Oilfield Chemicals Market Overview: Key Drivers and Challenges

Other |

2026-03-18 03:18:44

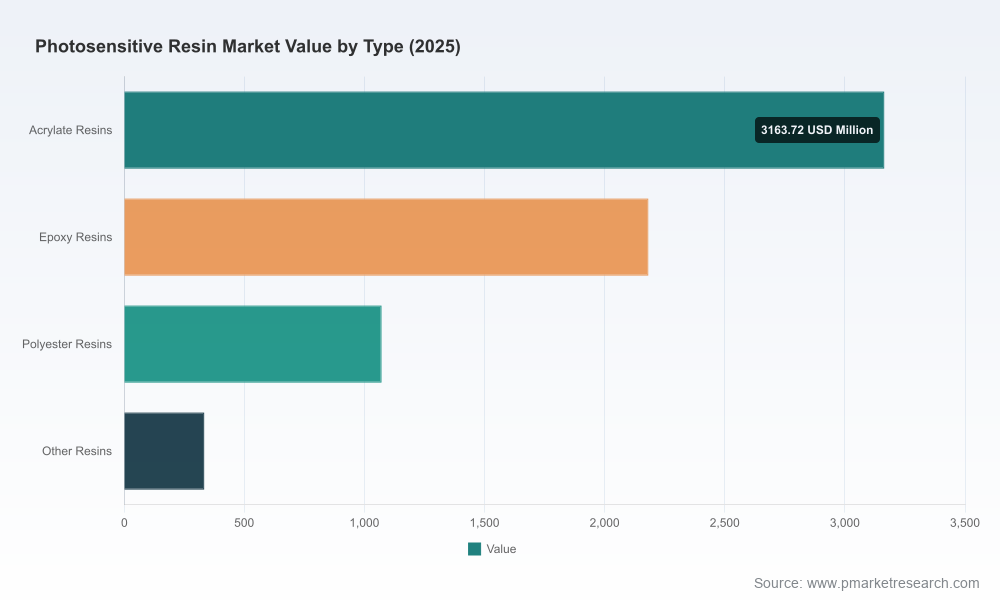

PW Consulting’s new Worldwide Photosensitive Resin Market report (base year 2025) provides executive teams with the market intelligence required to make high‑conviction strategic decisions in 2026. The global photosensitive resin market reached approximately USD 6,750.5 Million in 2025 and, at a compound annual growth rate of 12.45% (forecast period 2026–2032), is projected to more than double over the coming decade. This brief is a deliberate “preview”: it summarizes our most consequential insights, competitive interpretation, and recommended actions while reserving the full, granular segment-level data and downloadable financial models for report subscribers.

Worldwide Photosensitive Resin Market

Accelerating demand intersects with fragmentation: rapid growth across additive manufacturing, electronics, medical/dental and transport-related applications creates outsized opportunity windows but also increases competitive intensity.

Worldwide Photosensitive Resin Market

Concentration dynamics are meaningful: top-tier firms capture a material share of the market (CR3 ≈ 38.4%; CR5 ≈ 52.15%), but a long tail of specialized and regional players keeps price and innovation levers active.

Worldwide Photosensitive Resin Market

Input risk is non‑trivial: acrylate monomer experienced severe price volatility in 2023 (≈40%), while regional capacity shifts and feedstock availability are actively reshaping supplier economics.

Regulatory and sustainability forces are shaping product roadmaps: stricter U.S./EU requirements and a push for recyclability and biomass-derived chemistries are influencing formulation choices and go‑to‑market timing.

Market scale and trajectory: With a base of roughly USD 6.8 billion in 2025 and a mid-teens CAGR profile, the photosensitive resin market is transitioning from niche industrial use into broader commercial adoption across multiple end markets. The growth curve supports both volume-driven plays (scale manufacturing) and high‑margin specialty plays (biocompatible, high-temp and two‑photon resins).

Innovation intensity: In 2024 manufacturers introduced more than 120 new photopolymer grades, including heat-resistant formulations rated above 150°C and flexible resins with elongation approaching 25%. These product introductions are compressing time‑to‑adoption for new use cases and raising the bar for incumbent formulation roadmaps.

Supply-side realignments: Regional production capacity expanded (notably in Asia Pacific) during 2025, which helped moderate input costs for photoinitiators and oligomers. Nonetheless, raw material spikes remain a vulnerability—clients should plan for episodic price shocks rather than steady declines.

Sustainability and circularity: Early commercial advances (e.g., biomass-sourced photoresists) and growing recycled-content products indicate that sustainability can move from marketing differentiator to purchasing requirement within a short horizon for regulated buyers.

Our competitive analysis synthesizes public filings, new-product announcements, supply chain signals and primary interviews to map strategic postures. The market shows three overlapping player archetypes: formulation-specialists focused on 3D printing and photopolymer chemistry; systems/OEMs that tightly integrate optimized resins with printing platforms; and advanced materials houses serving semiconductor and electronics patterning.

Formulation specialists (examples: Resione, Zicai Chemical, U‑Sunny): These firms compete on speed of formulation, custom grades for MSLA/DLP/LCD systems and regional service. Their strengths are nimble R&D and close ties to desktop and industrial 3D printer ecosystem partners.

Platform-integrators and industrial resin brands (examples: Formlabs, 3D Systems, UnionTech, Liqcreate): These companies leverage hardware-resin synergies and regulatory clearances to command premium positions in dental/medical and industrial prototyping segments. Formlabs’ recent FDA clearance for a dental resin underscores the value of certification as a commercial moat.

Advanced materials and semiconductor-focused suppliers (examples: TOK, JSR, Shin‑Etsu, Fujifilm, Asahi Kasei): These incumbents bring scale, deep process knowledge and customer relationships in electronics and semiconductor patterning. Their capability to supply high‑purity, tightly spec’d photoresists differentiates them from generalist photopolymer players.

Specialty innovators (example: UpNano): Providers of ultrafast, two‑photon polymerization resins are enabling new high‑resolution markets and can command high margins where unique performance is required.

Near-term corporate moves to watch include expanded sales channels for UV-curable resins (reported in 2025), volume growth in recycled-content resins (early 2026), and early-stage deployments of biomass‑derived photoresists (announced product development in 2025/2026). These trajectories signal where incumbents will defend and where challengers will attack.

Proprietary market model (2020–2032) with top‑down and bottom‑up builds, downloadable Excel workbook and scenario toggles for price, capacity and regulatory impacts.

Segmentation analysis by region, type and application (note: this preview omits granular splits to preserve subscriber value). The full report includes interactive charts and forecast tables down to product‑grade level.

Supply chain maps and supplier economics showing feedstock flows, margin waterfalls and cost‑to‑serve differentials across key geographies.

Competitive benchmarking: revenue estimates, product pipelines, IP positions, go‑to‑market models and M&A screening shortlist with target rationale.

Regulatory and sustainability matrix detailing certification pathways (medical/dental), anticipated timeline impacts and product reformulation levers.

Operational playbooks: procurement hedging strategies, carbon and lifecycle assessment templates, and scale-up checklists for adding new grades or capacity.

Diversify monomer and photoinitiator sourcing and implement hedging: Given historical volatility (e.g., acrylate price swings), procurement must combine multi‑sourcing, inventory buffers and contractual mechanisms to stabilize margins.

Fast‑track sustainable formulation roadmaps: Invest selectively in biomass and post‑consumer recycled chemistries to secure early supplier status with EU/US regulated buyers and OEMs demanding low‑toxicity profiles.

Align R&D to differentiated performance tiers: Create separate development tracks for (a) ultra‑high‑performance resins (heat, resolution), (b) certified medical/dental grades, and (c) cost‑optimized commodity resins for volume applications.

Leverage certification as a commercial moat: Prioritize regulatory clearances where they materially shorten procurement cycles or unlock higher ASPs—medical and dental certifications are especially value-accretive.

Pursue ecosystem partnerships: OEM partnerships (printer manufacturers, dental systems) and material supply agreements create sticky demand and facilitate co‑developed product/market fits.

Use M&A tactically: Target bolt‑on acquisitions that deliver capacity, formulation IP or certified product lines rather than broad horizontal consolidation—our screening filters identify the highest IRR pockets.

Stress test pricing and capacity under alternate scenarios: Run scenario models that combine raw material spikes, accelerated regulatory lead times and regional capacity shocks to quantify downside and capital requirements.

This preview surfaces the strategic levers and market forces executive teams must consider in 2026. For practitioners building business cases, the full PW Consulting report supplies the granular segmentation tables, per‑company revenue estimates, product‑grade forecasts and a downloadable model you can plug into your planning systems. If your 2026 priorities include M&A screening, new product launch sequencing, or procurement redesign, the full dataset and our advisory team’s scenario workshops will accelerate decision quality.

PW Consulting’s industry specialists remain available to run bespoke workshops—translating the report’s implications into executable 90‑day roadmaps tailored to your cost structure, product portfolio and geographic footprint. Access to the full report and data toolkit is available through PW Consulting’s market research portal.

For detailed analysis of this topic, please visit the official page:Worldwide Photosensitive Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com