Worldwide PDMAT Market — Strategic Outlook for 2026: A PW Consulting Intelligence Brief

PWM Consulting’s new market intelligence brief on Pentakis(dimethylamino)tantalum (PDMAT) frames a concise, action-oriented playbook for corporate leaders and procurement teams preparing decisions in 2026. Built on a 2025 base year and a full historical review (2020–2025), the study projects the PDMAT market across a 2026–2032 forecast horizon at a compound annual growth rate (CAGR) of 7.5%. Our topline sizing places the market at approximately USD 385.0 Million in 2025 and shows a clear trajectory to roughly USD 639 Million by 2032 — a growth dynamic that underpins multiple strategic choices for semiconductor material buyers, fab developers and specialty-chemicals investors this year.

Worldwide PDMAT Market

Why this brief matters for 2026 decision cycles

- Timing: Semiconductor fabs and materials buyers are finalizing supplier qualifications and inventory strategies in 2026 — choices that will lock in supply relationships through critical device-node transitions.

- Specialization: PDMAT is a high-value, process-sensitive precursor used primarily in ALD/CVD TaN barrier layers for copper interconnects; small changes in supplier purity, packaging or handling protocols can materially affect yield at sub-22nm nodes.

- Concentration & risk: The market displays structural concentration among a few specialist suppliers, which raises supply-risk and negotiating leverage issues that buyers must account for in sourcing strategies.

What the PW Consulting report delivers (executive trailer)

- Topline market sizing and forward-looking scenarios (2026–2032) with deterministic and sensitivity cases that reflect both demand-side adoption rates and possible supply shocks.

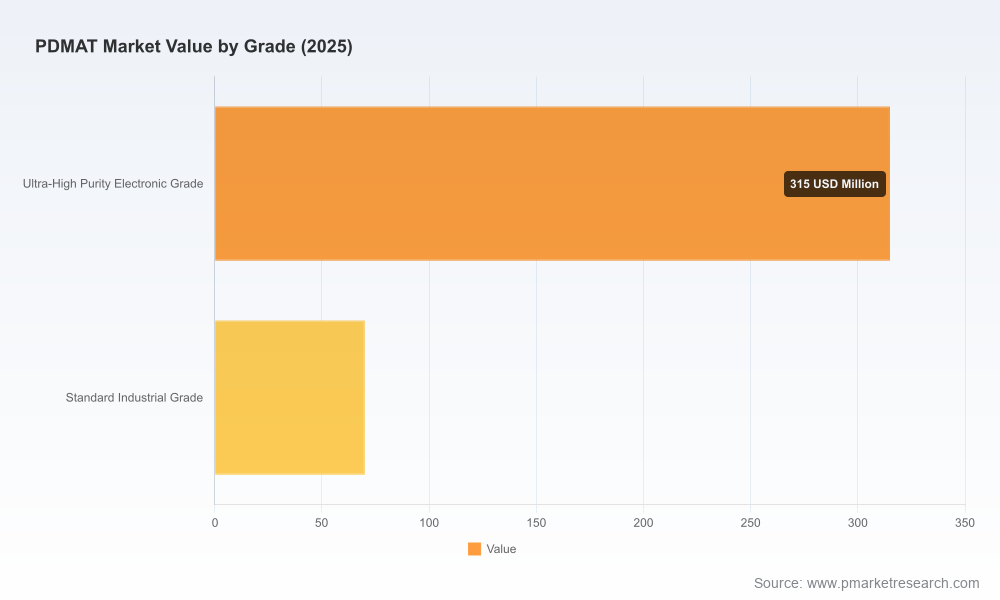

- Segment-level frameworks covering region, product-grade and deposition-method dynamics (note: this release intentionally omits proprietary subsegment allocations — full segmentation is available in the report).

- Supplier intelligence: operational profiles, capability matrices and qualification timelines for the leading global and regional PDMAT suppliers.

- Procurement and qualification playbook: recommended contract structures, dual-sourcing blueprints, inventory buffers, and CAPEX timing for in-house handling equipment.

- Technical appendix: synthesis pathways, ultra-high-purity requirements, packaging and handling best practices, and recommended process controls for ALD/CVD integration teams.

- Risk matrix and mitigation pathways: supply concentration scenarios, regulatory handling constraints and recommendations to de-risk high-volume manufacturing (HVM) adoption.

Data-driven trajectory and what it means

PDMAT sits within a specialty-chemical niche that is expanding in line with ongoing ALD adoption in advanced BEOL (back end of line) process stacks. Our study documents an acceleration beginning in the early 2020s — with market value rising into the mid-2020s — and a sustained compound growth through 2032 driven by a combination of fab capacity additions, node migration, and increased adoption of ALD-TaN barrier layers. The 7.5% CAGR over the forecast period reflects both base-demand growth and incremental switching toward higher-purity grades and ALD-centric deposition methods required by shrinking geometries.

Worldwide PDMAT Market

For decision-makers, this trajectory implies that supplier qualification, logistics readiness and purity-control processes cannot be deferred. Firms that move early to secure qualified supply and to align their process specs with supplier capabilities will reduce integration risk and shorten ramp-up time for new device generations.

Worldwide PDMAT Market

Competitive landscape — capabilities that matter

The PDMAT competitive set is populated by a mix of global chemical houses and specialized regional producers. Our evaluation of publicly available profiles and supplier collateral highlights distinct positioning vectors:

- Tier-global specialty houses (example: Merck KGaA / EMD Group) combine ultra-high-purity production, broad geographic distribution and process-support services. Their scale supports global fab rollouts and rapid cross-border logistics.

- Flexible specialty suppliers (examples: Ereztech, Strem Chemicals) excel at small-batch, research-to-production transition volumes and offer tailored packaging and bubbler configurations for ALD/CVD systems.

- Regionally anchored producers (examples from Taiwan and China) provide competitive proximity to major fabrication clusters in Asia and can be attractive partners for localized supply strategies and cost-sensitive programs.

- Niche ultra-high-purity manufacturers (examples: select European and Asian players) focus on sub-ppm impurity control and bespoke purification processes to support advanced nodes.

Market concentration metrics further inform competitive risk: the top three suppliers account for a dominant share of the market, and the top five consolidate an even larger portion. For buyers, that concentration translates into potential supply leverage for suppliers, but also clear levers for corporate counterparties to prioritize supplier diversification, qualification timelines and long-term partnerships.

Supply chain, synthesis and handling dynamics

From a technical and operational standpoint, three realities drive procurement and engineering decisions:

- Synthesis & purification: PDMAT is typically synthesized via metathesis routes that require multi-stage purification to achieve the ultra-low impurity profiles demanded by HVM ALD-TaN. The depth of purification directly affects film quality and device yield.

- Environmental sensitivity: PDMAT is highly air- and moisture-sensitive. It must be handled under inert atmospheres and packaged to prevent decomposition; common delivery formats include sealed ampoules and specially designed bubblers for CVD/ALD integration.

- Packaging & logistics: Packaging choices are not a convenience — they are a technical requirement. Glass or metal ampoules, specialized bubbler fills and moisture-scavenging logistics are operational differentiators between vendors.

These dynamics lead to tangible supplier selection criteria beyond price: demonstrated low-chloride and low-oxygen specifications, reproducible batch-to-batch performance, validated packaging systems and documented HVM support capabilities.

How the report supports concrete 2026 decisions

Organizations engaged in procurement, fab planning, or specialty-chemicals investment can use the report to:

- Prioritize suppliers for qualification based on capability matrices and regional risk assessments.

- Design sourcing strategies that balance cost, proximity and technical assurance — including staged qualification paths from research-grade to HVM-grade supplies.

- Model inventory and contract structures that reflect the market’s concentration profile and forecast growth (e.g., targeted buffer levels, multi-year purchase agreements tied to ramp milestones).

- Align internal CAPEX for handling and storage (inert-gas delivery systems, dedicated bubblers, analytical QA) with supplier packaging choices to minimize conversion risk during qualification.

- Implement mitigation plans for impurity-driven yield issues — specifying acceptance criteria, test regimes and supplier corrective action timelines.

Competitive moves and what to watch in 2026

Key near-term indicators we expect market watchers to track include new capacity announcements from regional producers, purity-improvement patents or processing breakthroughs, and contractual shifts by major fabs toward longer-term supply commitments. Given the market’s concentration, any material change in capacity or technical capability at a top supplier will echo across procurement strategies globally.

FAQ — quick technical clarifications

- Is PDMAT suitable for HVM? Yes — but only when manufactured and handled to ultra-high purity standards with validated packaging and delivery procedures tailored to ALD/CVD systems.

- How should firms approach packaging? Treat packaging as a technical specification. Options include sealed ampoules and metal bubblers; the chosen format should be validated with your ALD/CVD equipment vendor and supplier.

- Are regulatory or safety constraints material? Yes. PDMAT’s sensitivity to air and moisture means it’s typically handled under restricted-use designations and requires inert-atmosphere handling protocols in both supplier and buyer facilities.

Our recommendation — take a staged, risk-aware approach

For 2026, the recommended strategic posture is a staged, risk-aware pathway: (1) qualify at least two suppliers that meet your purity and packaging criteria; (2) secure conditional volume commitments aligned to your device ramp profile; (3) invest in modest CAPEX to control handling risk; and (4) incorporate impurity-sensitivity checks into incoming QC and yield monitoring. These measures convert forecast growth into managed, predictable supply for critical process windows.

Next steps & access to the full intelligence set

This press briefing illustrates the analytical depth and practical orientation embedded in PW Consulting’s full Worldwide PDMAT Market report. To access the complete segmentation tables, proprietary supplier scorecards, scenario-model spreadsheets and the full technical appendix — all intentionally withheld from this public summary — please consult the full report on the PW Consulting publications page. The full deliverable is designed to be a direct operational companion for procurement, process engineering and corporate development teams executing 2026 strategies.

For detailed analysis of this topic, please visit the official page:Worldwide PDMAT Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com