Breaking: Facilities Building MRO Market Set to Reach $145.3 Billion by 2035

Other |

2026-06-25 11:06:58

PW Consulting’s latest market study on the Worldwide Bottom Anti-Reflective Coatings (BARC) market delivers a forward-looking, decision-ready intelligence package for semiconductor materials leaders, equipment OEMs, fabs and private equity. Built on a 2025 base and a detailed historical series from 2020–2025, the report models the market through a 2026–2032 forecast window and quantifies an expected compound annual growth rate (CAGR) of 6.72% across the period. Measured in USD Million, the analysis frames near-term revenue momentum and medium-term scenario pathways that will directly influence capital allocation, sourcing strategies and product roadmaps in 2026.

Worldwide Bottom Anti-Reflective Coatings (BARC) Market

Timing: 2026 is a critical inflection point as the industry balances ramping EUV adoption, high-NA pilot activity and legacy lithography throughput optimization. Our forecast horizon captures the revenue runway that underpins equipment cadences and materials qualification timelines.

Worldwide Bottom Anti-Reflective Coatings (BARC) Market

Operational Significance: BARC is a production-critical specialty chemical. Small formulation shifts, capacity constraints, or supply-chain tariffs translate quickly into wafer cost and yield impacts — the sort of inputs executives must model into 2026 budgets and supplier scorecards.

Worldwide Bottom Anti-Reflective Coatings (BARC) Market

Strategic Clarity: The report translates macro growth into tactical actions — where to invest in capacity, which chemistries to prioritize for qualification, which regions present resilient demand versus regulatory friction in 2026.

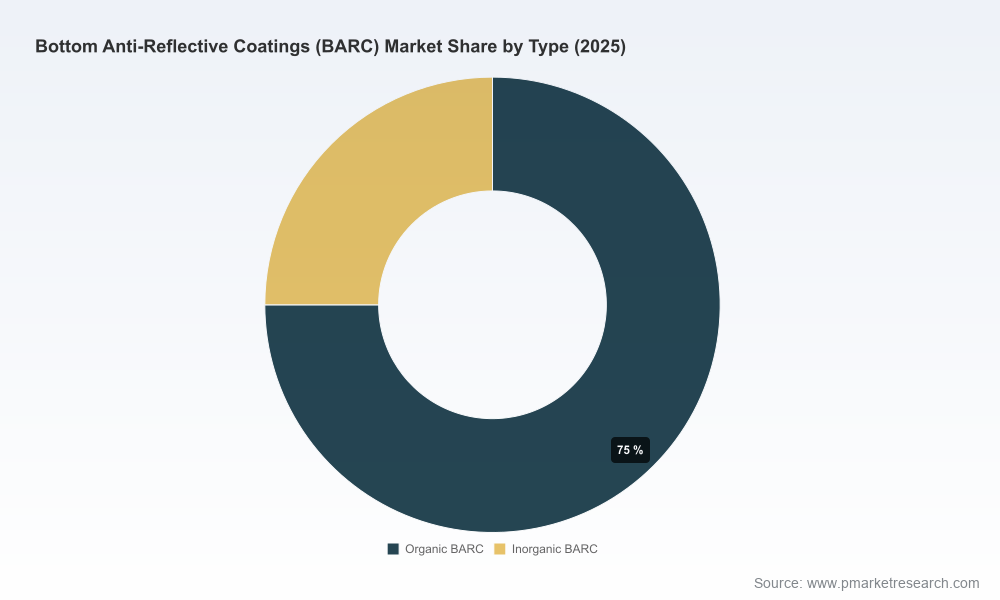

Our modeling shows the BARC market has sustained steady expansion through the early 2020s and is projected to continue growing at a mid-single-digit CAGR into the early 2030s. This expansion is driven by three structurally supportive forces: intensified lithography complexity at advanced nodes, persistent demand for yield-enhancing process chemistries in mature nodes, and incremental upgrades tied to EUV/high-NA pilot flows. While we disclose aggregate market sizing and the headline CAGR here to orient executive planning, the granular splits across region, application and lithography types are intentionally withheld in this executive synopsis to preserve the tactical value of the full report.

Qualification lead times remain the gating factor. Materials teams must align multi-year roadmaps with customer node transition timetables — accelerating internal qualification and cross-functional integration to avoid costly last-minute rework.

Portfolio bifurcation: product roadmaps that separate legacy KrF/i-line optimization from ArF/EUV-targeted chemistries are demonstrating both risk reduction and margin uplift for incumbent suppliers.

Supply resilience is a differentiator. Firms with diversified precursor sourcing, redundant production lines and logistics contingency plans capture outsized share during episodic disruptions.

M&A remains an underleveraged lever: targeted tuck-ins that add specialty resin chemistries or regional capacity can be faster and more cost-effective than greenfield builds to capture 2026 demand peaks.

Comprehensive market model (2020–2032): downloadable Excel with base-case and two alternative scenarios, enabling sensitivity analysis on throughput assumptions, pricing and input-cost volatility.

Go-to-market playbooks: role-specific templates for suppliers, fab procurement and materials integrators covering qualification timelines, sample management best practices and commercial contracting benchmarks.

Supply chain and input-cost module: bottom-up cost drivers for key monomers and solvents, plus stress-test outputs to quantify margin impacts under common disruption scenarios.

Regulatory impact assessment: actionable compliance timelines and reformulation pathways for major jurisdictions, with a focus on EU chemical restrictions that will require product adjustments for 2026 market access.

Competitive heatmap and capability matrix: vendor and technology mapping that helps planners prioritize partnerships, capex and M&A targets without exposing proprietary share tables in this summary.

Investment and procurement decision frameworks: ROI calculators, supplier scorecards and inventory hedging strategies tailored to BARC’s process-critical cadence.

The BARC supplier universe is dominated by established specialty chemical firms and electronic materials divisions that combine deep lithography domain expertise with global manufacturing footprints. PW Consulting’s analysis emphasizes technology differentiation, production capacity posture and customer co-development track records more than raw share numbers — these qualitative dimensions drive competitive advantage in 2026.

JSR Corporation (Tokyo, Japan): A leading supplier with ArF/KrF-optimized AR series products and an active development track into EUV-compatible formulations. Recent product introductions targeting high-NA EUV indicate an aggressive move toward next-generation qualification lanes (October 2025).

Dow Electronic Materials (now part of DuPont; Midland, Michigan, USA): Offers a catalog of BARC solutions for advanced nodes and is positioned to leverage DuPont’s broader materials platform for integrated offerings. Their portfolio approach emphasizes process consistency and global support for major foundry customers.

Tokyo Ohka Kogyo (TOK; Kawaguchi, Japan): Specialized resin manufacturing with targeted capacity expansions to support sub-2nm node demand. Their Kawasaki plant expansion (announced June 2025) signals readiness to meet high-margin, node-specific resin demand.

Shin-Etsu Chemical (Tokyo, Japan): Strong DUV product lines and certification milestones that support trust in high-volume fabs. Their regulatory and quality track record makes them a preferred partner where process control and supply assurance are prioritized.

Nissan Chemical Corporation (Tokyo, Japan): Focused on formulation adaptations for 193nm and emerging EUV flows; their product diversification provides resilience across lithography transitions.

AZ Electronic Materials (now part of Merck KGaA; Darmstadt, Germany): Offers high-resolution BARC chemistries and benefits from Merck’s global distribution and R&D scale, particularly in markets where integrated service agreements matter.

Collectively, these suppliers demonstrate a mix of organic innovation and capacity moves; the market rewards firms that pair R&D investment with nimble production scaling. Our full report includes a comparative capability matrix and supplier risk scorecards to guide sourcing decisions in 2026.

Raw material pressure: Certain resin monomers have experienced notable year-on-year price increases driven by supply constraints — this input inflation should be modeled into gross margin scenarios and contract renegotiations.

Regulatory friction: New chemical use restrictions in key regions require reformulation timelines and compliance costs to be factored into time-to-market for affected products. Firms that pre-emptively redesign formulations will mitigate 2026 market access friction.

Trade and tariff exposures: Post-2025 tariff developments have introduced import cost differentials that shift procurement optimization and location strategies. Companies with localized production or tariff mitigation strategies will have advantage.

Logistics volatility: Transportation surcharges and route disruptions raise landed cost uncertainties; dual-sourcing and inventory buffers provide practical mitigation pathways for 2026.

Prioritize qualification parallelization: Move from sequential to parallel qualification tracks for ArF/EUV chemistries; compress validation cycles by investing in joint testbeds with key customers.

Hedge input costs via supplier partnerships: Negotiate multi-year supply agreements with indexation and volume collars for critical monomers; evaluate upstream investments or long-term off-take where pricing volatility is highest.

Assess near-shore capacity expansions: For companies exposed to tariff or logistics risk, near-shoring targeted resin production can reduce landed cost and improve time-to-market for fabs ramping in-region.

Commit to regulatory-first product roadmaps: Incorporate regulatory gating criteria into product development stage gates so that reformulation costs are surfaced early and not as late-cycle surprises.

Use M&A to buy capability, not just volume: Identify acquisition targets that bring differentiated chemistries or qualification relationships with foundries rather than only incremental capacity.

Executives who need to finalize 2026 budgets, vendor strategies and R&D prioritization will find the report’s integrated model, supplier diagnostics and practical playbooks immediately actionable. The document balances quantitative scenarios (2020–2032) with qualitative, on-the-ground intelligence — including supplier developments, certification milestones and regulatory shifts — so leaders can move from insight to execution in a 60–90 day planning window.

For full access to the dataset, region-by-region and application-by-application breakdowns, detailed supplier scorecards and the downloadable scenario models that underpin our 6.72% CAGR projection, please consult the complete PW Consulting Worldwide BARC Market report. The report contains the granular segmentations and proprietary tables intentionally omitted from this synthesis to preserve the competitive value of our research and to support client-level strategic deployments.

For detailed analysis of this topic, please visit the official page:Worldwide Bottom Anti-Reflective Coatings (BARC) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com