Flavored Cashew Milk Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-30 11:52:14

PW Consulting’s latest market research on Zinc L‑carnosine (polaprezinc) synthesizes five years of historical performance and a seven‑year forecast to 2032, delivering an executive‑grade intelligence product designed to inform investment, product development, and regulatory strategies in 2026. Our analysis shows a clear, mid‑single‑digit growth profile underpinned by steady clinical and nutraceutical demand, rising API standardization, and differentiated regulatory pathways across global markets.

Zinc L-carnosine Market

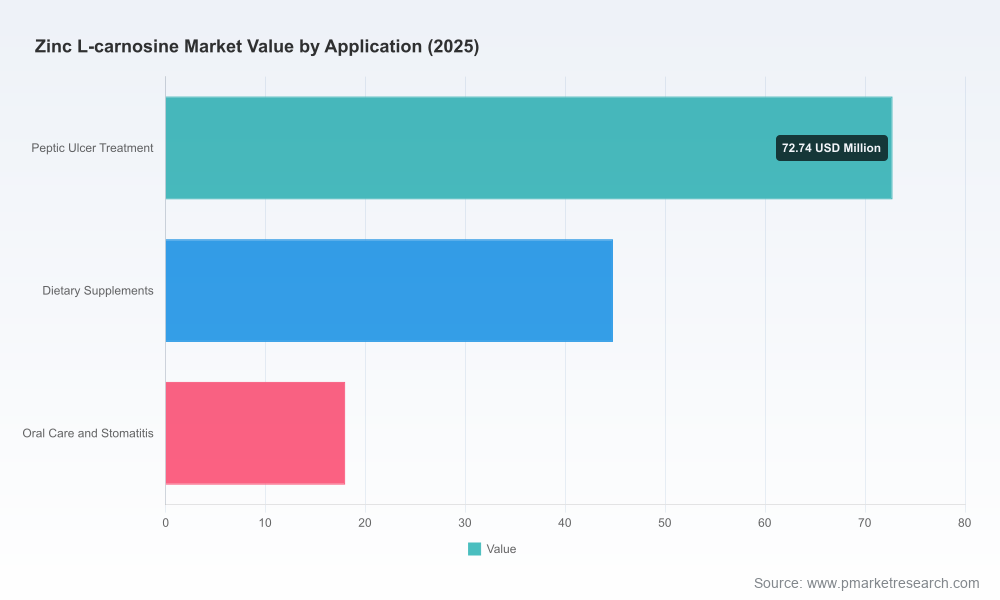

The Zinc L‑carnosine market expanded materially in the 2020–2025 period, rising from a modest base to a substantially larger, more liquid market by the 2025 reference year. This expansion reflects increased usage in gastrointestinal therapeutics and broader interest in dietary supplement formulations.

Zinc L-carnosine Market

Looking forward (2026–2032), our baseline forecast assumes compound annual growth of approximately 6.15%, reflecting a predictable, investable runway for established suppliers and new entrants that can meet API quality and certification thresholds.

Zinc L-carnosine Market

Market concentration is moderate: the top three players control a meaningful share of supply, and the top five increase that concentration further — dynamics that shape pricing power, supply security, and M&A appeal.

Validation of growth hypotheses: The report converts anecdotal industry narratives into quantified trajectories and scenario sensitivities — critical for CFOs and corporate strategy teams sizing R&D budgets or evaluating private equity interest.

Regulatory and market access playbook: For pharma and nutraceutical firms, the document dissects the divergent regulatory regimes (Asia vs. Western markets) and prescribes pragmatic pathways to market — from API filings to novel food dossiers and label claims strategy.

Supply chain and quality filters: We map the certificate landscape (USDMF/JDMF/WHO‑GMP), audit checkpoints, and procurement strategies that reduce on‑ramp risk for finished product producers and contract manufacturers.

Commercial scenarios to 2032: The report provides stress‑tested demand cases and pricing sensitivity analyses that help commercial teams prioritize channels and SKUs while preserving margin under variable raw material and regulatory cost assumptions.

Market sizing and forecast model with downloadable inputs and scenario toggles to re‑run projections for alternative CAGR assumptions and regional demand mixes.

Regulatory decision matrix outlining clinical claim windows, dossier requirements by jurisdiction, and timelines for submitting API/finished product registrations.

Supplier scorecard and RFP template that capture key quality, certification, and logistical KPIs for selecting API partners or contract manufacturers.

Go‑to‑market playbooks for three archetypal entrants — incumbent API supplier, finished‑form nutraceutical brand, and emerging biotech — with recommended budget phasing, trial design considerations, and channel prioritization.

Investor brief and M&A screening checklist to identify consolidation targets and value creation levers in a moderately concentrated supply base.

The Zinc L‑carnosine ecosystem is characterized by a mix of originators, regional API manufacturers, and bulk distributors. Competitive advantage is determined not only by capacity, but increasingly by regulatory filings, quality accreditations, and brand provenance tied to therapeutic claims.

Originator and brand anchor: The originator entity remains a strategic reference point for product identity and regulatory positioning. Their branded ingredient has stronger recognition in markets where anti‑ulcer indications are accepted, and they are leveraging certification and novel food filings to broaden addressable markets.

Specialist API manufacturers: Several producers in India and China have built reputations around high‑quality API supply and multiple GMP/DMF/JDMF registrations. For buyers, these firms represent cost‑efficient sources, but selection demands rigorous supplier audits and review of active filings to ensure market access for finished products.

Contract suppliers and ingredient distributors: European and UK‑based bulk ingredient houses play a crucial role in blending regulatory compliance with logistics and formulation know‑how for finished product companies, especially in the nutraceutical channel.

Recent institutional moves: Notable regulatory filings and registration updates in 2024–2026 — including new DMF/JDMF activity and bioequivalence work tied to reference formulations — signal an acceleration in both generic development and efforts to legitimize broader therapeutic use.

Regulatory dualism: In established East Asian markets, Zinc L‑carnosine is positioned and reimbursed as an anti‑ulcer pharmaceutical; in most Western jurisdictions it is marketed as a dietary supplement or novel food ingredient. This dual regulatory identity creates differentiated commercial paths and claim sets for manufacturers and brands.

Certification as a market entry gate: Active DMF/JDMF and WHO‑GMP filings are not optional for suppliers targeting pharmaceutical channels. The presence of these filings among Chinese and Indian manufacturers materially de‑risks supply for firms seeking to launch regulated finished products.

Raw material and composition considerations: The compound’s chelated chemistry and defined composition profile are important for formulation teams and regulators alike; specification harmonization reduces analytical friction in cross‑border approvals.

Scientific interest and label expansion: Emerging scientific reviews published in 2026 highlight potential indications beyond gastroenterology, rekindling interest among clinical researchers and biopharma sponsors. These developments will likely influence premiumization strategies for branded ingredients.

For established API suppliers: Prioritize advanced filings (e.g., USDMF/JDMF) and invest in visible quality credentials. Securing regulatory references and support materials for bioequivalence studies will preserve share in pharmaceutical channels and enable premium pricing.

For nutraceutical and finished product brands: Adopt a dual‑track market access strategy — secure high‑quality supplier relationships while pursuing novel food or ingredient dossiers in target jurisdictions to unlock stronger claim sets and expanded retail placement.

For investors and M&A teams: Target consolidation opportunities where quality accreditation and regulatory filings are present but commercial reach is limited. Value creation will come from scale in distribution, dossier completion, and integration of formulation capabilities.

For R&D and product development: Consider controlled clinical programs that bridge gastroenterology claims with emerging therapeutic hypotheses. Sponsors who can translate recent scientific interest into robust clinical evidence will own differentiated market positions.

For procurement and supply chain leaders: Build multi‑sourcing strategies with staggered qualification milestones to mitigate supply shocks while meeting certification requirements for regulated markets.

This report is intentionally operational: beyond macro forecasts and competitor profiles, it supplies actionable templates (RFPs, dossier timelines, supplier scorecards) and an interactive model that lets teams stress‑test market scenarios against changes in regulatory tempo, pricing, and adoption curves. The approach is tailored to ensure that strategy teams can move from decision to execution within a 90‑ to 180‑day window.

PW Consulting’s Zinc L‑carnosine Market report is published with source models, supplier annexes, and our proprietary scenario engine. The public summary above outlines strategic insights and directional data; for full segmentation tables, granular regional and application breakdowns, and the complete competitive intelligence annex — including supplier contact matrices and filing IDs — please refer to the report page on our website. The withheld segmentation details and supplier financials are available to subscribers and licensed report purchasers to protect commercial value and preserve competitive integrity.

For C‑suite teams, regulatory leads, and investment committees planning for 2026 and beyond, this report turns a niche ingredient story into a concrete set of strategic choices. PW Consulting stands ready to support bespoke advisory engagements that translate these findings into acquisition diligence, market entry plans, or supplier qualification programs.

For detailed analysis of this topic, please visit the official page:Zinc L-carnosine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com