Growing Adoption of Industrial Metal AM Printers in Aerospace and Healthcare Industries

Other |

2026-05-12 09:10:33

As companies finalize budgets and strategic roadmaps for 2026, the worldwide electrostatic discharge (ESD) packaging market is moving from niche risk-mitigation to core supply‑chain strategy. PW Consulting’s latest Worldwide ESD Packing Market report—anchored on a 2025 base and a 2026–2032 forecast horizon—provides the forward-looking intelligence executives need to convert regulatory headwinds, material-cost volatility, and sustainability mandates into competitive advantage. The market is on a clear upward trajectory: our base-year sizing (2025) and modeled pathway to 2032 underpin the structural growth that procurement, product, and corporate sustainability teams must plan around.

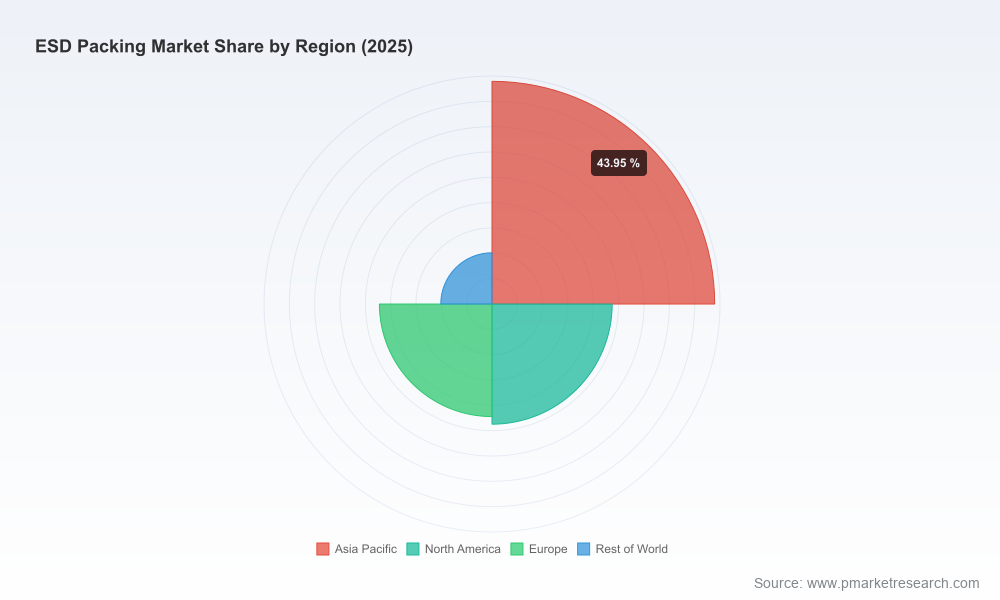

Worldwide ESD Packing Market

Our demand model synthesizes historical trends (2020–2025) with supply-side dynamics, raw-material scenarios, and adoption curves across electronics, semiconductors, automotive electronics and adjacent end markets. The result is a robust base case with a compound annual growth rate of 8.1% through the forecast window. Under that trajectory, the market expands materially from its 2025 baseline into the late 2020s and beyond—creating both volume opportunities for incumbent converters and margin pressure where raw-materials or regulatory compliance add cost.

Worldwide ESD Packing Market

For executives, the implication is straightforward: 2026 is a transition year. Investments made now—whether to qualify alternative materials, reshape supplier portfolios, or begin process changes to meet recyclability targets—will compound across the forecast period and determine whether organizations capture the benefits of growth or pay for late-stage compliance.

Worldwide ESD Packing Market

The ESD packaging ecosystem combines large diversified materials players with specialized converters and niche innovators. Market concentration is moderate: our benchmarking shows the three largest groups account for roughly one‑third of the market, while the five‑firm concentration remains well below a single dominant player. This structure creates opportunity for mid-size players and technology-led entrants to scale quickly when they prove performance and sustainability credentials.

Key companies profiled in the report span these archetypes, including established names supplying static-dissipative bags and trays, global packaging groups developing ESD corrugated solutions, and specialized manufacturers bringing recyclable or multifunctional products to market. Our competitive chapter contains vendor maturity maps, product-roadmap comparisons, and a proprietary capability‑risk matrix to support vendor selection—presented at a level sufficient for informed shortlisting while preserving the granular benchmarking behind our recommendations for premium subscribers.

PW Consulting’s report is built for executives who need to act in 2026. Rather than theory, the body of work emphasizes executable assets:

Each of these deliverables is accompanied by worked examples and decision trees—designed to be used in board decks or procurement negotiations without additional consultancy time. For organizations that require deeper support, the report identifies where bespoke modeling or lab validation is likely to be needed before multi-year commitments.

Product launches and enhancements across 2024–2025 underline the market shift described above. Manufacturers introduced recyclable ESD pouches and paper-based ESD alternatives; other suppliers combined corrosion inhibition with static control to reduce downstream failure risk. These tangible developments confirm the simultaneous emergence of two imperatives: maintain or improve electrostatic protection while meeting circularity commitments. The companies leading these moves are profiled and benchmarked in our vendor tables.

Procurement chiefs should use the report’s TCO tools to reprice packaging categories and test scenarios across short (12 months), medium (24–36 months) and long (36+ months) horizons. R&D and product teams will find the validation protocols and materials roadmaps useful for sprint planning and vendor qualification. Corporate strategy and M&A teams can leverage the market-size trajectory and vendor capability maps to prioritize targets that bring sustainable ESD IP or scalable manufacturing in geographies prioritized for growth.

Importantly, the report is designed as a working deck: slideable exhibits, data exports from our forecasting model, and templates that can be adapted for RFPs or board materials. We intentionally withhold select granular segment tables and full company-by-company financials from this summary release to protect the integrity of our benchmarking and to encourage direct engagement for tailored datasets and scenario runs.

For decision-makers preparing for 2026, the priority is clear: move from compliance planning to capability building. Use the report to set binding internal targets, reshape supplier relationships, and fund validation and pilot projects that prove recyclable and multifunctional ESD formats at scale. Organizations that act early and with discipline will convert the market’s secular growth and regulatory tightening into a differentiated offering and a lower-risk supply chain.

PW Consulting’s Worldwide ESD Packing Market report is available now. For full access to the granular datasets, vendor scorecards, and the interactive forecasting model that power the recommendations summarized here, please consult the report landing page or contact our advisory team to schedule a strategic briefing tailored to your 2026 planning needs.

For detailed analysis of this topic, please visit the official page:Worldwide ESD Packing Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com