and compliance timelines that align regional policy levers with operational milestones.

Executives should treat 2026 as the year to move decisively from strategy-setting to program execution. Specifically:

Lock in fleet transition financing and charging partnerships now to avoid supply-chain and commissioning delays later in the decade.

Develop premium and accessibility service stacks as separate P&L lines with dedicated operational owners—these are clear margin enhancers and policy-aligned growth paths.

Use targeted M&A and commercial partnerships to fill capability shortfalls (e.g., WAV fleets, corporate account management, local airport coverage) rather than attempting to build every capability organically.

Embed regulatory scenario testing into every strategic and investment review to ensure resilience under accelerated zero-emission timelines.

PW Consulting’s complete Worldwide Taxi and Limousine Services Market report contains the detailed datasets, proprietary segmentation, and executable playbooks that underpin the conclusions summarized here. For boards, executive teams, investors, and municipal partners preparing 2026 budgets and strategic plans, the full report provides the empirical foundation and tactical guidance needed to convert industry trends into competitive advantage. Visit our report page to review the full table of contents, methodology notes, and options for bespoke advisory engagements that translate these insights into an implementation roadmap.

For detailed analysis of this topic, please visit the official page:Worldwide Taxi and Limousine Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com