Augmented Analytics Market Size, Growth Trends, and Forecast to 2034

Other |

2026-06-08 10:58:58

The Cloud VPN market has moved from supporting remote access as a niche utility to becoming a strategic backbone for enterprise hybrid and multi‑cloud networking. Our latest Worldwide Cloud VPN Market study (base year 2025; forecast 2026–2032) provides the decision-grade intelligence enterprise CIOs, CISOs, cloud architects, and investors need to design resilient, compliant, and cost‑efficient connectivity strategies as they plan for 2026 and beyond.

Worldwide Cloud VPN Market

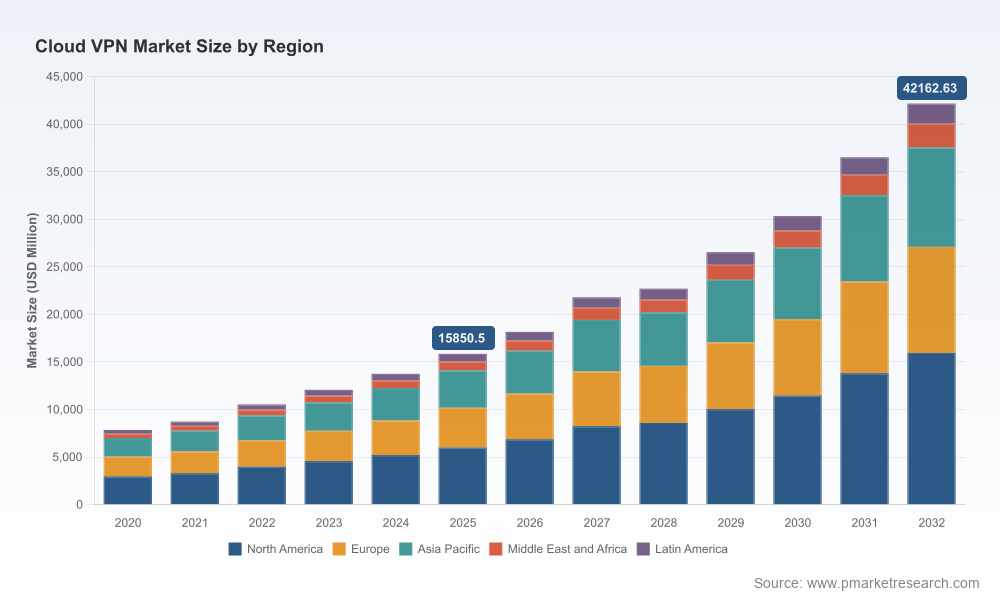

Corporate networking choices made in 2026 will lock in security postures, regulatory exposures, and multi‑year cost trajectories. The market is large and expanding rapidly — having roughly doubled in size over the 2020–2025 period — and our analysis forecasts continued strong expansion through 2032 at an approximate compound annual growth rate of 15.0%. That trajectory creates both opportunity and complexity: vendors are innovating aggressively, cloud platforms are embedding connectivity services deeper into stacks, and regulators plus infrastructure constraints are reshaping where and how secure tunnels are provisioned.

Worldwide Cloud VPN Market

This release is designed as a strategic “trailer”: it surfaces the high‑value insights and practical implications that enterprises must consider immediately, while directing stakeholders to the full report for the granular segment tables, vendor scorecards, and interactive models that underpin confident procurement and investment choices.

Worldwide Cloud VPN Market

Scale and speed: The Cloud VPN market crossed an important scale threshold in 2025 and is forecast to more than double again by the end of the 2026–2032 planning horizon. That scale increases the stakes for selecting architectures that balance performance, security, and regulatory compliance.

Economics under pressure: Rapid growth coexists with rising operating costs for cloud infrastructure providers and enterprises alike. Regionally concentrated data center electricity demand and volatile wholesale power prices are already elevating TCO for cloud‑hosted VPN services — an operational variable many IT teams have not yet fully internalized.

Platform convergence: Cloud providers, networking incumbents, and security‑first vendors are converging around integrated Secure Access Service Edge (SASE) and Zero Trust Access models. This convergence accelerates migration away from legacy on‑premises VPN appliances but introduces complexity when combining multiple vendor stacks and sovereign deployments.

Regulatory fragmentation and data sovereignty: Global data‑localization initiatives and sectoral rules (financial services resilience frameworks and national data protection measures) are making jurisdictional control over processing and telemetry a primary determinant of cloud VPN architecture. Compliance is no longer an add‑on; it is a design constraint.

National security and cross‑border data restrictions: New rules limiting bulk transfers of certain sensitive personal data are influencing where encrypted tunnels terminate, how key material is managed, and which cloud regions can host control‑plane components.

Operational energy and infrastructure constraints: Forecasts of sharply higher electricity demand for concentrated data center clusters mean that energy cost and availability will increasingly be considered in vendor selection and site placement for VPN concentrators and transit nodes.

Technology substitution and hybridization: Zero trust application access offerings are displacing some traditional remote‑access use cases, while site‑to‑site connectivity remains essential for hybrid cloud and legacy system integration. Organizations will increasingly adopt hybrid patterns that combine cloud VPNs, ZTNA, and SD‑WAN overlays.

The supplier ecosystem is a mix of hyperscalers, security platform vendors, and specialised networking providers. The competitive dynamics are shaped by two vectors: (1) breadth and depth of cloud and security portfolios; and (2) ability to deliver globally consistent, auditable, and sovereign‑aware connectivity.

Hyperscale cloud providers (notably those with established cloud networking stacks) are competing to make VPN capabilities a native, high‑performance part of their platform. Their advantages include global backbone scale, deep integration with cloud routing constructs, and bundled operational telemetry — attractive for organizations standardizing on a primary cloud provider.

Security‑centric vendors are embedding VPN functionality within broader SASE and Zero Trust offerings. Their strengths lie in policy‑centric access controls, threat prevention, and unified security telemetry. For customers prioritizing granular access policy and auditability, these vendors will remain compelling.

Specialists and appliance vendors continue to serve complex hybrid environments and performance‑sensitive use cases where customers require bespoke tunneling topologies or appliance parity in the cloud.

Recent vendor moves illustrate these trends. In late 2025 a leading hyperscale provider announced a VPN Concentrator product to simplify efficient multi‑site site‑to‑site connectivity via its transit fabric, reflecting a push to reduce orchestration complexity for widely distributed, low‑bandwidth endpoints. In early 2026, a prominent edge security vendor entered a strategic partnership extending application protection capabilities into small business and critical infrastructure segments — signaling that security vendors are broadening reach through channel and industry partnerships.

Our report is intentionally practical. Beyond market-sizing and directional forecasts, the deliverables you will use in 2026 include:

Decision frameworks to map connectivity requirements (performance, sovereignty, auditability) to architecture patterns and vendor archetypes.

Vendor positioning and scorecards that compare capabilities across security, cloud integration, SLA design, and deployment operationalization; these are distilled to inform RFP shortlists without bias to a single procurement model.

Deployment playbooks and migration roadmaps for moving from legacy VPN appliances to hybrid cloud VPN + ZTNA topologies, including staged rollback plans and vendor interoperability checklists.

TCO and sensitivity models that bring energy cost, bandwidth pricing, and compliance overhead into multi‑year cost projections so CFOs and procurement teams can make apples‑to‑apples comparisons.

Regulatory compliance matrices aligned to key frameworks (financial sector resilience requirements, national data transfer rules, and EU operational resilience acts), with prescriptive controls and audit artifacts to reduce second‑order compliance risk.

Scenario analyses that stress‑test architectures against three realistic 2026 risk vectors: concentrated energy price spikes, tightened cross‑border transfer rules, and rapid adoption of ZTNA by a large enterprise cohort.

Re‑baseline connectivity costs with energy and compliance in mind. Run TCO models that include power consumption and regional price volatility. This is no longer an infrastructure footnote; it changes where you place transit termination and how you size concentrator capacity.

Design for sovereignty and auditability from day one. Where regulatory rules impose local processing or restrict data flows, architect for localized control planes and immutable auditability. Ripping and replacing later is costly and operationally disruptive.

Embrace hybrid patterns. Adopt a hybrid posture that combines cloud‑native VPNs for scale, SASE/ZTNA for application access, and SD‑WAN for site performance. This mix yields resilience and reduces vendor lock‑in risk.

Prioritize vendor interoperability and open telemetry. Require interoperable control APIs and standardized telemetry exports in procurement contracts to avoid opaque silos and to enable unified observability across multi‑vendor deployments.

Plan for staged adoption with clear rollback guardrails. Test migrations in low‑risk lines of business, instrument controls, and keep a short rollback path until operational maturity and auditability are proven.

This announcement primes your strategic thinking but does not publish the granular segmentation tables and vendor quantitative scorecards that underpin procurement and valuation decisions. The full report contains the disaggregated regional, component, and connectivity‑type analyses, precise historical series, and our vendor financial overlays — material that procurement teams and investors will need to finalize RFPs, vendor shortlists, and investment theses. As a preview, we have highlighted directional trends and actionable recommendations necessary to begin board‑level briefings and vendor negotiations in 2026.

If your organization is planning any of the following in 2026 — a cloud consolidation, a shift to SASE, expansion into regulated geographies, or a major refresh of remote access architecture — PW Consulting’s full Worldwide Cloud VPN Market report is structured to accelerate decision cycles and reduce costly rework. The complete report includes interactive cost models, vendor scorecards, deployment playbooks, and compliance checklists ready for immediate operational use.

Contact our research team to schedule a tailored briefing, or visit the PW Consulting publications page to access the full study and supporting tools. Our advisors are available to run a rapid 72‑hour workshop to translate the report’s findings into a project‑level migration and procurement plan tailored to your environment.

PW Consulting — helping infrastructure leaders convert market complexity into strategic clarity as they design the secure, compliant, and cost‑efficient connectivity platforms of 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Worldwide Cloud VPN Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com